Readers of my last blog entry, Annuities and Delayed Social Security, provided many valuable comments, prompting me to now write a follow-up post. Most of the discussion centered on a chart showing the relationship between annuity payout rates and interest rates. That chart was actually a last minute addition, as I saw the picture on my desktop and decided it might be worthwhile to include.

Now I’d like to discuss more about how annuities are priced and whether it is a good idea to wait to buy an annuity. I will limit the discussion today to inflation-adjusted single premium immediate annuities (SPIAs).

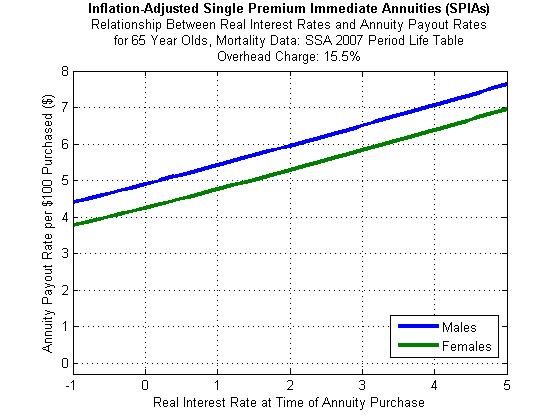

I will provide a modified version of the chart which I showed before. This is an inflation-adjusted SPIA for 65-year olds. For mortality data, I used the Social Security Administration’s Period Life Table from 2007. The interest rates are in real terms (such as the 30-year TIPS yield). Formulas for the calculations can be found below in Appendix 1. I charge a 15.5% overhead charge on the annuity (see more about overhead charges in Appendix 2). Also, before I showed interest rates up to 10%, but since these are real yields, the chances of seeing that are about the same as seeing pigs fly. So I stop at 5% this time. [Nominal interest rates can be higher because they consist of real interest rates plus a premium for expected inflation. Real interest rates do vary over time, but I think the chances of ever seeing long-term TIPS yields above 4% again are very low.] The chart looks like this:

Long-term TIPS yields are currently under 1%, which means that current annuity payout rates for 65-year old males are a little above 5%. Females get lower payouts because they live longer.

Should someone wait for higher interest rates to buy a SPIA?

There can be valid reasons to wait for buying an annuity, which I will address more below, but regarding the issue of whether it is worthwhile to wait specifically for interest rates to rise, I currently don’t think that sounds like a very good idea.

Who knows if TIPS yields will rise? They may continue falling. Even if TIPS yields do rise to 3% or so, this would result in only about a 20% increase in the annuity payout. Only 20%? That sounds like a lot. But as Boglehead dpbsmith argues at “with interest rates so low, are annuities effectively dead?”, if you are also investing conservatively like the insurance company, you will probably burn through your assets at a fast enough rate that you really don’t even get any benefit from the increased annuity payout rate since you have less assets by the time you do buy your annuity. He argues as well that, actually, by waiting you miss out on some of the mortality credits available by having had the annuity earlier. In the same thread, Boglehead alec also makes a good point that if you are waiting for interest rates to rise, and then they do rise, you will probably experience capital losses on your bond portfolio and so, again, you don’t get any benefit from the higher payout rate since you have less assets by that time. Joe Tomlinson did point out in the comments at my previous blog entry that this could be counteracted a bit by using shorter term bonds for your bond portfolio.

As well, as Matthew Amster-Burton, Dick Purcell, and others like Boglehead jbaron (at “Rates on annuities”) have argued, SPIAs actually become more attractive when interest rates are lower. You don’t buy annuities because they are good investments, you buy them because they provide a guaranteed income for life. This is insurance against living longer than your assets. And you have to compare SPIAs to the alternatives. A bond portfolio will also have more measly returns when interest rates are low. That is basically the alternative for an inflation-adjusted annuity. With low rates, the mortality credit component of the annuity payout becomes even more important, making annuities even more attractive relative to the alternatives like a bond ladder, etc. Another way to say it is, annuities are hurt less by low interest rates than alternative portfolio choices.

So don’t compare annuities to what might have been if interest rates had been higher, compare them to what is possible and available now. Now we are stuck with low rates. Trying to wait for rates to increase is going to eat away at your assets in the mean time, and there is nothing you can really gain from the effort. Low interest rates strengthen, not weaken, the case for purchasing a SPIA.

More generally, should I wait to buy an annuity?

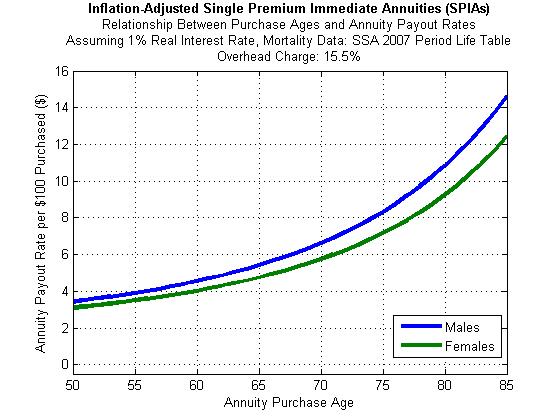

I will now provide another figure which I think explains a lot of the reasoning behind why some argue that it is good to wait as long as possible to buy an annuity. This chart varies annuity payouts by age of purchase, rather than by interest rate. It is made assuming a 1% real yield. Again, these are inflation-adjusted annuities with the same assumptions as before:

As you can see, the longer you wait, the higher is your annuity payout rate. It really starts accelerating in one’s 70s, because that is when mortality rates start picking up and survival rates drop more quickly. Remaining life expectancies start dropping quickly, and so as you do make it longer, you can get a higher payout by waiting to make the annuity purchase.

But this is not the whole story. For one thing, though the payout rate is higher, you have less time to collect. The life expectancy is getting shorter. That is the big reason why the payout is bigger. There really isn’t anything to be gained in that particular regard.

Another important point made by Dick Purcell is that you may not want to wait too long to make complicated financial decisions like this, because cognitive abilities decline as one ages and it could be easier for one to be swindled by some unscrupulous salesman selling some other type of annuity (not a SPIA) with all sorts of punishing fees.

One other issue is that as you wait longer for the higher payout, you end up using your other assets in the mean time. Boglehead dpbsmith argues that by waiting, you miss out on some mortality credits (though they are quite small before one’s 70s) and so you probably won’t gain from waiting. I’d like to run some further simulations about this point one of these days. It sounds like a good research topic.

And then again, there are valid reasons to hold off buying an annuity, or at least to stagger one’s purchases by purchasing small SPIA chunks over time. Boglehead bobcat2 provided some reasons, such as the possibility that interest rates could increase (though I argued against this reason above), the possibility that one could be run over by a bus the day after buying the annuity, the opportunity to spread annuity purchases across insurance companies to reduce the impacts of a company failure and to help keep annuity purchase amounts under state guarantee limits, and the opportunity to maintain more flexibility and control over ones assets.

In this regard, it does seem quite reasonable to me for one to make multiple annuity purchases over rather than buying all at once. This is probably a case where valid arguments can be made for both sides and there is no one-size-fits-all answer.

Of course another important point to emphasize is that it is probably very rare that the best course of action would be to annuitize all of one’s assets. I’m mostly talking about partial annuitization here.

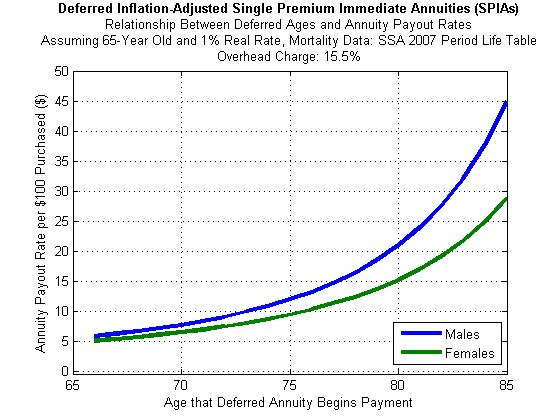

One other possibility worth mentioning is a deferred annuity. That is, someone aged 65, for instance, who purchases an annuity now which doesn’t begin payments until a later date. This is different from what I discussed previously when someone just waits until later to buy the annuity. The following chart is purely hypothetical since inflation-adjusted deferred annuities don’t exist yet. It is too hard for insurance companies to hedge the long-term inflation risk. But buying an annuity now which doesn’t begin payments until a later date gives a higher payout than waiting to buy the annuity at that date. The difference is just the probability of living that long. You get a lower price today because you may not make it until the time that annuity payments begin.

Appendix 1: Formulas for calculating annuity payout rates

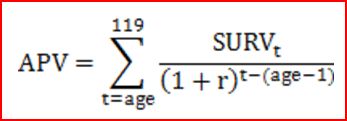

The Actuarial Present Value (APV) for an inflation-adjusted SPIA is:

where SURVt is the probability of still being alive to age t, conditional on having made it to the age in which the annuity was purchased (separated by gender), and r is the expected real return for the annuity company’s investments, which I am representing here as fixed over time at the value of current long-term real interest rates (such as the yield on 30-year TIPS).

When a deferred annuity is purchased (such as a 65 year old purchasing an annuity which begins payments at 85), then I replace SURV with zeros for the years that no annuity payments are made.

The Annuity Payout Rate is then:

where annuitized assets for the charts is $100, and overhead is the overhead charge in decimal form.

Appendix 2: About the Overhead Charge

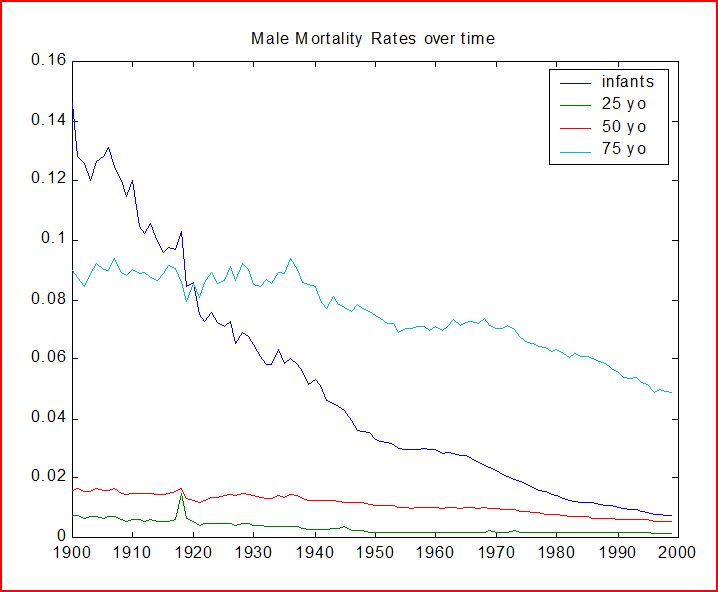

Insurance companies are businesses. They need to meet their business expenses as well as make a profit. Besides this, there are a couple reasons that they can’t just offer annuities priced using the 2007 Social Security Administration Period Life Tables. First, mortality rates can be expected to improve in the future as they have in the past. For instance, the figure below shows that single-year mortality rates for 75-year old males dropped from about 9% to 5% during the 20th century:

So people who are 65 today will probably have lower mortality rates when they turn 75 than the 75-year olds in 2007. The insurance companies must adjust for that, though perhaps if they have a life insurance business too then the two business components might hedge one another. But also, insurance companies must deal with adverse selection. That is, the people who buy annuities tend to know they are in good health (people with terminal illnesses have no particular reason to buy an annuity) and may expect to live longer than the average person. Insurance companies must also adjust for this.

John Greaney at the Retire Early homepage has an interesting analysis of these SPIA charges. He compared annuity rates from the Principal Group with actuarially fair annuity rates and found that compared to population averages, it seems that Principal charged an overhead cost to account for all the above factors of about 22-29%. Allowing for corrections for adverse selection (which annuity companies don’t get to keep and it isn’t really a cost for you either… if you expect you might live longer than average then you would need to be making adjustments for this no matter what retirement income strategy you choose), he finds the costs were 9-16%.

I too had played around with those Principal numbers as a way to try to calibrate my annuity pricing program to annuity prices in the real world. I was generally using 10-year Treasury bond yields (compared to higher yielding corporate bonds like John used), and I was usually finding that an overhead charge of 15-20% (compared to John’s 22-29%) would get me a matching annuity price. I’m not sure whether it is better to use Treasury bond yields or corporate bond yields, but at least here is a range of possible overhead charges.

This was a calibration exercise for me to match my results to some existing numbers, and I used 15.5% here because it happens to be the overhead charge that gave me a match for whatever was the last example I had looked at. That is the charge taken by the insurance company when they sell the SPIA, relative to the actuarially fair numbers. John is much more critical about these charges than I am and makes good points about corporate greed and excess, but I think that SPIAs are more transparent and understandable than many of the other types of annuities out there. If you want a guaranteed income for life in addition to the best deal out there (which is waiting to 70 to start Social Security), then you must understand that you’ve got to pay something for it. SPIAs seemingly provide the best possible actual option available.