Simple analyses, which look to historical returns as estimates for what retirees should expect in the future, tend to provide an incomplete picture that may overstate the potential for stocks relative to other strategies. We will investigate some of the adjustments that should be made to historical returns to obtain a better idea about the net returns from an investment portfolio on a forward-looking basis. These include accounting for the impacts of volatility on compounded returns, inflation, investment fees, investor behavior, asset allocation, and taxes.

We can also identify stock returns as the sum of inflation, real bond yields, and an equity premium, and we can look to what are reasonable values at the present for these building blocks. Another important matter is to incorporate the idea that most financial planning involves seeking a high probability of success, which requires assuming below average returns, and the necessary reduction to return assumptions is greater when distributions are taken.

While a risk premium must be expected in order to induce investors to position their assets into more volatile investments, there is no reason to necessarily believe that historical excess returns provide the best predictors about the future risk premium. Also, it may take longer than anticipated for returns on stocks to outpace bonds, and retirees who are taking distributions become more vulnerable to this waiting game.

All too often, it seems that examples about retirement planning are based on assumptions that investments will grow at a fixed 8 percent or even 12 percent. While not impossible, the reality is that such return assumptions are overly optimistic, especially for those approaching retirement.

For a lifetime financial plan, the most intuitive way to express a portfolio return assumption is as an inflation-adjusted compounding return. Unfortunately, this is not the most common way returns are expressed. It is more typical to see returns expressed in nominal terms and even as arithmetic numbers that incorrectly reflect long-term growth rates. As well, to understand potential purchasing power, we should make further adjustments for taxes, fees, investor behavior, and asset allocation. A quick review is in order for the steps needed to arrive at a net real compounded return for a portfolio, as well as other adjustments that may be needed to create a properly conservative portfolio return assumption.

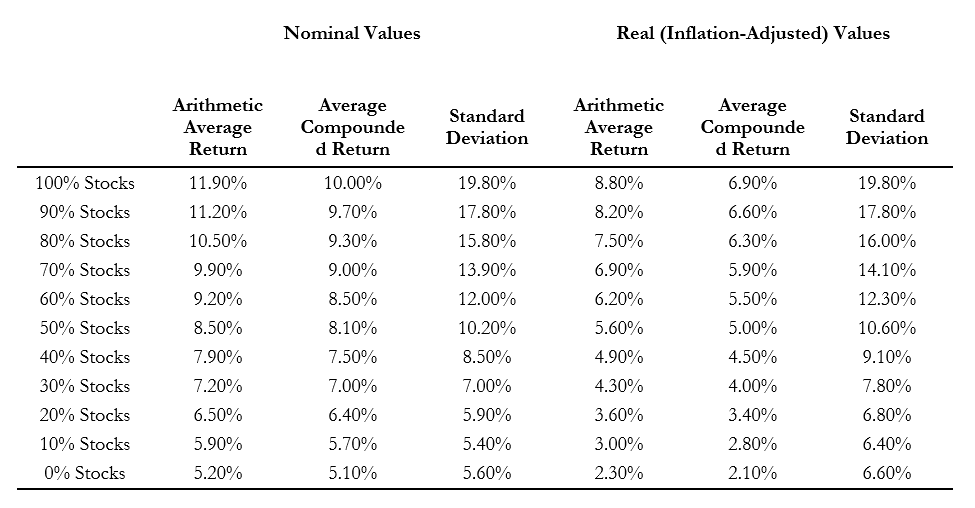

Exhibit 1.1 Return Characteristics by Asset Allocation as Based on US Financial Market Nominal Annual Returns, 1926–2018

Source: Own calculations from SBBI Yearbook data provided by Morningstar and Ibbotson Associates. Stocks are represented by the large-capitalization US stocks and bonds by intermediate term US government bonds.

Exhibit 1.1 shows the historical returns for different asset allocations for portfolios consisting of different combinations of the S&P 500 and intermediate term US government bonds (ITGB). As described with the earlier discussion of Summary Statistics for US Financial Market Annual Returns and Inflation, for the period since 1926, Morningstar data reveals that the S&P 500 enjoyed an average (arithmetic) return of 11.9 percent, while intermediate-term government bonds earned 5.2 percent.

Volatility

When simulating long-term financial plans, we also have to account for volatility and the lack of symmetry in outcomes for positive and negative returns, as discussed. We calculate the compounded returns over time to account for this volatility. The S&P 500 compounded return fell to 10 percent, while the compounded return for the less volatile bonds fell only slightly to 5.1 percent. These compounded returns express the growth rate for a portfolio over longer periods, while the larger arithmetic average returns represent the average return only for a single year.

At least one popular radio host likes to imply that his listeners’ stock portfolios will grow at 12 percent, but this is a misunderstanding on his part. It is the compounded return, not the arithmetic return, that matters for the long-run growth of a portfolio.

This is an excerpt from Wade Pfau’s book, Safety-First Retirement Planning: An Integrated Approach for a Worry-Free Retirement. (The Retirement Researcher’s Guide Series), available now on Amazon.