You may have zero interest in agriculture, but trust me when I say that anyone with a taxable investment account should be thinking about harvesting – gain/loss harvesting, that is.

You can safely ignore gains/losses in tax-qualified retirement accounts – like your IRA and 401k. Those accounts are only taxed based on withdrawals, not on gains realized within the account. However, if you have non-qualified accounts (i.e., individual, joint, trust, UTMA), then roll up your sleeves: you might have some harvesting to do prior to year-end.

What Exactly Is Harvesting Anyway?

If your investment grows to be worth more than the price you paid for it, you have an unrealized gain. But just like a vegetable provides zero nutritional value until it’s harvested, your unrealized capital gain is just a paper gain – hanging on the vine – until it is “harvested,” or realized, by means of a sale.

Losses are treated the same way – the IRS doesn’t care about unrealized gains or losses – only those where an actual sale occurs are considered “realized” for tax purposes.

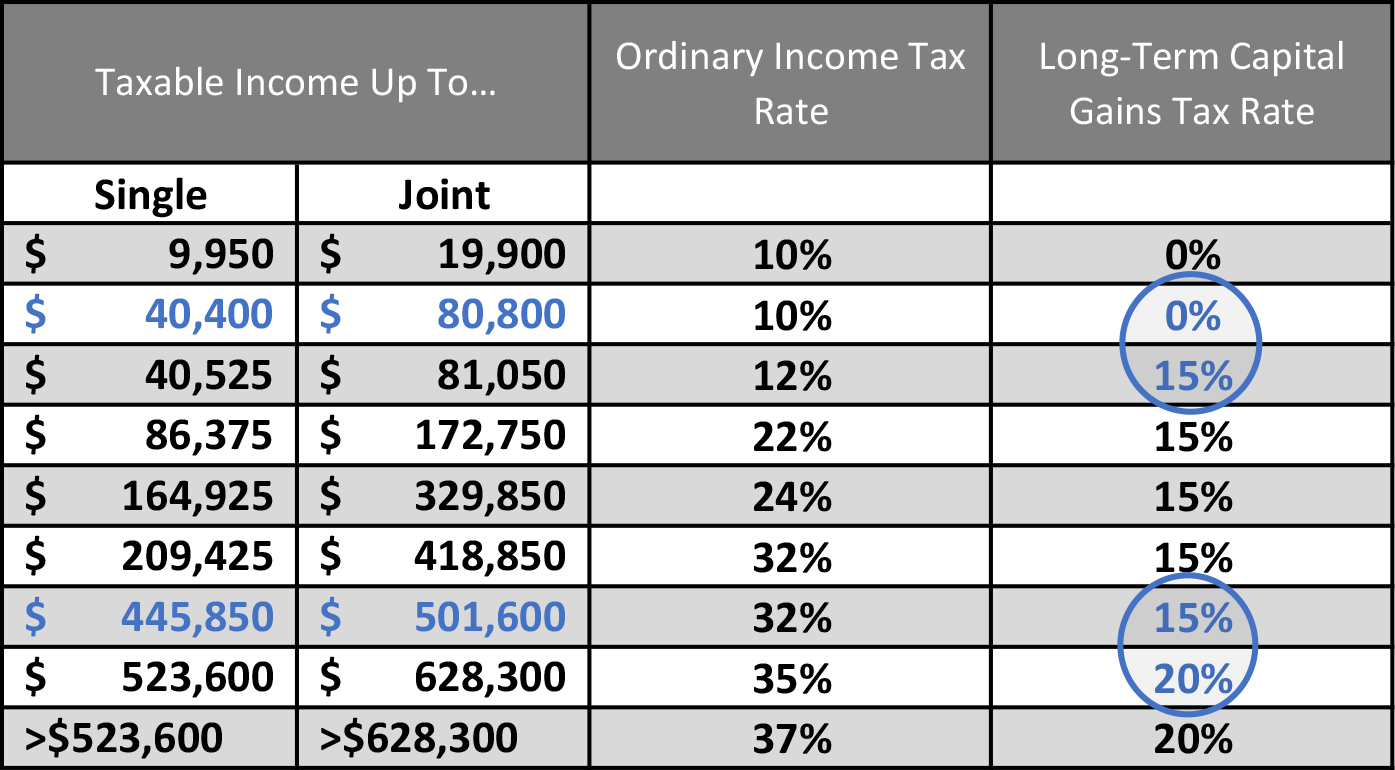

How Gains Are Taxed

Short-term gains (those with a holding period of one year or less) are taxed at ordinary income tax rates. Long-term gains are taxed at 0, 15 or 20 percent – depending on your ordinary income tax bracket. The chart below shows the latest numbers for 2017. Note the highlighted breakpoints, where the tax rate increases:

Thankfully, the IRS allows us to offset gains with losses, dollar for dollar. And if losses exceed gains, you can offset ordinary income by up to $3,000, with any additional amount carried forward to future years.

When to Harvest Losses

Not only will capital gains result in a capital gains tax, but those gains will also increase your Adjusted Gross Income (AGI), potentially causing numerous unintended tax consequences, such as:

- Exposure to AMT

- Increased taxation of Social Security benefits

- Increased Medicare premiums

- Exposure to the 3.8 percent NIIT (Net Investment Income Tax)

- Reduced medical and other itemized deductions

- Lost eligibility for tax credits or retirement plan contribution

Harvesting losses by reducing adjusted gross income (AGI) can mitigate some of these issues. Some reasons to consider harvesting losses.

- You sold real estate this year that generated a capital gain

- You have business sale proceeds that include a capital gain

- You have capital gains this year that push your AGI over an important breakpoint

- You expect to be in a lower (or zero percent) capital gains tax bracket next year

- You anticipate legislative changes that would reduce capital gains rates in future years

- You want to capture the $3,000 offset to ordinary income in the current year

When to Harvest Gains

Why on earth would you want to realize a gain?!? Here are some potential motivations:

- You are in a zero percent capital gains tax rate this year, and wish to capture as much in gains as you can for free, thus positioning your portfolio for reduced gains in future years by “resetting” your cost basis at a higher level.

- You have realized losses, and can rebalance your portfolio at no tax cost by selling high and buying low.

- You anticipate legislative changes that would increase capital gains rates in future years, so you want to harvest gains now, at presumably lower rates, and “reset” your tax cost basis at a higher level.

Survey Your Fields in The Fall

To determine if harvesting is warranted, review your YTD realized and unrealized gains/losses in your portfolio. Factor in any carryover losses from your prior year’s tax return. Consider that gain/loss information in the light of your current and expected future tax brackets and your current tax situation.

After completing that analysis, just execute your sales prior to year-end, and sit back and enjoy the fruits of your harvest!