There are a handful of times a year when certain events precipitate a market drop. So much so, that we feel it is helpful to provide perspective on why investing in the stock market is a great way to help you build your asset base so when you retire you can better generate retirement income streams to fund your lifestyle. Even in retirement, investment in the stock market is warranted since current retirement horizons will most likely last more than a few decades.

Despite not having any pressing downward concerns, by our nature we just need to wait for that next shoe to drop. It seems the trade disputes, North Korean negotiations, and internal government politics are not enough to weigh the stock market down. So, what are we beginning to hear about as the new concern? It seems the markets have had too much of a successful run and it could be time for people to start getting out of the pool.

The common refrain is:

“The market has had a good run and it’s time for it correction. So why don’t we take some off the table and wait for the dip and then go back in. While I don’t think you can time the markets, this should be clear to everyone who can see a chart.”

Granted, while I’m being a bit too cute with this quote above, I believe it captures the spirit of what is beginning to spread.

With stock indices continuing to set new highs, does this mean negative returns for stocks are on the horizon? When addressing this question, it is helpful to keep the following in mind:

- Every day, stocks have a positive expected return regardless of whether markets are at an all-time high or not.

- While expected returns are always positive, positive realized returns are never guaranteed and may deviate from expectations.

The reason we can expect positive returns, regardless of the current market level, is attributable to the mechanism by which markets set prices.

- Stock prices are the result of the interaction of many willing buyers and sellers.

- Current prices reflect the value of future cash flows expected by those buyers and sellers.

- But, there is uncertainty around these future cash flows for stocks, and investors bear the risk of potential losses.

- If the buyer of a stock views the future cash flows as more uncertain, they will likely want to pay a lower price for the stock.

- They will only transact when the price reaches a level where they expect to earn a positive return.

For these reasons, we expect stock market prices to be set to a level at which the required rate of return for investing in stocks is positive, whether the market is at a new high, a new low, or something in between. Otherwise, why would buyers in the marketplace willingly transact at a given price?

History can help illustrate this point and show us that a market index reaching an all-time high has not necessarily provided actionable information for investors.

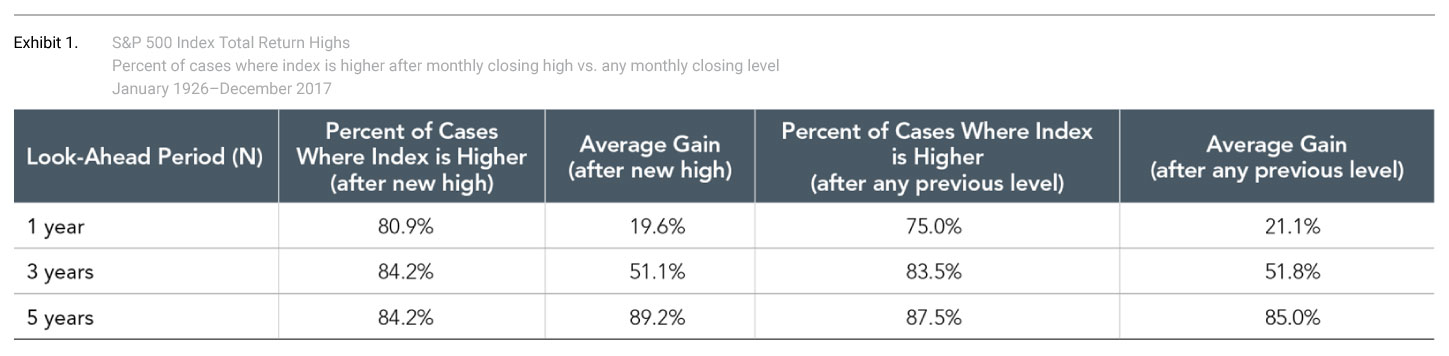

For illustrative purposes only. Average gain is a simple average of all positive returns for the 1-, 3-, or 5-year periods analyzed. S&P data © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

Exhibit 1 measures monthly closing levels of the S&P 500 Index from the beginning of 1926 to the end of 2017. Of the 1,103 months observed, almost one-third represented new closing highs for the index. This may not be surprising for some. Since markets generally tend to go up over time, new highs should be a relatively common occurrence. Considering this, it is worth posing the question: If prices increasing over time was a troubling development, what would be the point of investing at all?

This data also shows that looking ahead on a one-, three-, and five-year basis, the percent of cases when the index was higher or lower after a new market high is about the same when compared to any other previous price level. In other words, positive and negative returns tended to make up a similar proportion of returns after the fact, regardless of whether a new high was reached or not.

For example, for a three-year look-ahead period, the index was higher around 84% of the time both after hitting a new closing high as well as after any other previous level. Additionally, this data shows us that the average return experienced after those highs vs. any other level is also quite similar. For example, for the three-year look-ahead period, the average cumulative return after a new high was 51.1% vs. 51.8% for any other level. These results indicate that new index highs have historically not been useful predictors of future returns.

Another reason you should be cautious about reevaluating their approach at an all-time high is the potential opportunity cost of switching in and out of the market. Last year, the S&P 500 Index returned more than 20%, and yet 2017 started with three new market highs during the first 20 trading sessions.1The opportunity cost you paid by reacting to the new highs by selling stocks could have been substantial. There is no reliable way to predict when stock returns will be positive or negative, and while the long-term average return of the US stock market2 has been around 10% since 1926, year-to-year results often deviate markedly from the historical average. Investors looking to capture what the equity markets offer over the long term are likely well served by sticking with their approach rather than making changes based on short-term noise.

The question of whether new market highs portend a fall in stocks can often be translated to another, more general question: “Is now a good time for me to be invested?” The evidence suggests that the current state of the market is not helpful in answering this question. Rather, an appropriate answer is highly dependent upon your unique situation and their risk and return objectives. If you believe that stock market exposure is appropriate for you, a disciplined approach with a long-term view is likely a more prudent course of action than reacting to new market highs.