Many people approach retirement planning as if they’ll monotonically spend the same amount year after year throughout their retirement. This assumption certainly makes the planning process significantly simpler, but it’s not realistic. Our spending desires (and needs) change through time.

Spending Needs (and Desires) Change Through Time

Many people want to take advantage of their early retirement while they are still spry and energetic enough to travel, or just make up for lost time on their (expensive) hobbies that they put to the side before retirement.

However, as we get older, we tend to slow down and get more sedentary. This often translates to a decreased desire to spend. And then towards the end of our live there are a number of medical expenses that we will likely need to contend with.

Introducing the Retirement Spending Smile

David Blanchett’s 2014 article, “Exploring the Retirement consumption Puzzle” puts some data behind this consumption pattern by looking at household survey data to track their inflation adjusted spending through time.

Blanchett observes a “retirement spending smile” that varies slightly for retirees with different household spending levels. But the general form is reasonably consistent.

As we can see below, retirees tend to spend more in early retirement, followed by a dip in their spending as they age, and then their spending picks up again to deal with increased medical expenses towards the end of their life.

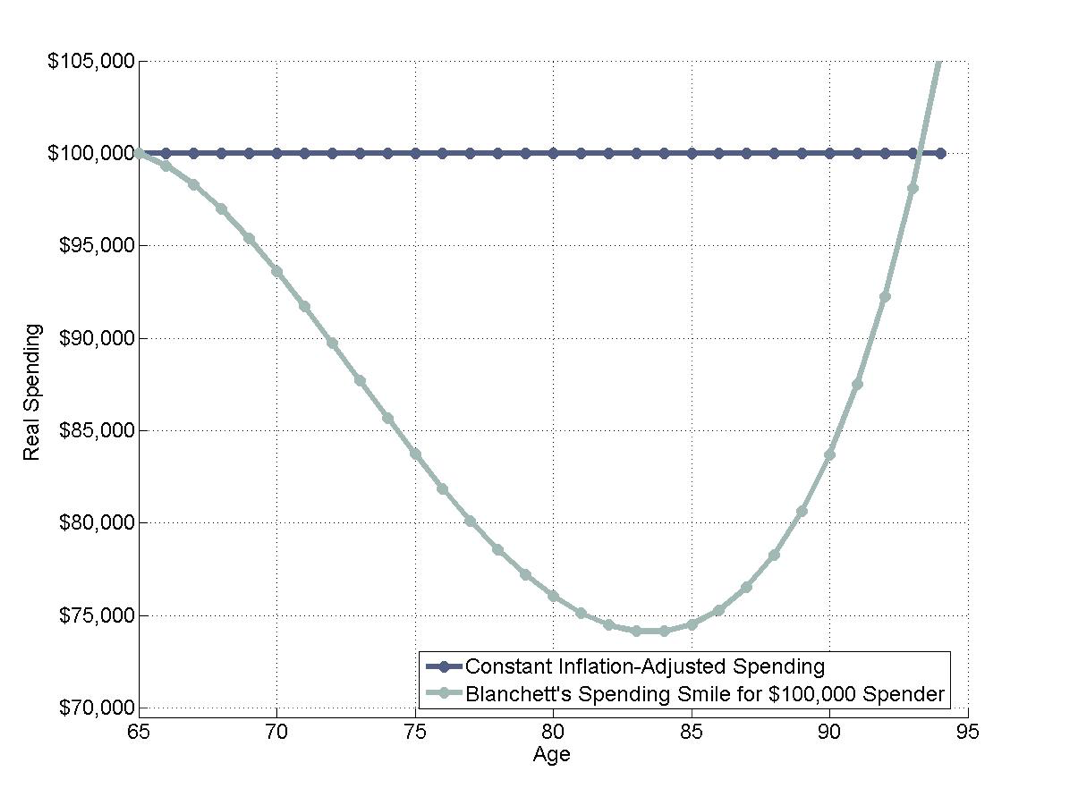

Blanchett’s Retirement Spending Smile

For illustration purposes only. The Estimated Path of Real Retirement Spending for a $100,000 Initial Budget at 65 vs. Constant Inflation-Adjusted Spending Strategy. Based on data from Blanchett, David. 2014. “Exploring the Retirement Consumption Puzzle.” Journal of Financial Planning 27 (5): 34–42

On average, this household, with an initial spending goal of $100,000 per year, can expect to experience declining real expenditures through age eighty-four, when real spending reaches a trough of $74,146. This reflects a nearly 26% drop in real expenditures.

After this point, average real expenditures increase, though they do not necessarily exceed their initial retirement levels until retirees reach their mid-nineties. I produced these calculations using Blanchett’s own equation, which relates changes in annual retirement spending to age and the expenditure target at the start of retirement.

Blanchett observes that the spending smile reflects the same types of outcomes we have described thus far. At the start of retirement, retirees spend more as they enjoy traveling, eating out, and other types of discretionary expenses. As they continue to age, retirees tend to slow down and spend less.

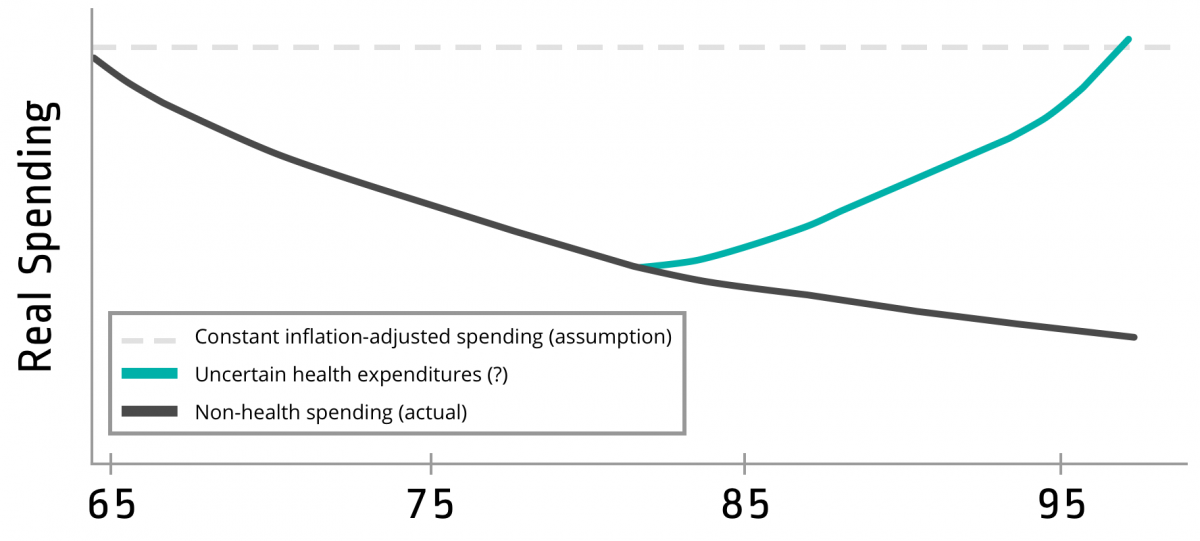

However, while discretionary expenses are declining, health costs tend to rise, and at some point later in retirement, these rising health costs offset reductions in other spending categories. Exhibit 2 provides a further illustration of this process.

Understanding the Path of Real Retirement Spending

For illustration purposes only.

Implications of the Retirement Spending Smile

The assumption of constant inflation-adjusted spending, according to Blanchett’s article, will lead individuals to over-save for retirement. The easiest way to understand this is to simply explore historical sustainable spending rates for different retirement spending patterns.

To do this we’ll compare a scenario where we use a constant inflation adjusted spending approach with one where we take into account the Retirement Spending Smile and adjust our spending through time. Specifically, we’ll be focused on the highest sustainable initial spending rate for each of these approaches through time, assuming a 50/50 asset allocation and a 30 year retirement.

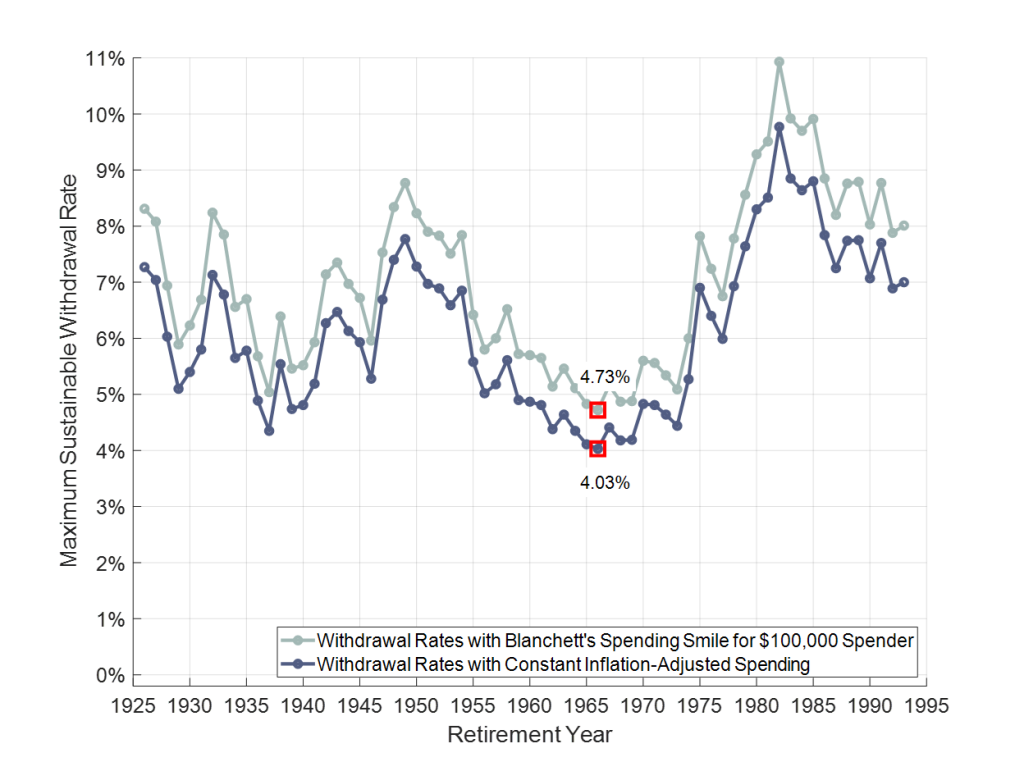

For illustration purposes only Maximum Sustainable Withdrawal Rates for 50/50 Asset Allocation, Allocations comprised of the S&P 500 Index and Intermediate Term Government Bonds, 30-Year Retirement, Inflation Adjustments, No Fees. Using SBBI Data, 1926-2022, S&P 500 and Intermediate Term Government Bonds. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results.

As we can see, there is a relatively consistent difference in the initial spending rate that each approach can support.

One of the important ways to quickly assess the different approaches is to look at the worst-case scenario – the lowest sustainable spending rate for each approach in our example.

For the constant spending approach, the worst-case sustainable spending rate was 4.03%. In other words, if you took out 4.03% of your portfolio in the first year of your retirement, and then adjusted that amount for inflation for the next thirty years, there were no historical periods where you would have run out of money over the time period of the study.

On the other hand, an initial distribution rate of 4.05% would have failed at least once (admittedly, this doesn’t give us much of a guide as to what an optimal distribution rate for our own retirements will be, but it does help us frame the downside risk.)

With the retirement spending smile approach, we see a much higher worst-case sustainable spending rate. In this case, the worst-case initial spending rate rose to 4.73%, which represents an increase in the initial distribution rate of 17% – just by using a more appropriate retirement spending model.

For a retiree basing their spending on these historical worst-case numbers, the retirement smile pattern would allow retirement to begin with almost 15% less accumulated wealth than if they assumed a constant spending pattern (as is typical).

This makes clear that retirement spending patterns are an important component of deciding on a sustainable spending rate. Constant inflation-adjusted spending is a simplifying and conservative assumption. While we prefer conservative assumptions to aggressive ones, we don’t need to unduly penalize ourselves – especially with assumptions we know are less realistic.

And choosing not to incorporate the retirement spending smile is one of those situations where you could be unduly penalizing yourself – especially if you are planning a distribution rate close to the historical worst case scenario.

Everyone, and every retirement, will be different, but the data around the retirement spending smile is pretty clear. Most people reduce their spending in the middle of their retirement.