After releasing our unofficial “official” launch of the RISA™ we followed up with a survey asking you if you felt the results were accurate; did the RISA™ “capture the essence of your style?”

If we needed to get something right, this is it!

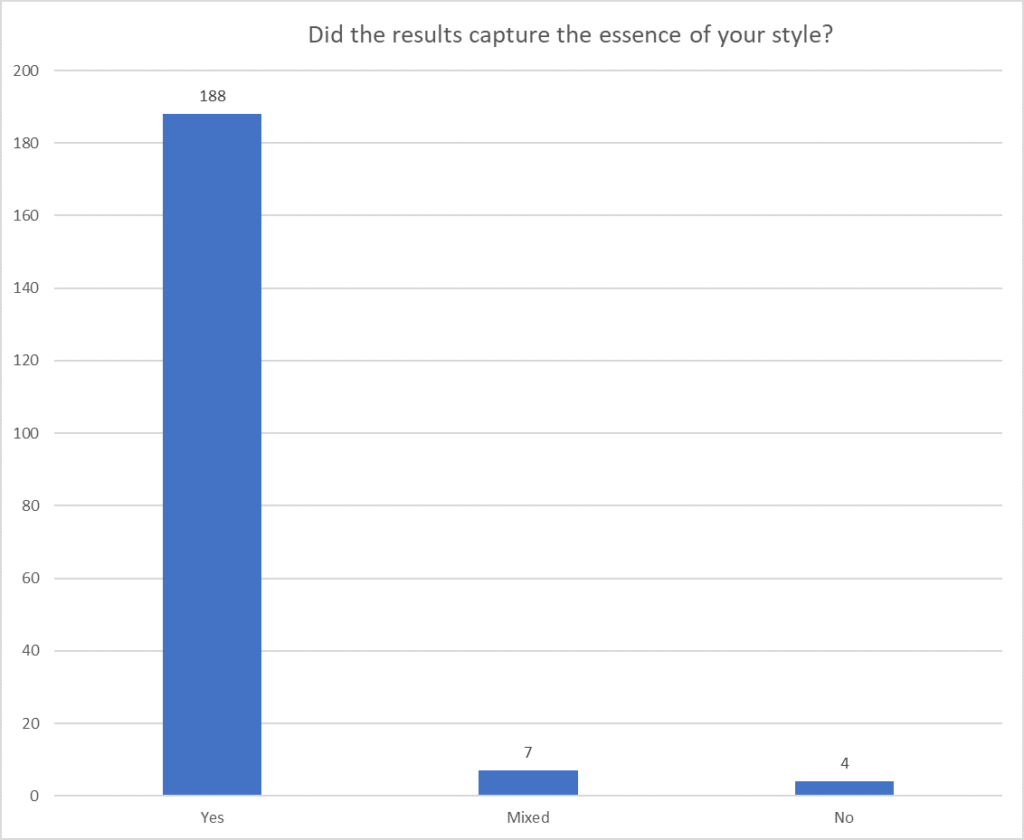

I asked everyone this opened-ended question. After reading the responses, I sorted the answers into three groups; Yes, Mixed, No.

As you can see from the results, we were very happy with the outcome. While we have a statistical library of information detailing reliability and validity with your retirement income style, it is always great to simply ask, “Did it work?” and hear a positive response. Whenever over ninety percent (90%) of your participants feel good about the results, so do we!

Here are some reactions from our participants:

- Pretty accurate capture.

- I found that the RISA profile captured and presented my investment and retiring style in a manner probably better than I know myself. It was very helpful in understanding the choices I have made and projecting future financial decisions.

- Yes. good questions, made me think

- Yes – It explained my discomfort of adopting either a purely Total Return or Protected Income approach. It rationalized clearly why I am primarily a Time Segmentation person blended with some Total Return and some Protected Income.

- Yes – and surprised me a bit in some instances, which was thought provoking & valuable

- Yes, very much so. Provided validation of what I considered my retirement income preferences are, and insight into the most appropriate implementation strategies. I came away with a sense of ‘what I have to work with’ in terms of style, biases, and strengths/weaknesses which need to be considered in developing, implementing, and sticking to a retirement income plan.

- Yes, I found this to confirm my suspicions about my style. I lean towards “Safety-First” and “Optionality”. It is nice to have an outside, objective source confirm this.

- I value the self-efficacy, self-awareness, numeracy, financial bias and inertia. People need to know this to better understand themselves!

- I think so. I knew I was a bit of a “safety-first” type, but didn’t realize how much. I’ve been conflicted for some time now about whether or not to buy an annuity, or, since I would only need to withdraw 1-2% of my investment portfolio, keeping the assets in the markets. I’ve not been able to commit to one or the other choice. However, I think that with this RISA look, I may get closer to a decision (safety first).

- Yes. The results confirmed my style and the current make-up of my retirement portfolio.

- Yes, I was shocked to realize that I’m a little more safety-first oriented than I would have thought, thanks to the nuanced differences between questions that, at first glance, seemed redundant. This will prove immediately helpful for asset allocation and rebalancing going forward and prompts me to re-read Dr. Pfau’s book entitled “Safety First.”

- Yes, it confirmed what I suspected as to where I stood on the dimensions and what products I should look at for retirement income.

- Came out pretty dead on

- Yes. I think it covered all aspects very nicely.

- Yes. Overall, certainly seemed to match my behavior and nicely learned a bit more which will help.

- Yes. they captured the essence of my style.

- The results definitely captured my style. I thought every area was on the mark in terms of my concerns and preferences were concerned.

- Yes, I believe it was pretty representative.

- The RISA confirmed my interest in covering my essential costs through fixed income sources. It also captured the major strategies I am considering to supplement my fixed income. For me, this validation was very useful.

- On the nose! Thanks for the opportunity to use it.

The mixed and negative reactions, while few (6% of the total), circle around potential next steps as opposed to shortcomings of the actual RISA™ assessment. For example, one participant responded that the RISA™ “didn’t really capture my investing style (bond/stock ratio), but otherwise quite apt.”

Another issue involved our treatment of how an existing pension may affect your next steps. These, especially the pension issue, have been further addressed in the updated version of the RISA™. A few others pointed out that they wished the recommendations for next steps were more precise.

While we feel the RISA™ is a great first step to understanding your Retirement Income Style, you should still “run your numbers” to know how to overlay your RISA™ profile with your fiscal reality. Once you know your style, you can play off your strengths and better analyze a more focused set of next steps. We do recommend a Funded Ratio Analysis to determine if you have adequate funding levels within your retirement plan. This will apply to a vast majority of RISA™ participants. Over time, we will continue to refine the RISA™ but for now we are ecstatic that over ninety-four percent (94%) of our initial participants felt the results were accurate. To review overall satisfaction with the RISA™, click here.

Next, read I’ve taken the Retirement Income Style Awareness™ Profile. What’s next?