We are really fond of the Funded Ratio because it allows us to provide a numerical picture of your retirement income plan. In our retirement income optimization process, you can create a framework by providing your preferences for your financial objectives and the subsequent ways you want to fund them with essential and discretionary expenses.

We are really fond of the Funded Ratio because it allows us to provide a numerical picture of your retirement income plan. In our retirement income optimization process, you can create a framework by providing your preferences for your financial objectives and the subsequent ways you want to fund them with essential and discretionary expenses.

This is the key to transitioning from investing for accumulation to investing for distributions.

In addition, this framework allows you to provide earmarks for needed reserves- your rainy day money. As you saw from our previous article, Understanding the Funded Ratio, a funded ratio of greater than 100% (i.e., 1.0) implies that the present value of your current and future assets is greater than the present value of your current and future liabilities.

This is an essential litmus test that helps you determine whether you need to take greater risks with your assets, reduce your current risk levels, amplify your retirement objectives, or better align your retirement expectations.

The Funded Ratio is used to determine the present value dollar amounts of your goals, assets, and liabilities and quantifies any gaps between your assets and liabilities by matching your stated preferences with your economic reality.

We will be able to determine:

- Are you overfunded or underfunded relative to your retirement needs and objectives?

- Do you have enough and can you prudently sustain your portfolio as you distribute assets from it?

- How much investment risk do you need and how can you earmark investable assets into other more reliable strategies?

The Funded Ratio is a great way to determine your options regarding how to best allocate your funds to efficiently provide your retirement income needs, so let’s look into each of these questions:

1) Are you overfunded or underfunded relative to your retirement objectives?

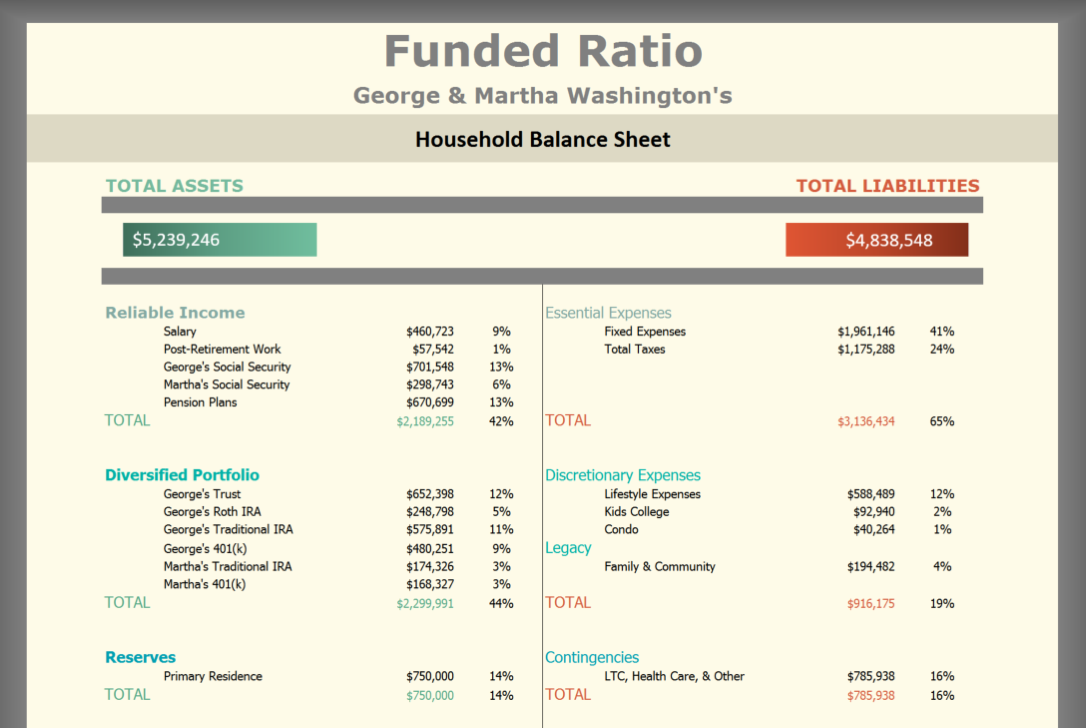

As noted in the above image, George and Martha have $5.2 million in assets. Notice how this combines both their current and future values of their expected income streams in today’s dollars.

As noted in the above image, George and Martha have $5.2 million in assets. Notice how this combines both their current and future values of their expected income streams in today’s dollars.

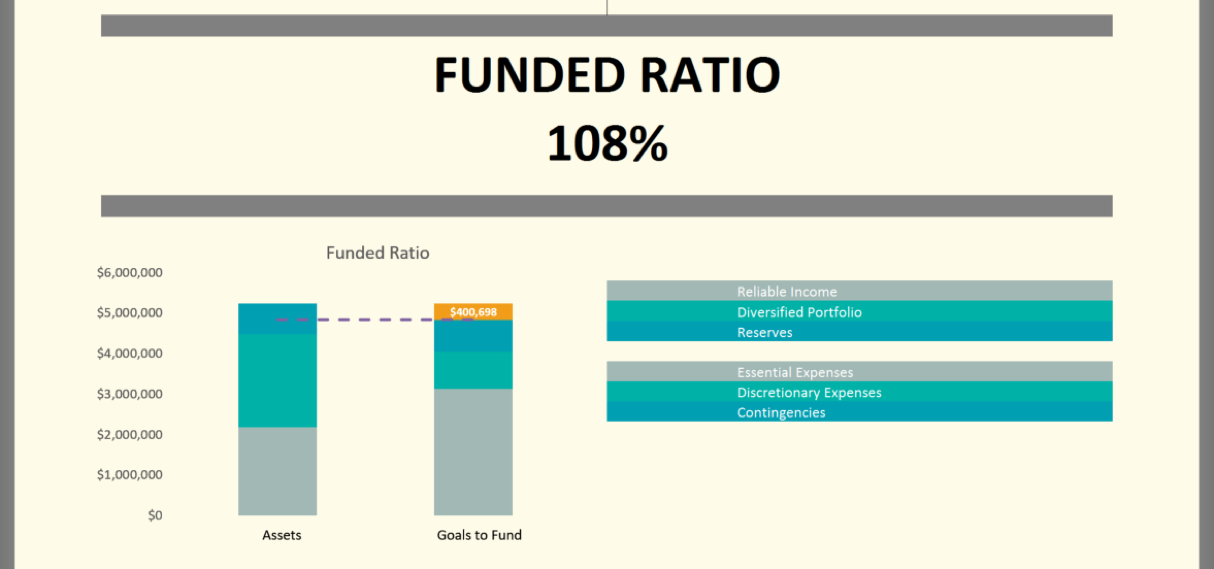

The present value of their future liabilities is $4.8 million. This implies that if George and Martha could convert all of their current assets and future income streams into cash immediately and use it to pay off all of their current and future obligations, they would have an asset surplus of $400k ($5.2M – $4.8M = $400k).

They are “overfunded” by 108% ($5.2M/$4.8M= 108%). This means that they currently have more than enough to meet all of their future obligations and financial goals.

While there is no “magic” funded number, you want to provide yourself a sufficient cushion since you will not likely convert all of your assets to cash (or even be able to). We like to see Funded Ratios that are 120% and above if you wish to maintain significant market risk to your assets.

While there is no “magic” funded number, you want to provide yourself a sufficient cushion since you will not likely convert all of your assets to cash (or even be able to). We like to see Funded Ratios that are 120% and above if you wish to maintain significant market risk to your assets.

2) Do you have enough and can you prudently sustain your portfolio as you distribute assets from it?

In this particular example, George and Martha can choose to distribute assets from their portfolio in order to maintain their desired distribution levels into their retirement.

However, because their Funded Ratio is 108%, they are significantly exposed to market volatility. If their investment assets were to drop by 15% from $2.3M to $1.9M, then their funded ratio would drop to 101%.

This would imply that they have just enough to get by. This has significant implications for the degree of investment risk they can prudently take.

3) How much investment risk do you need and how can you earmark investable assets into other more reliable strategies?

While the Funded Ratio is an aggregate score for your overall assets as aligned with your overall future income needs, we can further examine this score to see how well your assets align with your different types of funding needs.

The different types of income funding needs are broken up into three categories:

- essential expenses,

- discretionary expenses, and

- contingency expenses.

Ideally, you want to line up your essential expenses from reliable income sources, discretionary expenses from your diversified portfolio, and contingency expenses from your reserve assets.

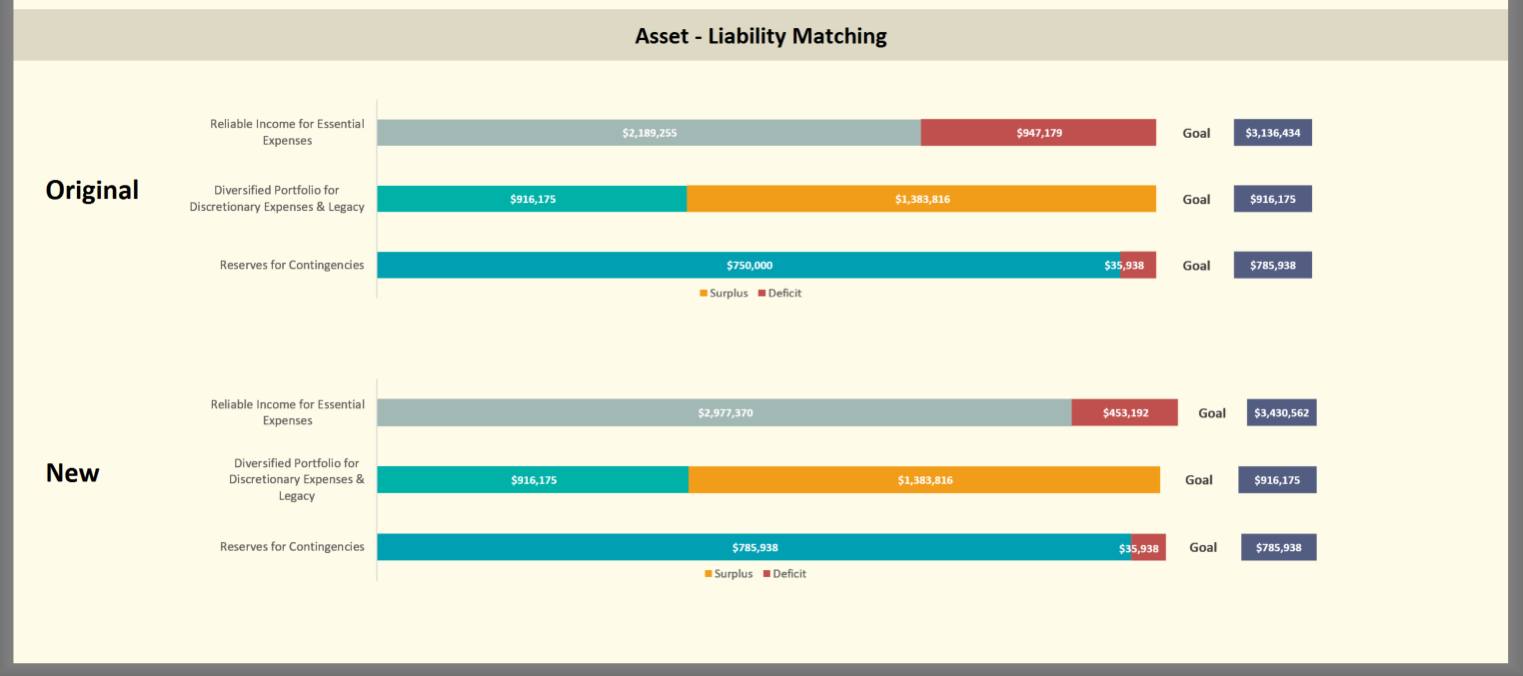

In this example, we can see that while George and Martha have a Funded Ratio of 108%, they have a shortfall within some of their funding categories.

While George and Martha have a surplus of $1.38M in terms of being able to fund their discretionary expenses, they have a slight shortfall with their contingencies spending of $36k. They also have a significant shortfall with funding their essential expenses of $947k.

The Funded Ratio better allows them to see what they need to do in order to closely align their retirement income needs with the different available funding sources.

For example, in order to better cover their essential expenses, George and Martha can use some of the asset surplus from their diversified portfolio and purchase bond ladders, income annuities, and/or consider other forms of reliable income.

This need for alignment will also stress to George and Martha the benefits of maximizing financial planning strategies such as delaying Social Security benefits.

With the Funded Ratio, George and Martha can run various breakeven scenarios and assess how the strategies impact their funded ratio score.

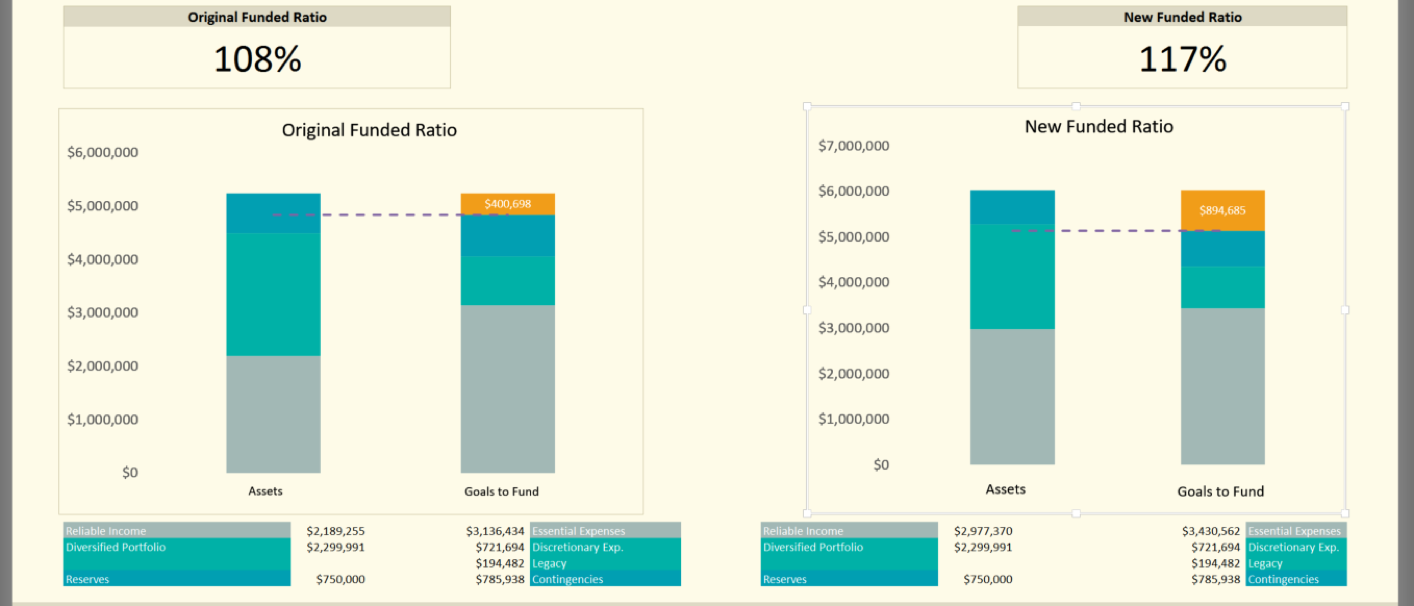

In this example, George and Martha were able to allocate a portion of their assets to more reliable income streams (e.g., immediate annuity and bond ladders). This allows them to reduce their shortfall of reliable income to essential expenses from $947k to $453k while also increasing their overall funded ratio (108% vs. 117%).

In this example, George and Martha were able to allocate a portion of their assets to more reliable income streams (e.g., immediate annuity and bond ladders). This allows them to reduce their shortfall of reliable income to essential expenses from $947k to $453k while also increasing their overall funded ratio (108% vs. 117%).

With reliable income streams further accounted for, George and Martha could potentially maintain their current portfolio allocation into retirement because they have allocated more reliable income streams to fund their essential expenses. Investment risk is more of a preference than a need at this point.

Because they have better allocated their retirement income streams across different sources, they can better weather market downturns and become less reliant on the stock market for retirement success.

With the Funded Ratio, you can assess how prepared you are for transitioning your investment portfolio and overall assets to maximize your retirement distribution while maintaining your overall net worth. You can intelligently run sensitivity analysis to determine your optimal strategy allocation among your reliable income sources, diversified portfolio, and reserve needs.

Furthermore, you can use the Funded Ratio to continue to tweak your retirement income plan and assess those modifications in a much more effective manner.

Want to find out what your Funded Ratio says about your retirement preparedness? Learn how you can get your own Funded Ratio Analysis by starting your 7-day free trial on the Retirement Researcher Academy.