When considering your retirement plan, it’s helpful to think of Social Security not just as a safety net, but also as an investment. How and when you claim your benefits can have a profound effect on your financial outcomes in retirement. In this article, we’ll dive into different approaches to claiming Social Security, and see how they compare when thinking of your benefits as part of your overall retirement investment strategy.

Early vs. Delayed Social Security Benefits

One of the key decisions you’ll make in retirement is when to start claiming your Social Security benefits. You can begin as early as age 62, or delay until age 70, with each option leading to different financial outcomes. Choosing when to claim affects both the annual benefit amount and the pressure placed on your investment portfolio.

Let’s look at a hypothetical example where you want to spend $60,000 per year in retirement, and a investment portfolio of $800,000. The amount of Social Security benefits you receive will depend on when you claim them, and your portfolio will need to cover anything that isn’t covered by Social Security.

Below, we’ll explore two different scenarios:

- Claiming at Age 62: In this case, you receive a smaller Social Security benefit of $22,500 per year but begin receiving it earlier. Your portfolio will need to cover the remaining $37,500 per year to meet your $60,000 spending goal.

- Delaying until Age 70: Delaying increases your annual Social Security benefit to $39,600, but you’ll need to fund your entire $60,000 living expenses from your portfolio until you reach age 70.

The table below compares these scenarios:

| Scenario | Start Age | Annual Social Security Benefit | Portfolio Withdrawal Required |

| Claiming Early (62) | 62 | $22,500 | $37,500 |

| Delaying (70) | 70 | $39,600 | $60,000 (until 70) |

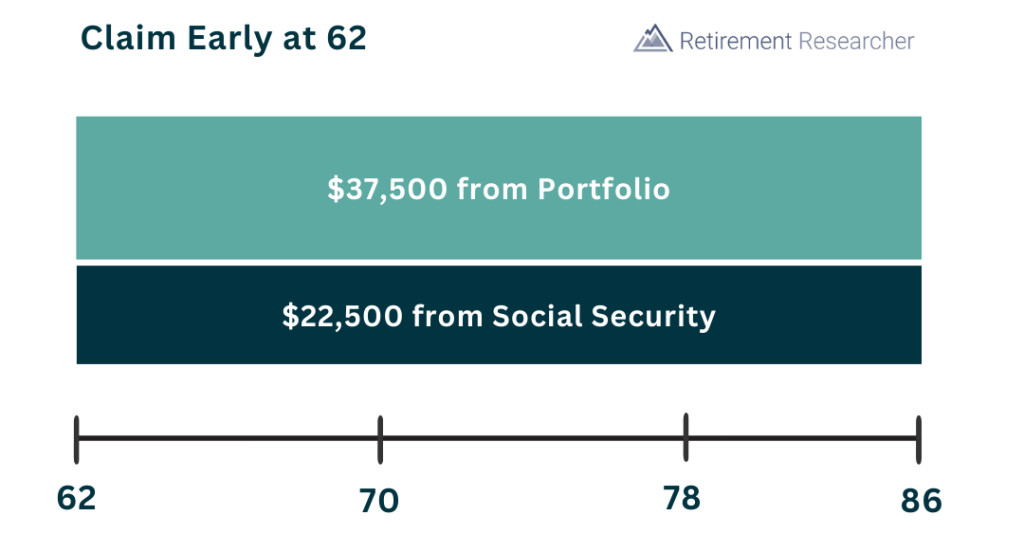

Portfolio Spending with Early Claiming

In the first scenario, you decide to claim Social Security at age 62. This provides an annual benefit of $22,500, which means you need to withdraw $37,500 from your investment portfolio each year to meet a $60,000 spending need.

The advantage here is that you start receiving money earlier, which reduces the immediate need for large portfolio withdrawals. However, the lower Social Security benefit means you’ll have to continue relying more heavily on your portfolio throughout retirement, which will increase the distribution rate and may put more pressure on your investments over time. In this scenario, your initial portfolio withdrawal rate is approximately 4.7% ($37,500 / $800,000), which increases the risk of depleting your assets, especially during periods of poor market performance.

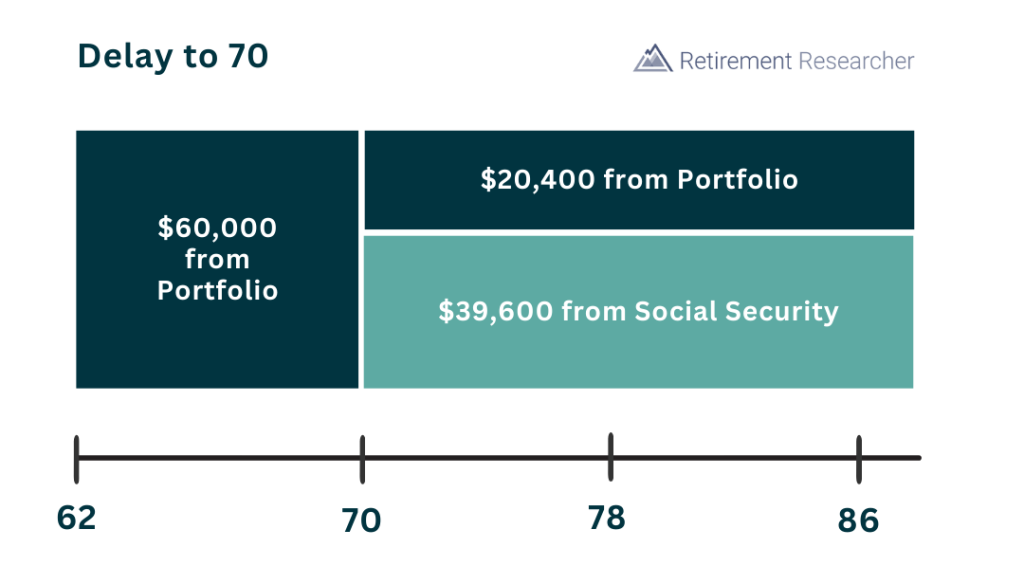

Delaying Benefits Until Age 70

In the second scenario, you delay claiming Social Security until age 70, which results in a significantly higher benefit of $39,600 per year. To cover your spending needs between ages 62 and 70, you fully fund your lifestyle from your portfolio, withdrawing $60,000 per year.

Once you begin receiving Social Security at 70, your annual withdrawals from the portfolio drop to $20,400. This can help preserve your portfolio over the long term, especially if you live beyond average life expectancy.

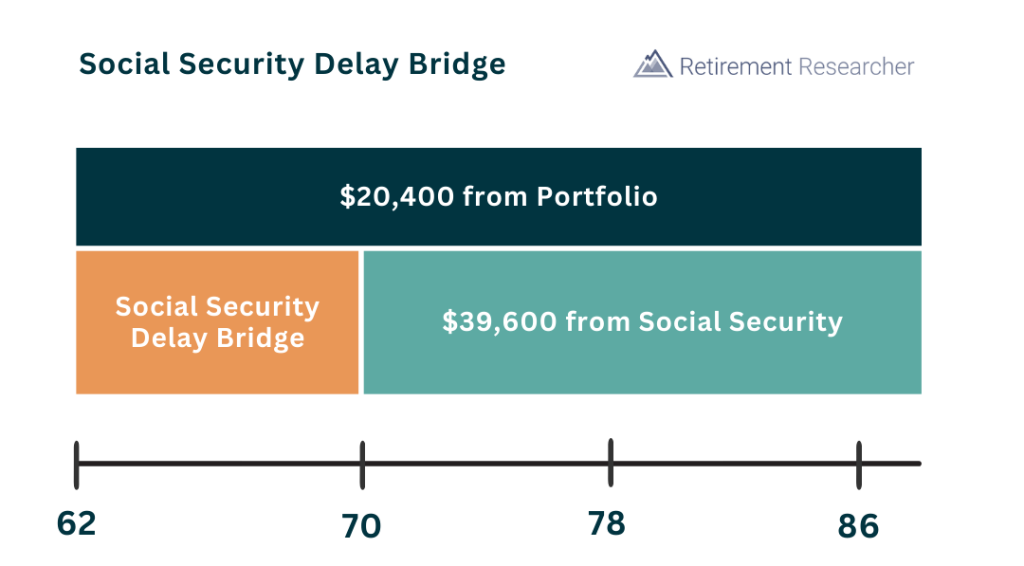

Using a Social Security Delay Bridge

A third strategy involves creating a Social Security Delay Bridge. This strategy involves setting aside a portion of your portfolio specifically to cover your spending needs between ages 62 and 70, allowing you to delay claiming Social Security without increasing your annual withdrawals.

By using a bridge, you essentially pre-fund the gap years – typically with a bond ladder – which allows you to take advantage of the higher benefit at age 70 while avoiding excessive withdrawals early on. While this does mean that you will reduce the size of your investment portfolio, it also means that you will reduce the magnitude of your sequence of returns risk as you are not spending from your volatile investment portfolio.

The cost of creating a Social Security Delay Bridge will depend on the current market conditions, as well as how much income you would like to receive. But as an example, say you would like to create a TIPS bridge that will provide $39,600 per year (the amount of your Social Security benefits if you claim at age 70) starting at age 62. We’ll also assume that this bridge will earn a 0% real interest rate (it is important to note that this is a very conservative assumption, and it is very likely that a real bridge would provide a positive real yield).

This means that at age 62 you would need to set aside $316,800 ($39,600 x 8 years) to purchase the TIPS Social Security Delay Bridge.

With the bridge strategy, you withdraw $20,400 from your portfolio each year throughout retirement, as the bridge funds the gap until age 70. The required withdrawal rate to meet the spending goal throughout retirement is now:

Withdrawal Rate = ($60,000 – $39,600) / ($800,000 – $316,800) = 4.22%

In this example, delaying Social Security allowed the withdrawal rate to drop from 4.69% to 4.22%.

This improves retirement sustainability. The investment portfolio is less likely to be depleted and more income remains available through the higher Social Security benefit in the event that the portfolio is depleted. In other words, running out of financial assets is both less likely to happen and less damaging when it does happen.

Allowing for the same probability of portfolio depletion, spending could be increased by more than 11% to $66,682 in order to use the same 4.69% withdrawal rate as when claiming early. Then, 76% more income is still available than otherwise in the event of portfolio depletion. This is the permanently enhanced lifestyle possible with Social Security delay.

Impact of Social Security Delay on Retirement Withdrawal Strategies

The key takeaway here is that delaying Social Security can act as a valuable investment in your retirement security. The additional income from delaying benefits reduces your reliance on portfolio withdrawals, which can be especially beneficial if market returns are lower than expected or if you live longer than average.

| Impact of Social Security Delay on Retirement Withdrawal Rates | Claim at Age 62 | Claim at Age 70 |

| Spending Goal | $60,000 | $60,000 |

| Social Security Benefit | $22,500 | $39,600 |

| Portfolio Withdrawal | $37,500 | $20,400 |

| Investment Portfolio | $800,000 | $800,000 |

| Set Aside for Social Security Delay | $0 | $316,800 |

| Remaining Portfolio | $800,000 | $483,200 |

| Withdrawal Rate | 4.69% | 4.22% |

The magnitude of the difference would be larger if the client’s spending goal and asset base were smaller relative to the Social Security benefits, and vice versa.

For this strategy to work effectively, the overall spending goal cannot be too large with respect to the size of the financial portfolio. For instance, if the portfolio was $300,000, there would not be enough to create the delay bridge. Otherwise, a large enough portfolio will allow for Social Security delay to reduce the required portfolio withdrawal rate. And if the portfolio is not large enough, it is more of a reflection that the overall spending goal is not realistic, rather than an indictment against Social Security delay. Though, severely underfunded retirees without alternatives may be forced to claim Social Security early because they cannot otherwise fund themselves through age 70.

Conclusion

Delaying Social Security benefits can improve the sustainability of a retirement income plan or increase spending power while maintaining the same success probability. Initially, retirees need to withdraw more from their portfolio until Social Security begins, but they can reduce withdrawals once the benefits start. However, relying solely on a volatile investment portfolio is not foolproof, as a poor sequence of returns early in retirement could deplete the portfolio and lock in losses. To mitigate this risk, retirees can carve out assets from the main investment portfolio to create a Social Security delay bridge. Alternatively, retirees may use other buffer assets, such as home equity through a reverse mortgage or life insurance, to construct this bridge.

Social Security is a critical component of retirement income, and the decision of when to claim benefits can have a significant impact on your financial future. By considering different claiming strategies, such as early claiming, delaying, or using a Social Security Delay Bridge, you can better align your retirement income with your goals and risk tolerance.

By thoughtfully considering when to claim Social Security, you can significantly enhance your retirement security. Delaying benefits isn’t always easy, but the potential rewards—reduced reliance on your portfolio, increased lifetime income, and greater flexibility—can make it a powerful tool in your retirement planning. Each person’s situation is unique, so it’s crucial to evaluate your options carefully and choose the approach that aligns best with your goals and financial circumstances.