Consider three scenarios:

- An individual investing a lump-sum amount for thirty years

- An individual saving a fixed percentage of a constant inflation-adjusted salary at the end of each year over a thirty-year accumulation period

- An individual withdrawing the maximum sustainable constant inflation-adjusted amount from a portfolio at the start of each year over a thirty-year retirement period

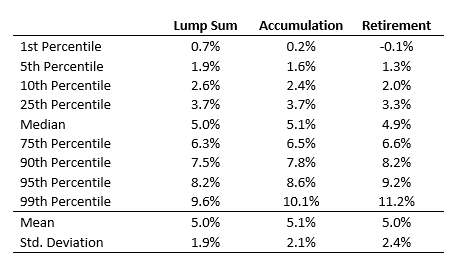

Exhibit 1.1 provides the distribution of results for these simulations. These simulations are based on a standard 50/50 portfolio using historical Morningstar data for the S&P 500 and intermediate-term government bonds. For the portfolio, Return Characteristics by Asset Allocation as Based on US Financial Market Nominal Annual Returns, 1926–2018 revealed that the real arithmetic average return was 5.6 percent, with a 10.6 percent standard deviation. This leads to a real compounded return of 5 percent.

For the lump-sum investment, the numbers represent the distribution of average compounded returns over 100,000 thirty-year periods. For the accumulation phase, the distribution of outcomes is for the internal rate of return for the final wealth accumulation when making thirty annual contributions. For the retirement phase, the distribution of results is for the internal rates of return on the portfolio when withdrawing the maximum sustainable amount over a thirty-year period with distributions taken at the start of each year.

The accumulation and distribution phases are dollar-weighted returns, instead of simple time-weighted returns for the lump-sum investment, because they account for cash inflows or outflows over time. Whenever there are cash flows, the ordering of returns matters because returns at different times will impact different amounts of net asset flows. This is the source of sequence risk.

In all three cases, the median return was close to 5 percent, with slight variations for accumulation and retirement based on the timing of the cash flows. This matches the observation that with an expected growth rate of 5 percent, the portfolio achieves at least a 5 percent growth rate only half of the time, as the probability the median return can be achieved is only 50 percent. When choosing a number to plug into a spreadsheet, a conservative retiree might be more comfortable using something like the return in the 25th percentile—or even the 10th—of the distribution. These lower return numbers would correspond to 75 or 90 percent probabilities of success, respectively, for a financial plan created with planning software.

Exhibit 1.1 Distribution of Compounded Real Returns over 30 Years Monte Carlo Simulations for a 50/50 Asset Allocation Based on SBBI Data, 1926–2018, S&P 500 and Intermediate-Term Government Bonds

Source: Own calculations with 100,000 Monte Carlo simulations for thirty-year periods. Portfolio returns are lognormally distributed with a 5.6 percent arithmetic real return and 10.6 percent standard deviation.

Exhibit 1.1 provides the implied fixed returns at other percentiles of the distribution as created through this reverse-engineering process. With the lump-sum investment, the compounded real return at the 25th percentile is 3.7 percent. For an accumulator, the 25th percentile return is also 3.7 percent, while it is 3.3 percent for the retiree. Higher success rates are connected with lower portfolio returns, since the return hurdle must be exceeded by the portfolio for the financial plan to be successful. At the 10th percentile, realized compounded real returns were 2.6 percent for the lump-sum investment, 2.4 percent for the accumulator, and 2 percent for the retiree.

These numbers are naturally lower to provide a greater chance of success, and sequence-of-returns risk pushes these numbers even lower for accumulators and retirees. The volatility of outcomes increases as we transition from a lump sum (standard deviation of 1.9 percent) to accumulation (2.1 percent) to retirement (2.4 percent). This trend represents growing sequence risk.

Individuals accumulating or spending assets will have different experiences than someone using a lump-sum investment. Accumulation effectively places greater importance on the returns earned late in the career when a given return impacts more years of contributions. This is sequence-of-returns risk as it applies in the accumulation phase. With greater importance placed on a shorter sequence of returns, we should expect a wider distribution of outcomes.

As for retirement, the impacts are even bigger as sequence risk further amplifies the impact of investment volatility. Retirees experience heightened sequence-of-returns risk when funding a constant spending stream from a volatile portfolio. A portfolio decline causes withdrawals to become a larger percentage of remaining assets. This digs a hole for the portfolio that can be difficult to escape. The distribution of internal rates of return during retirement will be even wider because of the heightened importance placed on the shorter sequence of postretirement returns. A conservative retiree seeking a return assumption for retirement should use a lower value than for preretirement.

In this discussion, I am tackling Monte Carlo from a different direction—using Monte Carlo simulations to calculate a fixed average growth rate for the portfolio. Those fixed returns could then be used in a deterministic planning analysis to determine outcomes with a greater chance to succeed. Conservative investors will want to work with lower assumed returns, implying a need to save more today. The exhibit provides insight about appropriately conservative adjustments for return assumptions.

Not only does sequence risk widen the distribution of outcomes in retirement, but retirees also experience less risk capacity. With less time and flexibility to make adjustments to their financial plans, retirees who experience portfolio losses after leaving the workforce can experience a devastating impact on remaining lifetime living standards.

This is another reason why individuals may want to use different return assumptions pre- and postretirement. For example, a conservative individual might be willing to use the 25th percentile return during accumulation (calibrated to a 75 percent chance for success) but only the 10th percentile during retirement (90 percent chance). If the individual were comfortable with the arithmetic real return and volatility of 5.6 percent and 10.6 percent, this would suggest using a 3.7 percent compounded real return assumption in the spreadsheet for accumulation and a 2 percent compounded real return assumption in the spreadsheet for retirement.

Because of sequence-of-returns risk, conservative investors will want to use lower fixed-return assumptions than just the compounded return assumed for a lump-sum investment. Sequence-of-returns risk is relevant for both the accumulation and retirement phases. Assumed returns should be lower in both cases. The impact is even greater for retirement. Conservative individuals will not want to use the expected return for their portfolios when developing lifetime financial plans. This is a really important point to remember and internalize when working in environments that require a fixed-return assumption without an accompanying volatility.

This is an excerpt from Wade Pfau’s book, Safety-First Retirement Planning: An Integrated Approach for a Worry-Free Retirement. (The Retirement Researcher’s Guide Series), available now on Amazon.