Traditional safe withdrawal rate literature regularly makes the assumption that retirees will choose a withdrawal rate that will leave precisely no wealth after the final withdrawal in the thirtieth year of retirement. Retirees cling to the inflation-adjusted withdrawal amounts, which leaves them playing a game of chicken as their wealth plummets toward zero.

In addition, these hypothetical retirees do not make any adjustments for the fact that as their thirtieth year of retirement approaches, they are increasingly likely to live longer than thirty years. The classical assumptions also present retirees with no particular desire to leave a bequest, an estate, an inheritance, or whatever you may like to call it.

The objective of the classical studies is to get a handle on what is the maximum sustainable withdrawal rate from a portfolio of volatile assets over a thirty-year retirement period without being worried that something will still be left at the end. When we talk about using a safe withdrawal rate, we are describing a situation in which remaining wealth is potentially allowed to fall to $0 at the end of the planning horizon.

While the safe withdrawal rate approach is meant to typically provide leftover funds at the end of the time horizon, the analysis will be different if we specifically incorporate a desire that our worst cases still preserve assets at the end of the time horizon.

I aim to investigate how withdrawal rate decisions may change when retirees specifically incorporate a desire to leave a bequest, which I will summarize here as either maintaining the nominal value of retirement date wealth at the end of the thirtieth year, or maintaining the real value of retirement date wealth at the end of the thirtieth year.

The value of wealth may decline and rebound in the interim, as I am only checking the value of wealth after the thirtieth year.

I am using the same assumptions as described in my discussion of William Bengen’s SAFEMAX:

- Withdrawals at the start of the year,

- Annual rebalancing from a 50/50 portfolio of large-capitalization stocks and intermediate-term government bonds,

- A 30-year retirement, and

- Inflation-adjusted withdrawal amounts.

Data is from the SBBI Yearbook.

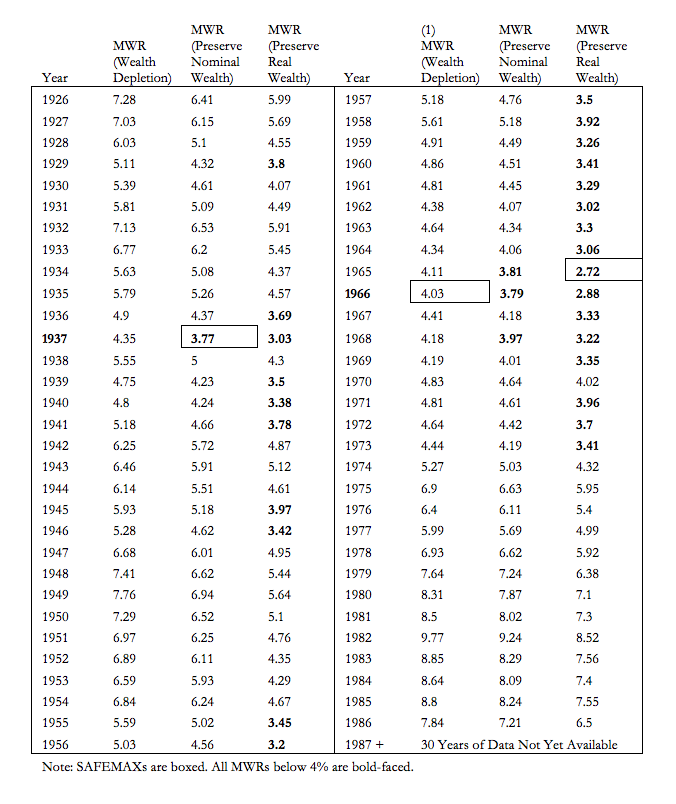

Exhibit 1 shows the maximum sustainable withdrawal rates by retirement year for three scenarios:

- The classic case in which wealth is depleted after thirty years,

- The case in which the nominal value of retirement date wealth is preserved after thirty years, and

- The case in which the real inflation-adjusted value of retirement date wealth is preserved after thirty years.

With the classical wealth depletion assumption and a 50/50 asset allocation, the worst-case scenario withdrawal rate (SAFEMAX) of 4.03% fell to the 1966 retiree. Switching to an objective to preserve nominal wealth after thirty years, the SAFEMAX falls to 3.77%.

The 4% rule would have been too aggressive to preserve nominal wealth at four historical starting points (though after thirty years of inflation, that wealth may not have a whole lot of purchasing power left).

When someone says they want to preserve the value of their wealth, they are probably implicitly thinking in terms of preserving the real purchasing power of their wealth, even if they do not articulate as much. People tend to suffer from “money illusion,” in which they think in terms of nominal dollars when they really mean to be considering the real purchasing power of dollars.

The next column in the exhibit shows the maximum sustainable withdrawal rates that will preserve the real value of wealth after the thirtieth year. The 4% withdrawal rate accomplishes this in 57% of the historical simulations (thirty-five out of sixty-one rolling periods).

The SAFEMAX for this case happened for a 1965 retiree who could only use 2.72% to preserve the real value of their retirement date wealth.

Exhibit 1

Maximum Sustainable Withdrawal Rates (MWRs)

Cases: (1) Wealth Depletion, (2) Preserve Nominal Value of Retirement Date Wealth,

and (3) Preserve Real Value of Retirement Date Wealth

For 50/50 Asset Allocation, 30-Year Retirement Duration, Inflation Adjustments

Using SBBI Data, 1926-2015, S&P 500 and Intermediate-Term Government Bonds

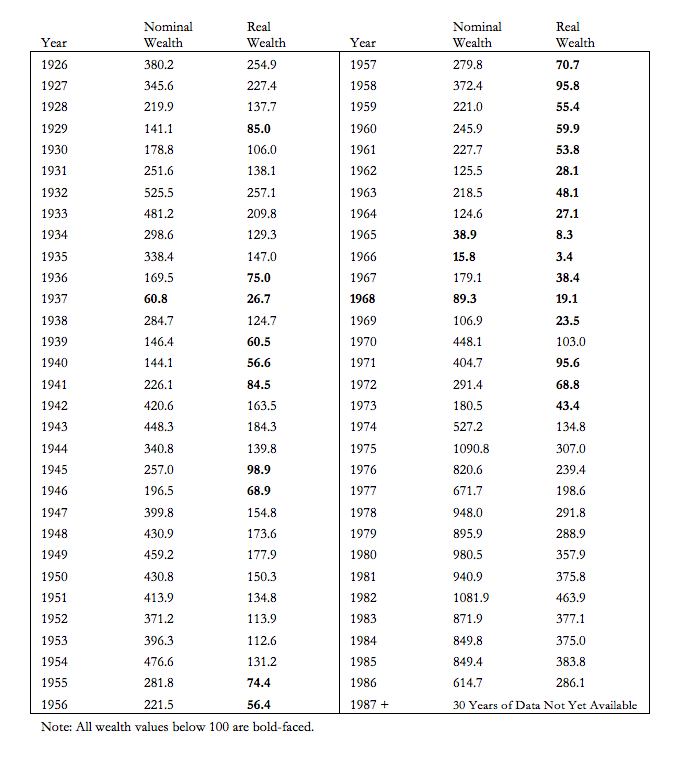

Exhibit 2 expresses this information in a different way by identifying the amount of wealth remaining after thirty years in both nominal and real terms (retirement date wealth = $100) when using a 4% withdrawal rate with a 50/50 asset allocation and all of the other standard assumptions.

As I mentioned before, the 1966 retiree got the SAFEMAX of 4.03%, and we can see that the real value of their wealth after thirty years is $3.4. Since a withdrawal of $4 will be taken in year thirty-one, the 4% rule fails over a thirty-one-year horizon for the 1966 retiree.

On the other end of the spectrum, as we can now calculate outcomes for the 1982 retiree as well, we can see the growth of their wealth if they used 4% withdrawals. In nominal terms, their wealth would have grown to more than ten times its retirement date value, and even in real terms the value of their wealth more than quadrupled.

In the 57% of cases that real wealth grows after thirty years of spending with the 4% rule, this table better clarifies the degree of this wealth growth. One could also calculate the current withdrawal rate after thirty years as the $4 real spending divided by the remaining real wealth. The withdrawal rate is higher when wealth is less and lower when wealth is greater.

When meeting a spending goal with the 4% rule, the withdrawal rate for the 1982 retiree after thirty years has fallen to 0.86%. On the other hand, for a 1966 retiree the withdrawal rate would rise to 100% for the next year beyond thirty.

Exhibit 2

Remaining Wealth After 30 Years (Measured in Nominal and Real Terms)

Using a 4% Withdrawal Rate and Retirement Date Wealth=100

50/50 Asset Allocation, Inflation Adjustments for Withdrawals

Using SBBI Data, 1926-2015, S&P 500 and Intermediate-Term Government Bonds