Both traditional and newer hybrid insurance policies carry a number of parameters and options to consider. At the most basic level, you should consider:

- How much time passes before benefits start,

- How much benefits are provided per time period,

- How long benefits are provided, and

- The total benefit pool available to be used.

There are other important considerations as well, which we will delve into.

Elimination or waiting period

First, what is the initial elimination period before benefits begin? This choice could be viewed as a deductible, with longer elimination periods serving as the equivalent of a less costly high-deductible policy.

Since many long-term care events have short durations, a short elimination period could substantially raise the cost of insurance. It may also not be necessary. In certain circumstances, Medicare or health insurance may cover a portion of the costs for short-term events.

Elimination periods in the range of two to three months may be reasonable compromises for those with sufficient assets to fund some of the initial care not covered by Medicare or other health insurance. Elimination periods up to one year may work best for retirees who can afford to fund short-term events themselves and wish only to protect themselves from the risk of more serious and costly events.

Monthly or daily amount, period of coverage, and total benefit pool

Most benefits are defined in terms of a monthly or daily maximum payable benefit amount. Determining the appropriate level depends on the cost of care in your community and your ability to partially fund some expenses in other ways. You almost must have a firm understanding of how much insurance you can afford to buy through the payment of premiums, regardless of potential future increases.

The period of coverage indicates how long benefits are available. As most policies allow the time period to be extended when less than the full periodic benefit amount is used, a key consideration for the periodic amount and period of coverage is the total benefit pool available to be used.

For instance, a $150 daily benefit provided for five years would provide maximum benefits of 150 x 365 x 5 = $273,750. Long-term care benefits up to this total amount are available. Coverage ends without further benefit payments when the total pool is spent.

Most traditional insurance policies allow for care coverage from one to five years. Lifetime coverage is rare for traditional policies, though some hybrid policies offer additional continuation of benefit riders which may allow it.

Inflation protection

Should the allowed long-term care benefit grow over time? This is an important question, as the long-term care benefits may not be received until 20 or 30 years later and long-term care costs often grow at a faster rate than overall consumer price inflation. Today’s cost of care may only be a fraction of what the future realized costs could be. Inflation protection may also add substantial costs to the insurance.

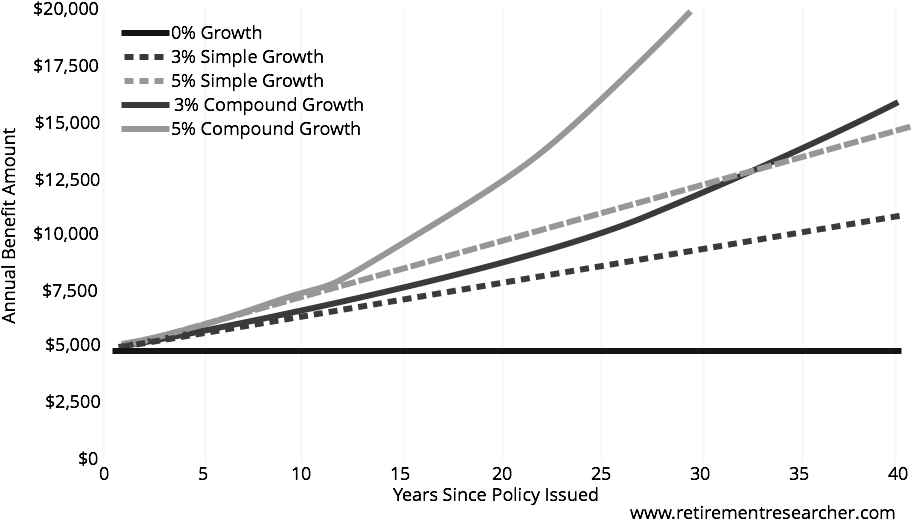

Common options for inflation include no benefit growth, a simple growth rate, or a compounding growth rate. Growth rates may be 3% or 5%.

Figure 1 shows an example of the impact of different growth rates for a baseline monthly benefit amount of $5,000. With no growth, the benefit amount remains at $5,000. With a simple growth rate, a fixed amount is added to the benefit each year. For instance, 3% simple growth adds $150 to the monthly benefit amount each year. After 40 years of coverage, monthly benefits grow to $10,850. Meanwhile a 5% simple growth rate adds $250 per year. After 40 years, the benefit is $14,750. With compounding growth, the amount of growth increases over time as the rate is applied to the latest benefit amount rather than the initial amount. With 3% compounding growth, the benefit is $15,835 after 40 years, as opposed to $33,524 with 5% compounding growth.

Figure 1: Tracking Growth for a $5,000 Monthly Benefit Using Different Inflation Factors

As you can see, it takes about 33 years for a 3% compound growth rate to catch up to and exceed a 5% simple growth rate, making the choice among these options less than obvious. Compounding growth should better reflect the pattern of cost growth in the future, but simple growth may be a more affordable option for a particular growth rate, especially as overall insurance costs rise.

The choice is also complicated because there is no way to know when you will need care and what the cost inflation will be until then. Simple growth may not be able to keep pace with long-term care costs, but it at least provides some growth relative to a flat benefit. Another option to help support a growing benefit amount over time is a provision within the contract for additional coverage to be purchased periodically.

How benefit amounts are determined and paid

Several options are available for how benefits are paid. The reimbursement method requires paying the provider and then submitting a claim for reimbursement from the insurer. The indemnity or cash methods pay the beneficiary a specific benefit amount for particular services which could be more than actual expenses.

By better matching up with actual expenses, the reimbursement method is usually the most cost effective because it will result in smaller claims. Paying an extra premium would rarely make sense as benefit amounts may exceed the actual costs for care.