When you’re investing, you need to focus on the long-term.

This is one of those pieces of received wisdom that everyone has heard, and

most people at least pretend to believe it, but it’s often wildly misinterpreted.

There’s this idea out there that stocks get safer the longer you hold onto them

because you can ride out the bad periods if you are disciplined enough – it’s

just a matter of sticking around until the market rewards you for being a “good

investor.”

To put it simply, this is not the case.

Since we’re always talking about how you need to focus on the long-term, and be a disciplined investor, we should probably break this down a little bit more.

People often think that the stock returns (as well as the returns of most risky assets) basically average out over time. So long as you stay invested for a long enough period, you should get roughly the market’s historical average return. In essence, the risk that the market is paying you for taking on is the short-to-medium term volatility of returns – not the risk of the underlying companies. Now let’s think about why the market doesn’t operate this way.

The Market Doesn’t Give Things Away

The first problem is around how the market operates. If the markets were offering really high returns simply for having a really long holding period, wouldn’t this get whittled down pretty much immediately? There are a huge number of market participants with long time horizons who can commit (or convince themselves that they are committed) to buying and holding, such as insurance companies, sovereign wealth funds, endowments, and even retirement investors. All of these participants would be happy to pay a little bit more for “guaranteed” stock returns, and this is exactly how a security’s expected return is reduced. A security’s expected return is inversely proportional to it’s price. The more you pay for a security, the lower it’s expected return will be in the future.

What’s happening here is that people with long time horizons are bidding up the price of stocks, and driving down their future returns. They keep driving up the price of stocks until that investment doesn’t look so special anymore – until their expected return is in line with their long-term risk (1). Stocks would end up looking a whole lot like bonds, just without the specific contract on payouts.

The Market is a Shark

For stock returns to average out to somewhere close to their historical returns over time means that the markets effectively need to remember where they have been, and adjust based on that information. A fancier way of saying this is that for stocks to become safer in the long run, you need to think that the market exhibits mean reversion. If you’ve had a run of bad returns, then you are more likely to get good returns in the future, and vice versa.

A good way to visualize this idea is to think of a rubber band. As you stretch away from the average return that you are “supposed to” get, the rubber band will pull you back towards the middle. While this is a nice visual, it’s not really accurate. The market certainly has a memory – all of the historical information about a security is incorporated into its price – but it’s always moving forward. Future price movements are based on how new information squares with the market’s expectations, not how either the market, or some individual company has done in the past.

The Average is the Average

The average return is just that – the average of all the historical returns. There is nothing particularly special about that number. The one nice thing about it though, is that it can serve as a decent starting place for planning purposes as it can give you an anchor for figuring out what a security’s expected return will be going forward. For a quick and dirty example of this, look at the range of outcomes for the S&P 500 Index over rolling periods. To put these numbers in perspective, the annualized return of the S&P 500 Index from 1926-2019 was 10.20%.

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Data from 1926-2019. 20, 30, 40, and 50 year periods are monthly rolling period lengths. For illustration purposes only. Indexes are not available for direct investment. Past performance is not indicative of future performance.

There are a few items of note here. First off, it’s important to remember that we are looking at only the extremes here, but we can still see some patterns. Secondly, even though the range between the best and worst periods generally decreases the longer your period is (dramatically when you step from 20 to 30 years), were still looking at a pretty big range of possible returns. Not only that, but the range actually increases when we step from 40 to 50 years periods.

There’s a rough tendency to be around the long-term annualized return, and you tend to be closer to it the longer you stay invested, but it’s just a tendency. We don’t need mean reversion to explain it. Every year’s market return is basically an independent draw; the expected return for each of those returns is (reasonably) close to the long-term historical return (2). If you get a return far from the expected return it’s not that the next year has a higher than normal chance of getting a “typical” return, it’s just that getting a big return is unlikely in any given year.

So Why Focus on the Long-Term?

This all raises a pretty fundamental question: if your expected return for stocks doesn’t increase with time, why do we always talk about staying disciplined and focusing on the long-term?

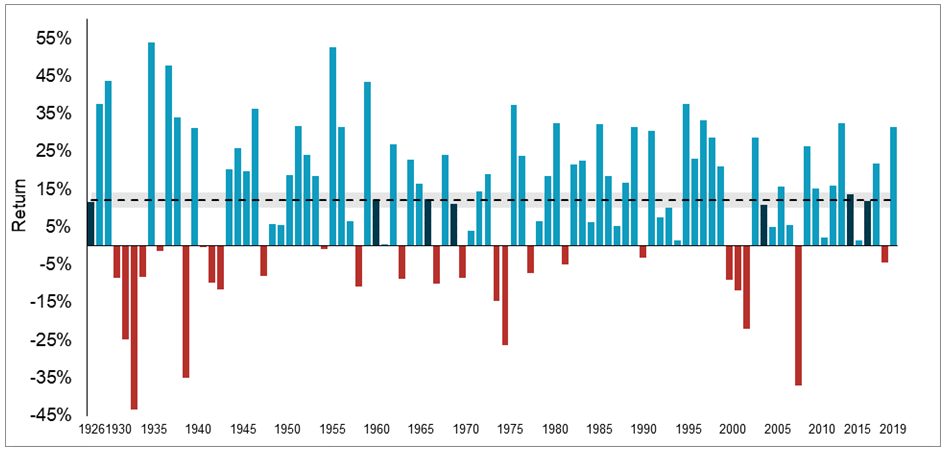

First off, it’s important to recognize just how noisy security returns are, especially stock returns. The average annual return of the S&P 500 Index from 1926-2019 was 12.09% (3), but the standard deviation of that return was 19.76%. That means that about two thirds of the time the annual return of the S&P 500 was somewhere between -7.67% and 31.85%. Which is obviously a pretty big range. Another way that we can visualize this is to simply chart the annual returns.

Annual Average Return of the S&P 500 Index 1926-2019

Data from 1926-2019. Gray area represents two percentage points above and below the S&P 500 Index’s average return of 12.09% over this period. For illustration purposes only. Indexes are not available for direct investment. Past performance is not indicative of future performance.

There’s a lot to unpack in a chart like this, but what I want to focus on is that little gray area there around the average return. This represents the area within two percentage points of the annual average return (4). What’s interesting here is how atypical an “average” return actually is. There were only 7 years where the annual return was within two percentage points of average – that’s about 7% of the time. The other 93% of the time, it was somewhere else (to put it delicately).

However, over time you tend to converge towards the average return. Over a 30 year time period, the lowest return that the SP 500 Index ever had was an annualized 7.80%, which isn’t all that bad. Again, this isn’t indicative of the market consciously making sure that you get roughly the average return, rather that the average is just… the average. Since every year is basically independent, you’re more likely to get returns close to the average than you are to get them far away from the average, and those extreme returns are reasonably randomly distributed, and will tend to cancel out over enough time.

To be clear, there is no guarantee that over the time period that you care about those differences will cancel.

And unfortunately, when investors aren’t monomaniacally focused on the long-term, they tend to lose their discipline immediately after the market drops – which just locks in the losses that they have experienced.

Focusing on the long-term doesn’t mean that stocks aren’t

risky anymore, but it does mean that we are giving ourselves the best possible chance

to capture a security’s long-term expected return.