An important simplifying assumption in William Bengen’s research is that retirees spend constant inflation-adjusted amounts throughout retirement. This may be at odds with the spending patterns of many retirees. An exploration of the data should give us an idea of how people actually change their spending during retirement.

A well-known early example of spending changes over time for retirees can be found in Michael Stein’s 1998 book, The Prosperous Retirement: Guide to the New Reality. Stein says retirement happens in three phases, popularly known as the Go-Go, Slow-Go, and No-Go years of retirement.

He found retirement spending to be greatest in the early active phase of retirement through age seventy-five. In these Go-Go years, discretionary expenses for things such as travel and restaurants are high, and retirement spending tends to keep pace with inflation.

Between the ages of seventy-five and eighty-five, retirees enter a transition phase (Slow-Go) in which they become less active and reduce discretionary expenditures. Spending no longer keeps pace with inflation and may even decline on a nominal basis.

Finally, after age eighty-five, retirees enter into the No-Go years, which are signified by a much more modest spending budget whose growth will generally also trail consumer price inflation.

The idea that spending declines throughout retirement obtained further support in an article Ty Bernicke published in the June 2005 issue of the Journal of Financial Planning. Bernicke used evidence from the Consumer Expenditure Survey (CES) to show that those aged 75+ spend less than those aged 65-74, who in turn spend less than those aged 55-64 (population-wide averages by age group).

To account for spending decreases, Bernicke described a tug of war for retirees: Though their spending increases over time with inflation, they voluntarily spend less as they age. For instance, retirees may lose the desire or ability to go on vacations or restaurants as they age, resulting in fewer expenditures.

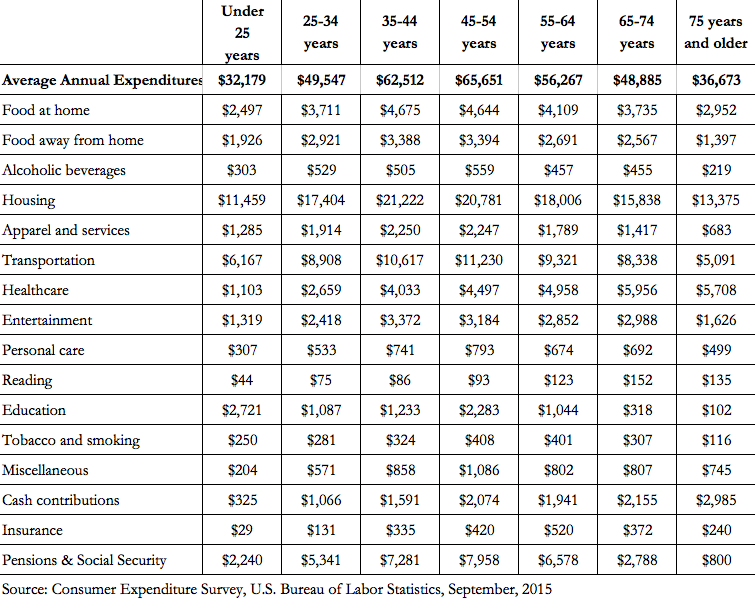

Exhibit 1 provides updated data from the most recent CES, conducted in 2014. With the updated data, we can observe the trends highlighted by Bernicke.

In terms of average annual household expenditures, homes with a reference person aged 75 and older spent 25% less than households aged 65-74, and households aged 65-74 spent 13.1% less than 55-64 year olds. The exhibit also provides spending broken down into various categories.

Comparing those 75 and older to the younger retiree age group (65-74), we see substantial decreases in spending for food away from home, alcohol, apparel and services, transportation, entertainment, and education. As most have left the workforce, contributions to pension funds and Social Security decreased substantially as well. The only category that increased was cash contributions, which represents gifts to family, friends, or charity.

Exhibit 1: Spending in the Consumer Expenditure Survey, 2014

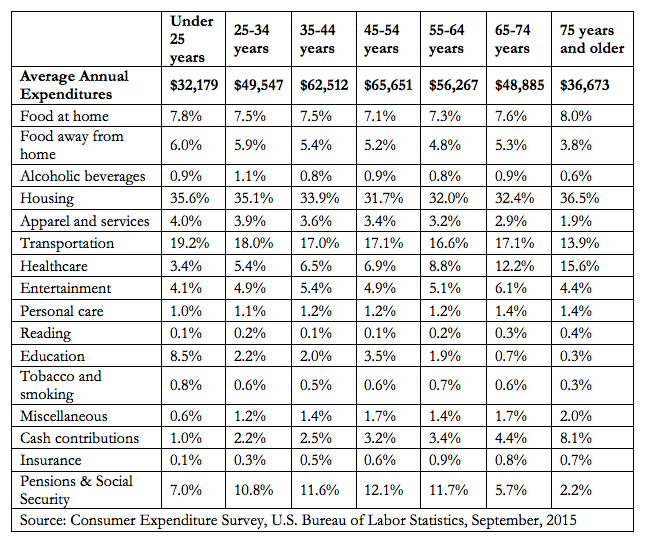

The following exhibit provides a different view of the same data, with expenditure categories broken down by the percent of overall household expenditures by age group. Expenditure shares grow for ages 75 and older in the categories of housing, health care, and cash contributions.

For these averages, Bernicke’s suggestion about retirement spending holds; expenditures decrease in a number of discretionary categories. Housing and health care expenses may not always decline, but the average growth in these categories is more than offset by expenditures in other categories.

Suggesting that retirees should plan for constant inflation-adjusted spending may overestimate the required retirement savings that many households will require for a successful retirement.

Exhibit 2: Spending Shares in the Consumer Expenditure Survey, 2014

Another issue is that even if spending declines on average, certain households may experience rising expenditures with age and would be ill-suited by planning with a general assumption that spending will decline. The CES data represents average trends, but conservative plans will call for preparations beyond what happens in the average outcome.

That being said, any conclusions drawn from the CES data should be tempered considerably. For instance, inflation is higher in some spending categories than others. The previous analysis misses this because it considers spending between different age groups in the same year.

The CES data shows that health care spending, for instance, tends to rise over time for given age groups even after adjusting for inflation. Health care has a higher inflation rate than overall consumer price inflation. Ten years later, when the 65-74 group joins the ranks of 75+, one should expect higher health care spending. By looking at different age groups in the same year, we miss this. It is important to follow the same households over time to be confident that spending declines with age.

Another issue is that even if spending declines on average, certain households may experience rising expenditures with age and would be ill-suited by planning with a general assumption that spending will decline. The CES data represents average trends, but conservative plans will call for preparations beyond what happens in the average outcome.