There’s been a lot of interest in Bitcoins lately. Over the course of 2017, we also saw the price of a Bitcoin shot up more than 1,300%. It would have been at almost 2,000% if the year ended on it’s high point of December 171 (over the course of the last two weeks of the year, Bitcoin dropped 37%). Additionally, future contracts have started trading on the Chicago Board of Exchange, making it a lot easier to participate in.

It’s easy to see why there’s so much hype around Bitcoin and other various cryptocurrencies. It’s been a phenomenal year, and they keep hitting new highs. Plus, we’re right on that cusp of public consciousness where pretty much everyone has heard of Bitcoin, but you still sound really smart talking about them.

So, what I want to do is break through the hype, and see if Bitcoin, and similar cryptocurrencies, are good tools for retirement investors. Is Bitcoin likely to help you reach your retirement goals?

What Exactly Is Bitcoin?

Bitcoins are the most widely known cryptocurrency. Cryptocurrencies are decentralized digital mediums of exchange. In other words, electronic currencies.

There are several interesting features of cryptocurrencies, but I want to focus on two: 1) they are decentralized, and 2) this is still the ‘wild west’ for cryptocurrencies.

Let me elaborate. Because cryptocurrencies are designed to be decentralized, there’s no central authority that controls the money supply, or really anything else about them. There’s no cryptocurrency Federal Reserve pulling levers behind the curtain. In fact, it’s pretty much the opposite. The monetary policy of each cryptocurrency is baked into the specific design of the cryptocurrency.

Cryptocurrencies are still very new. The first major cryptocurrency was Bitcoin, which launched in 2009. New ones have been popping up like mushrooms ever since. Some of them are all but exact copies of existing cryptocurrencies, some are jokes (2014’s Coinye West, for instance), some are just strange (PotCoin, which was designed to facilitate buying and selling marijuana, and notably sponsored Dennis Rodman’s recent trip to North Korea), and some have real technological developments that meaningfully add to the ecosystem.

While all this activity moves cryptocurrencies forward from a technological standpoint, it also means a lot is still undetermined. We have no clue which of the hundreds of active cryptocurrencies (and all that will still be created) the market will settle on.

Like most technology, this is likely a winner-take-all type of situation. You don’t want to bet on the wrong one, or it will be about as useful as your HD-DVD collection.

So discussions of bitcoin really have two elements: Bitcoin as a technology, and Bitcoin as an economic instrument.

On the technology side, I’m incredibly excited. I think that the Blockchain(the underlying technology that Bitcoin and it’s cryptocurrency brethren are built on) will have profound impacts on the world – for our financial system, but also much more broadly.

However, I want to focus in on the economic side, since we want to find out if bitcoin is useful for a retirement investor.

Bitcoin as an Economic Instrument

Bitcoin presents itself as an economic currency: electronic money (we’ll deal with Bitcoins as an investment later). ‘Money’ is a notoriously tricky thing to pin down. We all know what it is, but economists end up doing mental gymnastics when they try and precisely define it. Is pizza and beer money? I once paid some friends with pizza and beer to help me move out of my house in Maryland. I even explicitly told them I would pay them in pizza and beer. If pizza and beer aren’t money, why aren’t they?

This is actually really common. If you ask specialists in almost any field to define their basic terms, especially the terms so basic that most people just implicitly understand them, those terms stop being basic really quick.

One of my favorites is how physicists define ‘time.’ This is something we all deal with, and it is absolutely fundamental to physics, but it’s really hard to accurately define. It’s all but it’s own subspecialty. There’s a concept called the Arrow of Time. It basically boils down to the explanation that “time moves in the direction that it does, because that’s the direction that time moves.” There’s been a lot of work on this since it was proposed, but the definition of time is still tricky.

…But, I digress. Back to Bitcoin as money. There are really three functions of money:

- Money is a medium of exchange

- Money is a unit of account

- Money is a store of value

So let’s walk through these functions, and how Bitcoin fits into each.

Is Bitcoin a Good Medium of Exchange?

Money is a standardized unit of exchange. This is probably the most basic of the functions of money. I can sell something, and immediately turn around and use the proceeds to buy something else. Essentially, it’s something that means that we don’t need to barter.

Bitcoin fits this definition. I can sell something and receive Bitcoins, and then use those Bitcoins to buy something else. The problem is, it’s not a very good medium of exchange. It’s hard to use Bitcoins in the real world. Many of the ease of use problems would be improved upon as Bitcoin becomes more popular and more widely accepted, but there are some problems that simply can’t; these problems are baked into how Bitcoins operate.

One of the biggest problems is how long transactions take to clear. Because of Bitcoin’s decentralized nature, it can take a while, often several minutes, for a transaction to clear, confirming for both the buyer and seller that the transaction went through.

With cash, transactions clear pretty much instantaneously. As soon as I hand you your money, the transaction has cleared. Think of a store swiping your credit card and waiting for the authorization. Now think of how annoying that is when something’s off. That whole uncomfortable process of getting your card declined and then giving them another card takes a minute or two at most. Bitcoin makes that process take several times longer, and it happens every time you buy something.

So, no, it’s not a great medium of exchange.

Is Bitcoin a Good Unit of Account?

A unit of account refers to how we think about value. If I ask you the price of something, you’re probably going to tell me how much it’s worth in dollars. Going back to our pizza and beer example, you’re (probably) pretty unlikely to tell me that something costs two large pizzas from Otto’s, and a six pack of Pacifico.

Whatever we’re talking about may actually be equivalent in worth to two large pizzas and some beer, but it wouldn’t be a good way to express the value. That’s just not how we talk about how much something is worth. You can think of this as essentially a collective action problem. Something’s not really a great unit of account until enough people think that it is, and use it.

With Bitcoins, we’re in the same place as we are with the medium of exchange. I could certainly price something in terms of Bitcoins (for instance, my consulting rate is one Bitcoin per hour – and given the price of Bitcoins, I’d be more than happy to have that conversation with anyone who might be interested), but two problems still remain:

- We have the collective action problem that we just talked about. You need a critical mass of people to price things in terms of Bitcoins for it to work.

- The value of bitcoins is incredibly volatile. When I’m setting my price, I want stability. I want to know what I can buy with the proceeds of what I sell. With Bitcoins, I really have no idea how much my proceeds are worth on a day-to-day basis.

Which brings us to the last function of money – storing value.

Is Bitcoin a Good Store of Value?

This is the function of money that most of the people who are really enthusiastic about Bitcoin tend to focus on. Money is supposed to hold it’s value through time. A $20 bill will still be worth $20 five years from now. A Bitcoin will still be worth a Bitcoin five years from now.

What gets Bitcoin fans really excited is inflation. Most currencies have some level of inflation. Bitcoin does not. In fact, to the extent that people keep using it for the long-term, it’s actually, by design, deflationary. There is a limited number of Bitcoins that will ever exist. Once they are all in circulation, that’s it. As the value of the economy denominated in Bitcoins increases, the value of Bitcoins will rise right along with it.

At first blush, this may sound appealing, but moderate levels of inflation are actually good for the economy.

We’ll talk about this more when we discuss Bitcoins as investment vehicles, but what most people are really after here is a way to hedge their inflation exposure to their home currency, and we have tons of really good ways of doing this.

One other point that’s worth making here – the fact that Bitcoins are massively volatile doesn’t actually disqualify it as a store of value. Bitcoins are more volatile than gold, but the same idea applies.

Gold is really volatile. But, not only is gold a store of value for many people, it actually was money for a long time around the world. That being said, I don’t really like my store of value jumping all over the place on a daily basis – especially when I have more stable options that are much easier to use.

So, to sum up, Bitcoins hits all of the marks for being a currency, but not all that well. This could change as the technology improves, and if more people decide to use it.

…But now for the real question – are Bitcoins a good tool for retirement investors?

Bitcoins as an Investment Tool

This is what gets most people excited about Bitcoins. The hardcore folks may talk about the technology, and the more utopian aspects of Bitcoin, but the vast majority of people are really focused on Bitcoin as an investment. Last year, we looked at this exact subject, and my basic answer hasn’t changed at all. Investing in Bitcoins is straight up speculation.

I still want to dig a little deeper and put some numbers around this.

As we discussed last time around, Bitcoins act a lot like gold – but with the volatility cranked up to 11. In fact, even the volatility of the volatility is higher for Bitcoins than it is for gold.

This actually makes a lot of sense; Bitcoins, like commodities (and other currencies), do not produce anything in and of themselves. If you invest in a company, that company is actively trying to create economic value for it’s shareholders. It’s trying to grow the size of the economic pie. A Bitcoin is always going to be worth a Bitcoin (just like a dollar will always be worth a dollar). An ounce of gold is always going to be an ounce of gold. They are things that are acted upon – not the things that are doing the acting.

When we looked at commodities in the past, we saw that commodities didn’t work all that well for someone investing for retirement. The same is true if you’re looking at investing in Bitcoin.

Bitcoin has certainly done very well over the past year. As I said at the outset, in 2017, it had a 1,200% return, as opposed to the 19% return you got from the S&P 500 Index (which is actually an awesome return).

But, the path to Bitcoin’s incredible returns has also been incredibly bumpy. A good way to look at this is by looking at the volatility of daily returns. The standard deviation of the daily returns of Bitcoin in 2017 was 4.94%. This is a truly astounding number.

To give some context, the standard deviation of the S&P 500’s daily returns was 0.42%. Less than a tenth of the volatility of Bitcoin, and this is the hairy and scary stock market. Bitcoin makes it look boring. That’s pretty impressive.

It gets even scarier if we look at the most eventful days of the year.

| Bitcoin | S&P 500 Index | |

| Worst Day of 2017 | -16.21% 9/13/2017 |

-1.82% 5/17/2017 |

| Best Day of 2017 | 25.56% 7/19/2017 |

1.37% 3/1/17 |

| Range Between Best and Worst Day of 2017 | 41.77% | 3.19% |

Data courtesy of Yahoo Finance. Data from 1/1/2017 – 12/31/2017. Indices are not available for direct investment. Past performance is not indicative of future performance. For illustration purposes only.

The best and worst single days for Bitcoin, just this past year, were not even in the same ballpark as the stock market. They were more in line with reasonably large annual moves than single day moves.

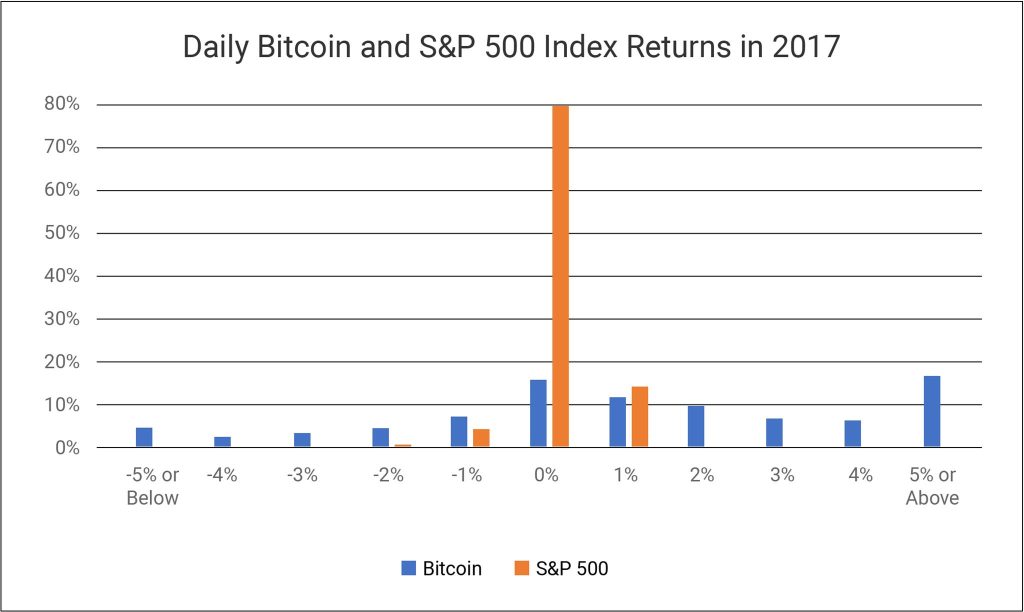

It wasn’t just that there were a handful of really big days throughout the year; this was more or less constant. Let’s look at a histogram of the daily returns for Bitcoin and the S&P 500 Index:

Data courtesy of Yahoo Finance. Data from 1/1/2017 – 12/31/2017. Indices are not available for direct investment. Past performance is not indicative of future performance. For illustration purposes only.

As you can see, the returns of the S&P stay huddled pretty close in – and in fact, just shy of 80% of the returns round to 02. For Bitcoins, only a little more than 16% of the daily returns rounded to 0. In fact, a lot more of the returns were out on the tails than in the middle. More than 1 out of every 5 days (that’s more than once a week) Bitcoin had a day where it returned either more than 5% or less than -5%3.

This looks a lot more like speculation than real investing to me.

And Finally, Should You Take a Flyer on Bitcoin?

Pretty much whenever we speak with clients about Bitcoin, or any other cryptocurrency, they understand why it doesn’t really have a place in their retirement portfolio, but they come back and ask if it’s worth taking a flyer on. Is it worth throwing down a couple thousand bucks and seeing what happens?

I think of it like heading out to Vegas4. If you enjoy gambling in Las Vegas, that’s great, but it’s entertainment – it’s not an investment strategy. If you go in thinking that you’re going to spend a certain amount like you would on any other vacation, there’s absolutely nothing wrong with that. That’s why you have your money: so that you can do what you want with it. But the odds of you going home with more money than you started with are vanishingly small. It’s possible – you might be the person to hit the jackpot – but it’s certainly not the way to bet.

The same is true with Bitcoin. If you enjoy having some money in Bitcoin, that’s great. As I sit here with five computers within ten feet of me, I think they’re really cool5. Buying bitcoins is a similar consumption activity; you’re doing it because it’s fun. You get to be part of something that has the ability to fundamentally change the world, plus it’s great to talk about at parties. However, it’s not what I would call investing.

—

Footnotes

- All returns data courtesy of Yahoo Finance. The 2017 return was 1,332.65%, and year to date as of the high point on 12/17/17 was 1,962.59%.

- Meaning that the daily return was more than -0.5%, but less than 0.5%

- And remember – Bitcoin doesn’t care about market hours. It trades all seven days of the week.

- I hate when people compare the stock market to Las Vegas. Investing in stocks is not gambling – in fact, they’re diametrically opposed. When you gamble in Las Vegas, the odds are actively stacked against you – the house (eventually) always wins. It’s the opposite in the stock market – if you stay disciplined, the odds are in your favor because of the long term, positive, expected return on capital.

- I hate when people compare the stock market to Las Vegas. Investing in stocks is not gambling – in fact, they’re diametrically opposed. When you gamble in Las Vegas, the odds are actively stacked against you – the house (eventually) always wins. It’s the opposite in the stock market – if you stay disciplined, the odds are in your favor because of the long term, positive, expected return on capital.