Most people are focused on saving for retirement so they’ll have the money they need to fund their spending in retirement. However, ask most people how much they’re going to spend in retirement and they have no idea. To plan for retirement effectively, you need to have some sense of what your spending needs are actually going to be.

Knowing what you want to spend is crucial if you’re going to know how much you need to save. Just like everything else in finance, figuring out how much you will spend in retirement is a big “it depends.” Most folks want to maintain (roughly) the same standard of living in retirement they had while working. Same standard of living, same cost of living, right? It’s not quite that simple. Retirement changes everything, including how you determine your budget.

What is Your Replacement Ratio?

One common approach is to find your “replacement ratio.” This is found by taking the income you made immediately prior to retirement and figuring out what percent of that income you think you’ll spend every year. The amount you’ll spend is the amount you’ll need to replace every year in one way or another.

Most people end up needing less income in retirement than they did while working, because, among other reasons:

While a lot of expenses will go down, you’ll also want to consider expenses that tend to go up in retirement, such as travel or other leisure activities you’ll have more time for. Depending on what you enjoy doing, this can end up being a significant portion of your budget in retirement.

Empirically, your replacement ratio is inversely related to your pre-retirement income. The higher your income before retirement, the lower your replacement ratio. Essentially, people with higher paying jobs had proportionally more of their income going to retirement, job-related expenses and taxes before retirement, rather than necessities.

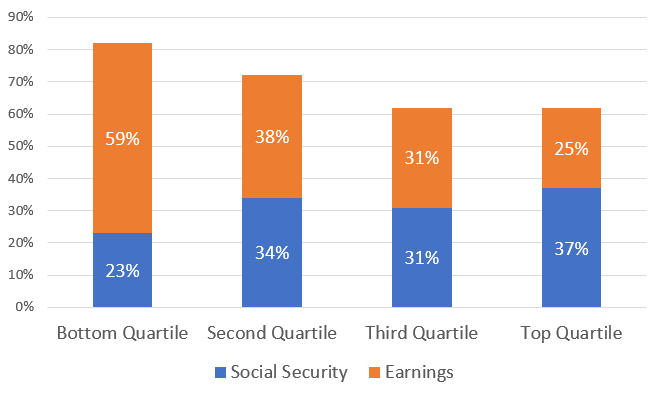

Marlena Lee at Dimensional Fund Advisors found median replacement ratios as a percentage of pre-retirement income:

Don’t take these numbers as absolute truth, but they should put you in about the right ballpark of how much income you want in retirement. Take a serious look at your financial situation and your desired lifestyle to determine a realistic spending rate in retirement. If you want to spend a month traveling every year, you’ll want to budget for a larger replacement ratio than if your big annual trip is a long weekend at a local bed and breakfast.

Get More Specific

Replacement ratios provide a great way to start thinking about how much income you’ll need in retirement, but they are only the beginning of the story. Your needs will almost certainly vary in retirement – you may want to help pay for your grandchildren’s education, you could have health issues, or any number of things could happen.

A good way to approach this is to make a list with two columns — on one side, list things you want to accomplish in retirement; on the other, list things you are afraid of in retirement. These can give you some idea of what you need to be prepared for in retirement. That list combined with your replacement ratio will put you on the path to figuring out what you will want to spend in retirement – which is the first step in the retirement planning process.