This article is part of a series; click here to view Part 1.

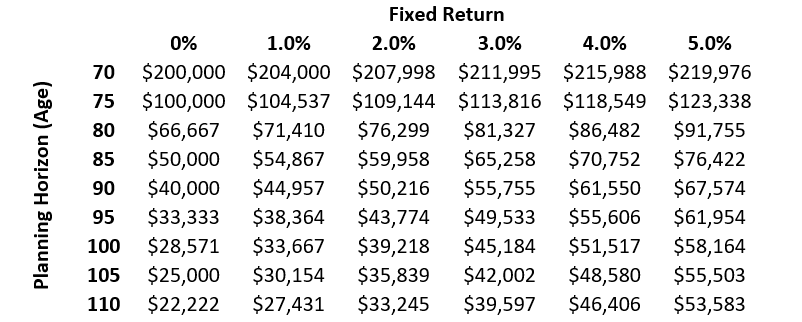

Exhibit 1.1 provides reasonable approximations for sustainable spending in retirement as it relates to a bond interest rate (or a fixed return for an investment portfolio) and a retirement longevity assumption. For a sixty-five-year-old with $1 million, the exhibit shows sustainable spending levels given both returns and longevity. The returns can express either nominal or real returns. If nominal returns, then the spending numbers would also be nominal and would not adjust for inflation. If the returns are real, however, then spending numbers are also real and would grow with inflation.

For additional information, click here to download our resource, 7 Risks of Retirement Planning.

If the retiree sought to buy a retirement income bond ladder through age ninety-five using Treasury bonds, the 3 percent yield curve assumptions suggests that the sustainable spending amount is $49,533. Again, because this is an assumption about nominal bond yields, this spending amount would not growth with inflation. As inflation is generally a positive number, real returns are less than nominal returns. With real returns the initial spending level would be less but would grow with inflation. With the 1 percent TIPS yield curve assumption, sustainable spending through age ninety-five is $38,364 plus inflation.

Exhibit 1.1 Sustainable Spending for a Sixty-Five-Year-Old with $1 Million of Assets as Based on Fixed Portfolio Returns and Longevity

The fixed return assumptions could be treated as bond yields, in which retirement income is based on building a ladder of individual bonds. In this case, the yield would reflect the average yield from the bond ladder if the yield curve was not otherwise flat. These returns could also reflect the return assumptions for a diversified investment portfolio. In this case, these returns would reflect the net return assumption after working through a series of factors.

A thirty-year TIPS ladder is as close as we can get to a real-world safe withdrawal rate for thirty years of inflation-adjusted spending. The exhibit shows that at current interest rates, this number is less than 4 percent of the initial retirement date assets. Spending more from an investment portfolio is based on a hope that a higher return arrives to sustain a higher spending rate. This is risky. It is important to note that with this bond ladder, nothing will be left at the end of the thirtieth year. The calculation is risk free for thirty years, but the possibility of living beyond thirty years must be considered. A TIPS ladder does not hedge longevity risk. Longevity risk can only be managed by assuming a more conservative planning age with a lower probability to outlive, and then spending less to stretch the asset base out over a longer retirement horizon.

This is an excerpt from Wade Pfau’s book, Safety-First Retirement Planning: An Integrated Approach for a Worry-Free Retirement. (The Retirement Researcher’s Guide Series), available now on Amazon.