I am often asked whether it is worth the cost to hire a financial advisor. After all, they charge you money to make you money. People say they can listen to the news and know where and how to invest, so, “Wouldn’t I be better off just keeping that fee for myself?” That is an excellent question with an answer that depends on many factors.

Good financial planning decisions extend well beyond where and how you invest. Two major research efforts have attempted to quantify how good financial decision making can enhance one’s lifetime standard of living. It is important to understand what this research means, because this may not always equal a higher portfolio return in the short term.

The research identifies how good decision making can enhance sustainable lifetime income on a risk-adjusted basis. The ability to spend more than you could have otherwise can be interpreted as meaning that the assets earned a higher return net of taxes and fees to make that spending possible.

In the field of finance, the term “alpha” identifies how a fund manager can combine securities into a portfolio that provides excess returns to investors above the appropriate related benchmark index for those investments on a risk-adjusted basis. In simple terms, achieving alpha means earning more money than expected.

This generally is achieved through either timing market trends correctly or picking winning individual securities. If a fund manager charges a fee of 1% of assets under management, but then produces alpha of 2%, the fund owner enjoys an overall net gain of 1%. After fees, they’ve earned 1% more than they would have had they invested directly in the benchmark index.

In practice, it is very difficult to achieve alpha from market timing and security selection, which explains the rise of indexing. Low cost index funds generally perform better than the majority of actively managed funds seeking alpha, at least after accounting for management fees.

(Side note: many investors don’t even realize they’re paying fees on mutual funds since they don’t appear on portfolio statements. It’s important to look for the expense ratio and any loads which are being charged at the time of purchase or sale.)

After fees, alpha is often negative for actively managed funds. Those who understand this point can dramatically simplify their portfolio by filling it with well-diversified low-cost index funds. In this way, investing is basically commoditized these days. Financial advisors who only focus on selecting investments will really struggle to add value.

Do not misunderstand me — there is immense value in comprehensive financial planning and good financial decision making. It’s important to remember and easy to forget that the end goal of comprehensive financial planning goes beyond choosing investments.

As you can see, the term alpha has been shown to be insufficient when it comes to financial planning, and these articles both seek to replace it with a term that represents more than merely beating the market. Vanguard proposes the term “Advisor Alpha” to explain this broader concept. David Blanchett and Paul Kaplan at Morningstar settled on “Gamma.”

Vanguard’s Advisor Alpha

Vanguard developed their Advisor Alpha concept in 2001. This infographic shows their overall estimate for Advisor Alpha is 3% on a net basis (4% less an assumed 1% fee). In the introduction, they explain their objective is to shift the focus away from “traditional beat-the-market objectives” (i.e. traditional alpha) toward what they view as the “best practices of wealth management.”

These best practices are separated into several categories that focus on tax efficiency, costs, risk management, and making good investment decisions:Overall net impact of good advice: about 3%

Suppose a good comprehensive financial advisor who does all these things charges a fee of 1% of assets under management. An investor who is capable of doing all of the above on his or her own is able to keep all of these advantages. However, an investor who doesn’t know how to effectively implement the above, or who wishes to instead devote their energy elsewhere, misses this extra Advisor Alpha. Even though they saved the 1% advisory fee, they end up worse off.

Justin Wagner from Vanguard offers the following example. Suppose the overall market return is 8%. Without good financial decision making, the combined impact of fees, taxes, and poor investment decisions is around 4%. This leaves a net return of 4% to the investor. However, for someone working with a capable advisor, they eliminate poor investment decisions, minimize taxes, and only pay the 1% fee, leaving a net return of 7%. That is the Advisor Alpha. The value added by good advice can greatly exceed the fees.

Vanguard provides greater details in their full-length whitepaper on this topic.

Morningstar’s Gamma

David Blanchett and Paul Kaplan at Morningstar created a similar study about the value of good decision making. Their results are not exactly the same, as many assumptions must be made regarding good financial decisions and the impact of poor investment decisions. The Morningstar research is more directly focused on how retirees can achieve higher income, which they call gamma. They left out issues like behavioral coaching, and included other matters like dynamic retirement spending. Full details can be found in their whitepaper, “Alpha, Beta, and Now… Gamma”

The dimensions for improving financial decisions considered in their paper are broken down into several issues, along with how a naïve investor might approach each issue and how an improved outcome could be achieved with the guidance of a professional.

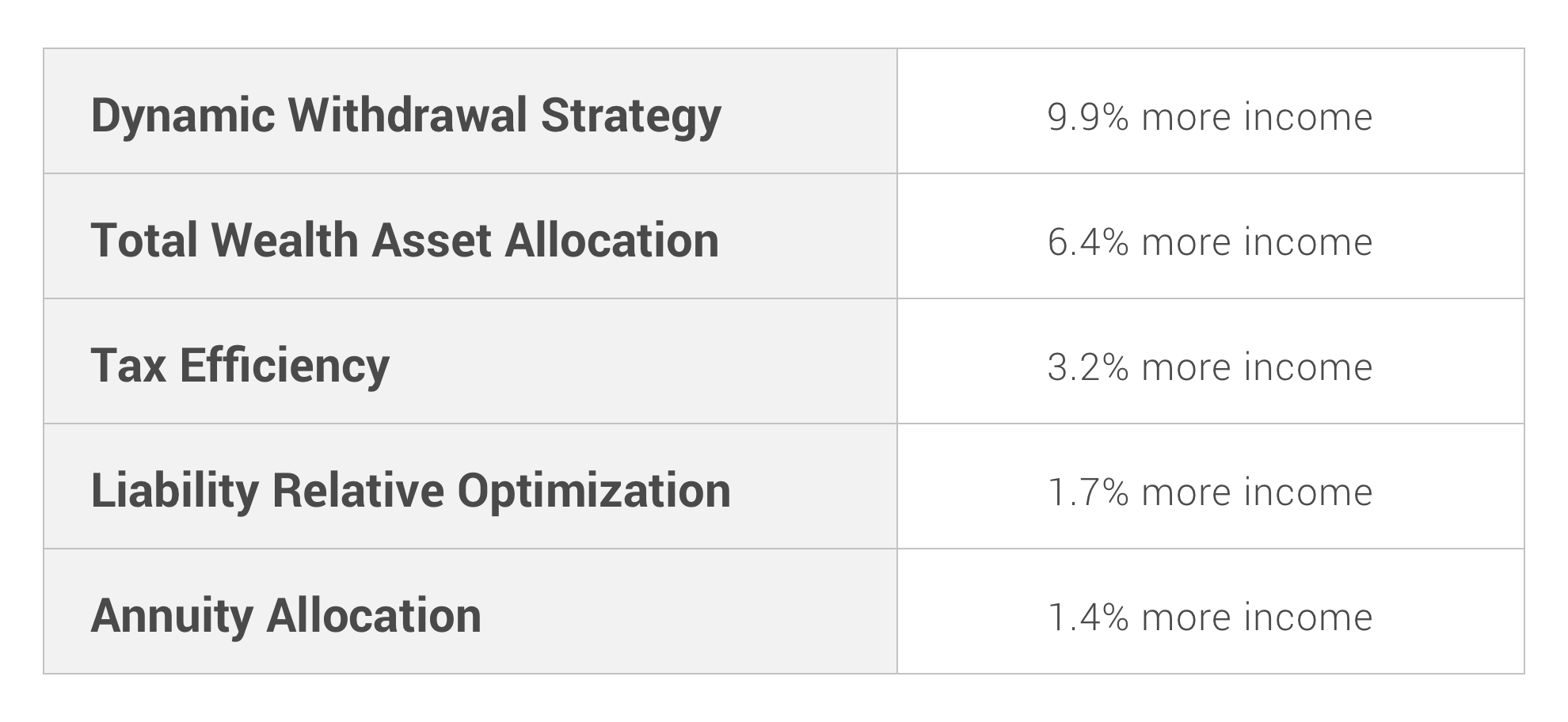

(1) Total Wealth Asset Allocation

The issue: Making asset allocation decisions after considering total wealth including human capital

Naïve investor: Makes asset allocation decisions without considering the role of lifetime human capital.

Improved Outcome: Calculate the present discounted value of lifetime earnings which will be saved. Determine the characteristics of lifetime income in terms of whether it is more bond-like or stock-like. Consider this as an asset in your portfolio and then figure out the asset allocation for the financial portfolio in order to obtain the final overall desired asset allocation for wealth.

(2) Dynamic withdrawal strategy

The issue: Making withdrawal decisions using a variable spending strategy which updates spending to keep a similar probability of failure for the remaining time horizon in retirement.

Naïve investor: Uses the 4% rule. Takes out 4% at retirement, and then increases that amount by inflation in subsequent years for as long as possible until wealth is depleted.

Improved outcome: Dynamic decisions based on a circular process. Every year, determine retirement horizon, asset allocation, and maximum withdrawal percentage for a given target probability of failure. Repeat annually to determine spending.

(3) Annuity Allocation

The issue: Using product allocation to devote some financial assets to purchase guaranteed income products may improve outcomes

Naïve investor: Views annuities as a gamble on dying too soon and ignores them as a retirement income option.

Improved outcome: View annuities as insurance against outliving one’s wealth by relying on the guaranteed income for life. Allocate part of the financial portfolio to an income annuity at retirement, while also keeping the same overall amount invested in stocks. In other words, part of the allocation to bonds in the retirement portfolio is transitioned into an income annuity.

(4) Tax Efficiency Through Asset Location and Withdrawal Sequencing

The issue: Maximizing tax efficiency by locating assets in the most tax efficient places and withdrawing assets in a more tax efficient manner.

Naïve investor: Ignores these issues by keeping the same asset allocation for both tax-deferred and taxable accounts, and then withdrawing proportionately from each account in retirement.

Improved outcome: Efficient asset location is to fill tax-deferred accounts with bonds, while stocks would be used in taxable accounts as much as possible. Efficient withdrawal sequencing is to first spend down taxable accounts, and then spend down tax deferred accounts.

(5) Liability Relative Optimization

The issue: The true risk for a retirement portfolio is not the standard deviation of the asset portfolio, nor is it the performance of the asset portfolio relative to peers. Rather, it is the risk that you won’t be able to meet your spending goals.

Naïve investor: Makes asset allocation decisions without regard to spending goals by focusing instead on single-period Modern Portfolio Theory concepts.

Improved outcome: Make investment decisions specifically with spending liabilities in mind. This could result in a portfolio with a lower expected return and/or higher volatility than a more traditional one, but it might do a better job meeting lifetime spending needs. Adding a liability creates a different efficient frontier with portfolios that would have previously seemed suboptimal. For instance, TIPS might not play a role in mean-variance optimization, but it might do a better overall job meeting spending needs, especially in high inflation environments.

By making these improved financial decisions, retirement income can be increased dramatically. The improved outcome scenario comes out 22.6% ahead of the naïve investor.

That doesn’t even consider Social Security. David also discusses optimizing the Social Security claiming decision, which could raise retirement income by another 9%. Now we are talking about a 31% increase.

Without Social Security, here is the breakdown of how improved decisions can improve outcomes from the baseline:

How much is this worth in alpha terms? In other words, how much would portfolio returns need to be increased to support a 22.6% larger spending level? The answer is that over a 30-year period, those starting with a 4% withdrawal rate would need to earn 1.59% more per year as alpha (in the median case), a difficult task indeed, to increase their income by this amount. This is the “gamma-equivalent alpha.”

Just the Tip of the Iceberg

These studies are naturally somewhat limited in what they can examine quantitatively. Financial advisors add value in many ways that are harder to quantify. With retirement, declining cognitive skills associated that come with aging will make it increasingly difficult for one to self-manage investment and withdrawal decisions. For households where one person takes primary responsibility for managing finances, surviving household members will be especially vulnerable to making mistakes when they outlive the primary financial decision-maker. Developing a strong relationship with a trusted financial planner can help in both regards.

Financial advisors can also support other wealth enhancements through estate planning guidance, insurance selection (life, long-term care, etc.), and other types of tax minimization strategies.

Conclusions

Can an advisor charging a 1% fee provide enough value to justify the fee? It depends on the answers to two questions:

(a) Do you have the time, energy, interest, knowledge, emotional discipline, and desire to implement all of these decisions on your own?

(b) Are you working with a comprehensive financial planner who does more than just manage investment portfolios and is capable of implementing good financial planning decisions?

If you have the time, interest, energy, knowledge, emotional discipline, and desire to do this on your own, then you would make an excellent advisor. If your advisor is less than capable, you might be better off saving yourself the 1% or taking your business elsewhere.

If the answer to (a) is no, and to (b) is yes, then it is worth considering that both of these studies demonstrate how working with a financial advisor can lead to net gains. It doesn’t take much to improve your standard of living through better decision making, even after accounting for any fee related to planning advice.