Everyone is always looking for the perfect investment strategy. But investing, like everything in life, is about making trade-offs. It seems like there are a near infinite number of ways to invest, but they all fall into one of two broad categories: active or passive investing. Active investing means you are trying to predict the future and beat the market. Passive investing means you aren’t – you are taking what the market is giving you.

I’ve spent a lot of time talking about how active management doesn’t work. But I want to look at the issues most investors face with passive management. When you say passive management to most investors, they automatically translate that to “index funds.”

Index funds dominate the passive management landscape (though they are not the entirety). But just because there’s no way to guess which active managers will do well in the future doesn’t mean index funds don’t have problems themselves.

Before we go any further, I want to be clear on something – the problems with actively managed funds are much worse than the problems with index funds. It’s the equivalent of picking apart the problems with Michael Phelps’s butterfly stroke compared to, well, mine.

Sure, you can find problems with his stroke – his elbow might be a centimeter out of alignment, or his kick may be a tiny bit off – meanwhile, I’m in the next lane trying not to drown. It’s the same with investing. The problems of index funds pale in comparison to the problems of active management.

But we still need to understand what those problems are – we need to understand the trade-offs we are making.

The problems index funds face all stem from the same place. Indices weren’t designed to be trading vehicles. They were designed to tell you how well actively managed funds were doing. There’s nothing wrong with this – in fact, it’s incredibly important.

But it means indices were not designed to be good investment vehicles. They had the job thrust upon them.

It makes sense indices were used. They’re relatively unbiased and objective representations of specific asset classes, and they (generally) aren’t controlled by the fund managers.

This is a crucial point – the fund manager was turning over control of what their fund looked like to a third party. This made it obvious index funds were not trying to beat the market – they were looking to invest in the market.

There are two (and a half) big problems with index funds:

- The Reconstitution Effect

- Purity of Exposure (and the monomaniacal focus on tracking error)

It’s Just Too Easy

The first of these problems, the reconstitution effect, is easy to understand. Everyone knows what an index owns. They try to own exactly what is in the index they track, in exactly the same weight. So, this means when the index reconstitutes (essentially rebalances), everyone knows exactly what you are going to buy and sell and they know exactly when you are going to do it.

Now, I’ve said some mean things about traders, but they aren’t stupid. This is like playing poker with your cards facing out. It’s not hard for traders to figure out what they should be doing.

They’re going to bid up the price of the stocks being added to the index, and they will sell off the stocks being dropped from the index. And this is exactly what we see in the data.

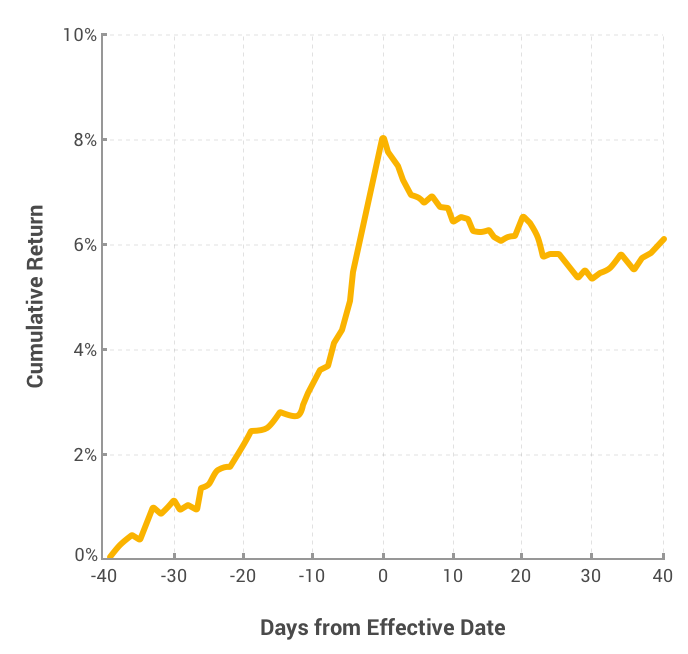

Equal Weighted Additions Relative to the S&P 500 Index 2000-2016

In US dollars. Source: Center for Research and Security Prices, University of Chicago, and Standard and Poor’s. The information shown here is derived from such indices. For more on index reconstitution see Chen, Noronha, and Singal (2004) [Equity] and Dick-Neilsen (2012) [Fixed Income]. Past performance is no guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Here, we’re looking at the returns of stocks right around the time when they were added to the S&P 500 Index since 2000 (the effective date is the date they were added to the index). Looking at the chart, it’s clear what happened.

As it became obvious a stock was going to be added to the index, more and more people were buying the stock on the assumption all the funds tracking the index would have to buy the stock. In other words, the index funds bought the stocks that were added for inflated prices.

And while the prices did stay higher (there is a lot of money indexed against the S&P 500 index), they dropped relative to where the index funds had to buy them.

And this is with the S&P 500 index – there are no set rules for what stocks will be included or dropped. It’s essentially a large cap active fund in disguise. Think about what would happen with a more deterministic index where everyone knows exactly how the index is put together.

Purity of Exposure

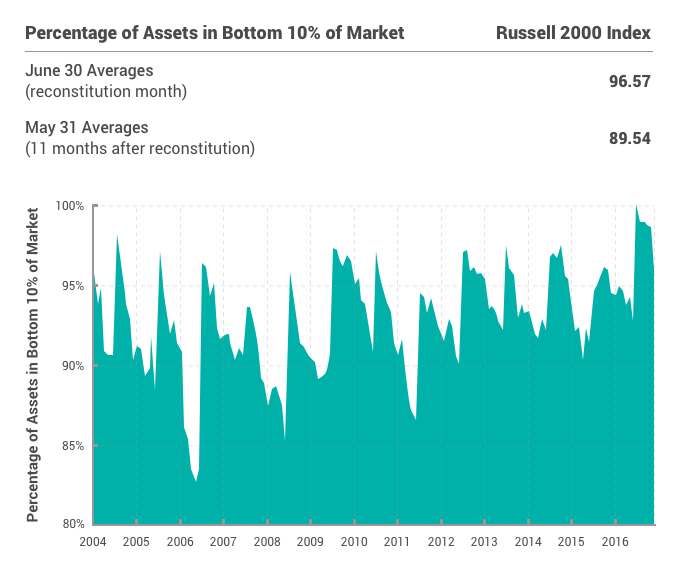

You also need to worry about the purity of risk exposure you get with index funds. Since most indices only reconstitute once a year, they have a full year to bounce around before everything gets pulled back into alignment. Let’s say we want to capture the small cap premium.

Well, the obvious answer is to go out and buy a small cap index fund, and one of the biggest names in the space is the Russell 2000 Index. This tracks the smallest 2000 companies of the largest 3000 companies in the US market. That is, companies 1,001 through 3,000 by size.

It’s a pretty good representation of the US small cap asset class – especially when you look at it right after it reconstitutes. But what happens as the year moves on?

As of December 31, 2016. Month-end values from December 2003-December 2016. The information shown here is derived from the index. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results.

Right after the index reconstitutes in June, on average, about 97 percent of the index weight is concentrated in the smallest companies. Eleven months later, that drops to less than 90 percent. These are averages, so some years are better than others, but overall you end up with progressively worse exposure to the asset class.

If you’re building your portfolio around capturing specific risk factors, this is a problem. You want to make sure you are always targeting the risk factors – not just right after the index reconstitutes.

This impurity of exposure is the result of having to follow specific benchmarks with a laser-like focus on minimizing your tracking error.

How Much Do You Trust Your Fund Manager?

The need for an outside, observable index to manage against is the result of an important split in passive management – high- versus low-trust investing.

Most passively managed funds are low-trust funds – as an investor, you want to be sure the manager is doing exactly what they are supposed to be doing. Index funds work perfectly for this. That monomaniacal focus on tracking error is the way to see if the fund is doing what they say they are.

But there are firms out there that use high-trust passive management (and there are certainly a lot more out there using high-trust passive management than you should actually trust). These firms are taking what the market gives them and not trying to predict the future like a traditional index funds, but they don’t follow an index.

Breaking this link with a commercial index means they have the flexibility to design their portfolio to capture the risk factors they want, and to be smart about how they manage the portfolio.

This is where the trust comes in – you’re giving them the freedom to screw up. Index funds can screw up through bad implementation, but you know what they are trying to do.

High-trust funds are out there actually (I almost said actively) making decisions about what will and will not be in the portfolio. They decide what rules will define the portfolio, what sort of screens to use, and what the actual implementation and trading strategies look like. Any one of these steps can cause problems for the portfolio, but they are also places where the high-trust manager can add value.

With an index fund, you are basically watching over the manager’s shoulder. They’ve told you exactly what the fund is going to be doing. This is both their strength and their weakness. There is an objective, outside measure of what they are doing, but that measure is not focused on creating the best investment vehicle possible.

High-trust managers are focused on creating an effective investment vehicle, but you can’t monitor them quite as effectively. They can do things with the portfolio an index fund just can’t. But you need a monstrously high bar for this level of trust. You need to be sure they are going to deliver what they say they will.

There are no perfect investments. Everything is a trade-off, so you need to be comfortable with the trade-offs you are making. And while index funds are in many ways a safer bet than actively managed funds, they come with their own set of issues.