There was a time when your retirement was often paid for by your employer. In many organizations, if you met the age and years of service requirements, you knew exactly what your retirement income from your employer would be for the remainder of your life. For most non-unionized private sector workers, those days are gone.

Today the responsibility of preparing for your retirement life stage falls squarely on your shoulders.

In the early 2000s, more workers at large private sector companies had access to a traditional pension plan than those that only had access to a defined contribution plan, according to the Bipartisan Policy Center Report of the Commission on Retirement Security and Personal Savings. So, how does one think about preparing for a personally satisfying and financially secure retirement today?

For many, the default approach seems to be to just “save what I can” for retirement. Individuals taking this approach usually save what’s “leftover” after making payments on their home, car and credit cards and covering their expenses of daily living. People generally recognize that they should save at least enough to capture their employer’s 401(k) match, if such a match exists, lest they “leave money on the table” each year.

For most people, this approach will lead to a retirement that is well below their current lifestyle. On the other hand, for some high earners that live well below their means, it could mean putting away more money than they could ever use in retirement. In either case, the approach is flawed because it does not take into account the type of retirement the individual wants. The amount being saved under this approach is a byproduct of other expenses, uncoupled from future expectations. People are putting away whatever they can for a future they haven’t defined.

“Tangibilize” Your Retirement

I’m an advocate for a different approach to thinking about retirement. Step one is to “tangibilize” retirement. Ask yourself what do you want to do in your retirement years? Be as specific as you can possibly be. When I ask people what they want to do in retirement, the most common response is “travel”. I will follow up by asking for more specifics.

Tell me about the travel you want to have. Do you want to take the extended family on a three-week African safari, or do you want to live in Paris for several months each spring, or do you want to see a national park every other month with your spouse? Be as specific as possible. What about where you want to live when you’re not traveling? Where, what type of home? What type of work will you want to do around your house and what type of work will you want to have others do for you? What about hobbies and other pursuits you will have time to focus on? What will they be, what type of equipment will you need and where will you pursue them? How will you stay in touch with your friends and family? Will you try to see them in-person? How often? Will you go to see them, or will they come to see you? Does this impact where you might want to live? What type of healthcare services and equipment will you want access to as you get older? Just the minimum or do you want first-rate care and equipment?

For most people, buying something is a much more compelling proposition than “saving for an undefined future”. So, if you can visualize the many aspects of what you will want to do in retirement, you will make retirement “real” because you will be able to recognize (almost touch) what you are wanting to buy. Few people get excited about saving 15% per year for retirement. But we all recognize that it takes money to buy the things we want, this approach will give retirement a chance to compete with the other “things” vying for your money. Too often people make retirement preparation about “getting to a number” rather than about getting to an exciting chapter of life they can describe to others, much less themselves.

Of course, whether we recognize it or not, we are each already on a path to buying a particular type of retirement. We just may not fully realize it. So, how can we re-frame the thinking around preparing for retirement to help us achieve our personally satisfying and financially secure retirement? The addition of two new elements may help.

First, we can better leverage the priority that most Americans place on paying their debt. Although it varies over time based on overall economic conditions, typically only about 1 in 10 Americans are behind on their mortgage or auto loan payments.

Contrast that with the recent Gallup finding indicating that most Americans feel they won’t have enough money to retire comfortably.

We should recognize that when we are born, we receive two items related to retirement. We receive a Social Security number, and we receive our retirement debt. We must pay (to ourselves) this amount before we can comfortably retire. If we don’t make payments on our retirement debt, we risk not having the retirement that we seek to have. Moving the need to prepare for retirement from the “optional savings” category and into a mindset of “paying off” an important debt may increase the importance and regularity of making this a financial priority. Imagine if we all made preparing for retirement as important as paying the mortgage. Instead of most Americans being worried about being able to afford retirement, nearly 90% would feel comfortable about their future.

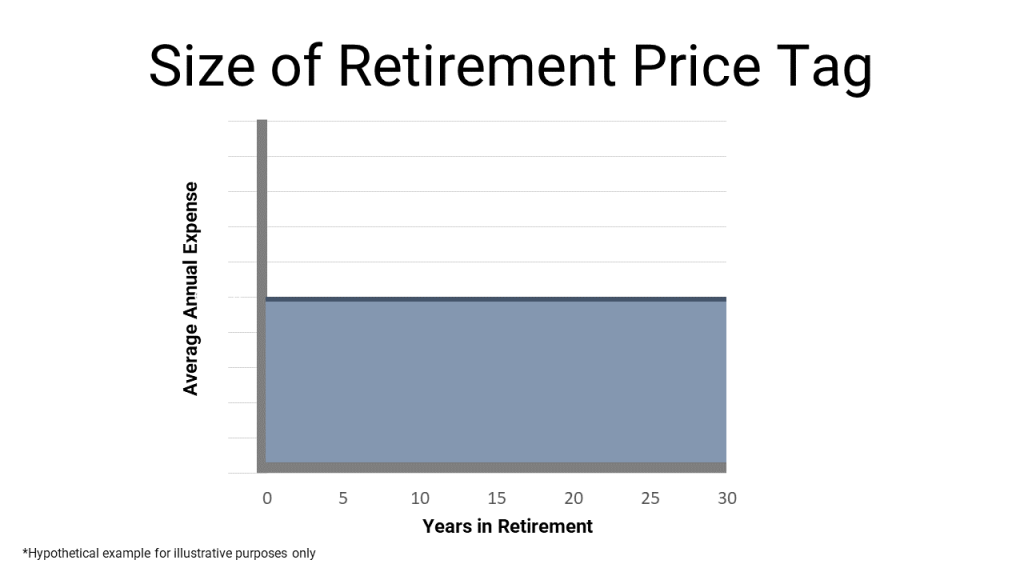

Visualize Your Retirement Price Tag

Second, it’s conceptually difficult for many people to grasp how big the price tag is for the retirement they desire. In its simplest terms, the cost of retirement is the product of your average annual retirement spending times the number of years in retirement.

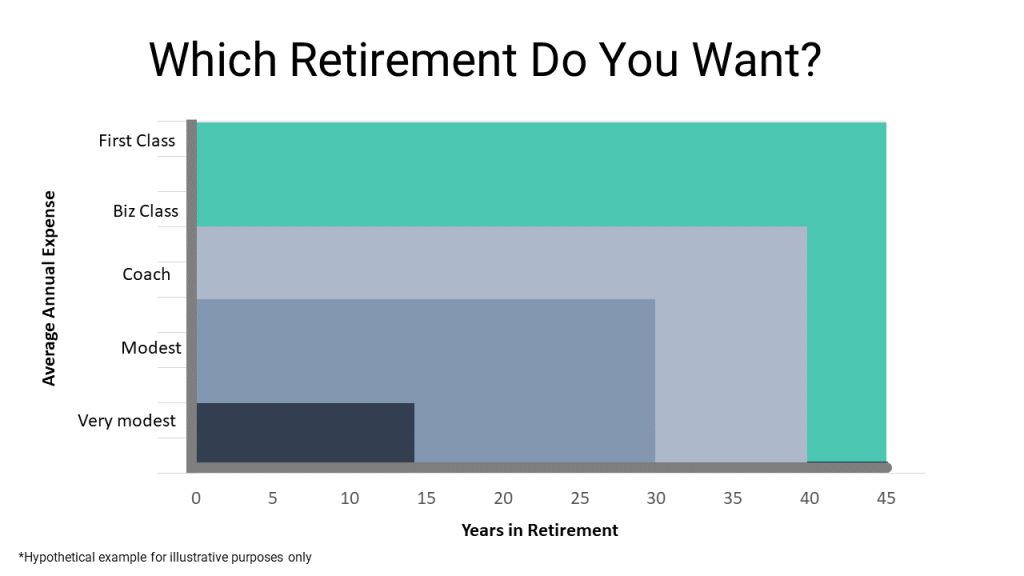

Of course, there are various types of retirement for sale. For example, if we refer to a typical retirement as the “coach-class” version of retirement, you can imagine that a nicely upgraded version of retirement exists that includes a bit more comfort in all aspects of life, call it a business-class version of retirement. For those that can afford it, there is a version of retirement that includes all manner of luxury, from housing to travel to entertainment to health services, call it the first-class version of retirement.

Similarly, there are also less expensive retirements available to buy. Perhaps some of these will require you to move from your current home to a smaller home in a much more affordable part of the country. Perhaps this retirement will only allow for limited, budget-minded travel, and health care services only when absolutely necessary. In essence, the vertical axis in our chart indicates the type of freedom and lifestyle one desires to have in retirement. Each level comes with a different price tag. The higher up on the axis you desire your retirement experience to be, the more expensive your retirement will cost.

The horizontal axis is the number of years of retirement. Obviously, we don’t control this precisely. However, for a particular individual, the sooner/later you enter retirement the longer/shorter retirement will generally be for that individual. Retiring earlier can be expected to lead to a longer, more expensive retirement because, at any level of expense, you can expect to have to pay for it for more years. Retiring later can be expected to lead to a less expensive retirement, because there will be fewer years in retirement for which to pay.

Decide Which Retirement You Want

Using this approach anyone can start to get an intuitive sense of how large the price tag is for the retirement they want to buy. For example, if one is willing to work beyond the typical age of retirement and live a very modest retirement, the price is relatively small (as depicted by the yellow box in the chart below). On the other hand, if someone wants to retire early and live very comfortably during retirement, then the price will be much more (as indicated by the green box).

Visualizing the size of the price of the desired retirement can help people make a connection between the retirement experience they have “tangibilized” and the amount they need to save. Some may desire a long comfortable, retirement but be saving only enough for a short, modest retirement. Realizing this may help provide the motivation to make different day-to-day financial decisions. Alternatively, some may be fine with a typical, “coach” style of retirement but be saving enough for a long, luxurious retirement experience. The key is to couple your “tangibilized” expectations and the cost of that experience.

Too often industry professionals boil preparing for retirement a one size fits all mathematical chore. In reality, we aren’t saving for retirement, we are saving for our retirement. There are important individual decisions to be made about our retirement that take into account our personal circumstances and desires. Making important choices about our desired retirement can motivate and guide our financial decision-making throughout our lives to prepare us for the retirement experience we seek to have.