In previous entries, we have discussed your reactions to various aspects of the RISA™. Here, I want to address whether or not you feel it would be helpful to share the results with a financial professional. We asked participants:

- If you have a financial advisor, do you feel the RISA™ would be helpful to them in implementing your retirement income plan?

- If you do NOT have a financial advisor and you considered using one, do you feel the RISA™ would be helpful to them in implementing your retirement income plan?

These questions were open-ended to encourage feedback. After reading your answers on both questions, we categorized them into three general categories:

- Yes

- On the fence

- No

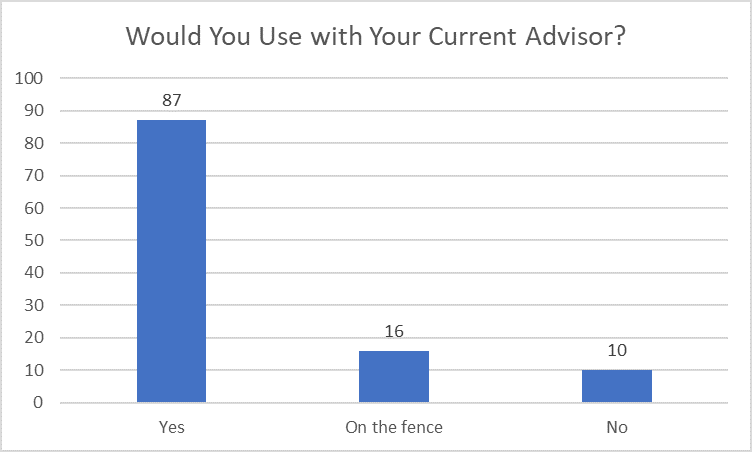

First Question:

Out of one-hundred and thirteen (113) respondents with an advisor, eighty-seven (87; 77%) indicated that they would present this to their current advisor as a guide for their retirement income plan. They indicated:

- Absolutely, at a minimum the advisor should be well versed in the underlying philosophy behind the RISA.

- Definitely as it would greatly help them know their client. It would also help them show the client exactly what their investment and retirement style is like and why specific recommendations are made.

- Definitely. I feel financial advisors only provide options that fit in their wheelhouse.

- I do have an advisor and my results would be a great starting point for a conversation about my comfort level for ‘risk’ vs. the advisor’s input on appropriate level of risk to attain desired financial success.

- I think it would be most beneficial at the beginning of the client relationship.

- I think this is a product that would be very beneficial to use with a financial advisor, instead of the “what would you do if the market dropped 25%” question

- Looking back at our experience with advisors, this would have been a great improvement over the tools they used.

Interestingly, some of the negative responses indicated that their advisor was already doing something like this:

- “Based on other tools that my current advisor utilizes and the relationship we have developed, I don’t think there is anything new here that would be useful to our retirement income plan.”

- “With the firm I have taken on, no. I do feel the information they asked for, and even more importantly, the one-on-one, both on phone and face-to-face, they provided, let them propose a retirement portfolio plan and distribution that is not very different from what the RISA recommended.”

Or their advisor has a different approach; “No, not their method.”

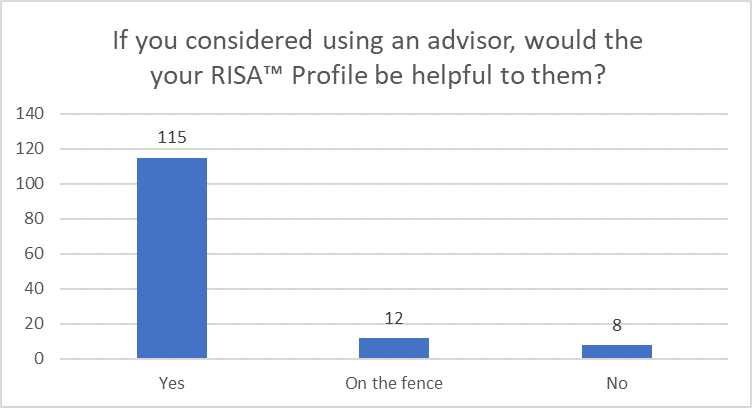

Additionally, we asked: If you do NOT have a financial advisor and you considered using one, do you feel the RISA™ would be helpful to them in implementing your retirement income plan?

Of the one-hundred and thirty-five (135) responses, one-hundred and fifteen (115; 85%) thought their RISA™ Profile would be helpful to a potential advisor in helping them develop a retirement income plan. While many responded with a simple “Absolutely” and “Yes,” more detailed responses are sampled below:

- Absolutely. And I would use the RISA in a screening process, if an advisor immediately rejects the RISA results, I would tend to avoid him or her. But I probably wouldn’t use an advisor at all.

- I think RISA is much more in-depth than a standard risk-analysis questionnaire and could be really helpful to newbies that are starting to see the need for financial and retirement planning

- Definitely. I think such a tool would help open up a series of discussions about goals, risks, investing approaches, income needs, and other topics. It can help identify one’s inclinations and do a better job of exploring options that match better.

- I would think it would be a tremendous tool to quickly and accurately determine an investor’s profile in order to recommend the “right” product, strategy or investment.

- If I were to engage again with an advisor, I would want to know if they had such a tool.

- It would definitely help any FA establish the lay of the land and first steps with me as a client. Also provides me peace of mind in that I can check FA against the RISA to ensure I’m getting what I should.

- Yes, absolutely. I could not imagine using a financial advisor without having the person review my RISA Profile, now that I have taken the almost-final version and learned about its construction, testing, validity, and reliability.

- Yes, if for no other reason to show the advisor what you are thinking as central to your plan. If he/she do not align then that points to looking further for an advisor.

- Yes, in fact, whether I gave them a copy of my results, I would be able to be assertive and say, “I want this kind of plan options”

- Yes. Would likely help them understand many of the key areas that they would need to know. RISA seems like a good way (methodical way) to jump start the process.

- Yes. This would be a VERY helpful tool in meeting with an advisor. It would save a lot of time and energy in the advisor getting to know me and my styles and goals.

We did have eight (8) respondents out of the one-hundred and thirty-five (135) answer negatively. Their comments included the simple “No” response. Another pointed out that their advisor was just responsible for managing investment portfolios and the RISA™ was not relevant to the advisors mandate: “Hope a financial advisor would match portfolio distribution to market conditions rather than an unrelated parameter.” And a few others expressed a desire to have clearer recommendations for an advisor new to the subject matter: “Not without reducing the technical wordsmithing and providing a clearer understanding of its benefits.”

Although we would like to please everyone, we know that is not realistic. In summary, however, we are extremely pleased with the results. Eight-seven (87) of one-hundred and thirteen (113) respondents with an advisor indicated that they would find the RISA™ helpful in implementing their retirement income plan, and one-hundred and fifteen (115) of one-hundred and thirty-five (135) respondents without an advisor indicated that they would use the RISA™ as a collaborative tool with a potential advisors for their retirement income plan.

All in all, we feel that the RISA™ passes the scientific rigors in determining your retirement income style. As importantly, by simply asking our participants what they thought of the process and outputs, the RISA™ Profile passes the “eye test” pretty convincingly.

If you missed our previous entries regarding initial reactions, please see them here: