There’s no magic formula for investing. The financial markets seem to take some sort of cosmic joy in bringing people back down to Earth. And it’s value investing’s turn – in fact, it’s been value investing’s turn for a while now. To put it mildly, this has been a rough decade and a half for value stocks.

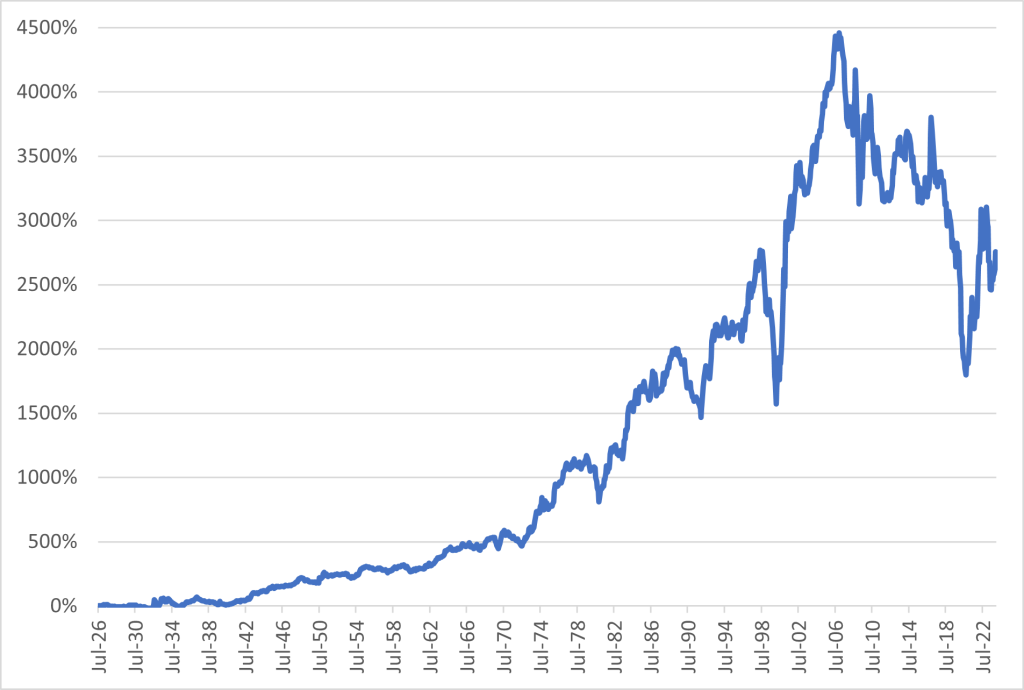

This has been the worst period for the value premium that we have ever seen. Rather than belabor the numbers, I think one chart can sum it up pretty well.

Cumulative Return of the Fama/French US Value Factor 7/1926 – 12/2023

This is a chart of the cumulative returns of the value premium – the difference between the returns of value and growth stocks. The story is clear – this has been an ugly decade and a half for value stocks.

And it’s led a lot of people, quite reasonably, to start asking is value dead? And additionally, is there a premium for owning growth stocks now?

What is a Value Stock?

Before we start looking at the current situation, let’s rewind a bit and talk a little about what the value premium actually is. Put simply, the value premium is the idea that the stocks that the market doesn’t “like,” value stocks, have better long-term returns than those stocks that the market “likes.”

So let’s take apart what this actually means. The price of a security is determined by how much investors are willing to pay for it (on both sides of the trade – both the person buying and selling a security need to be happy with the trade). When we are talking about value stocks, we’re specifically talking about stocks where investors aren’t willing to pay much relative to some fundamental measure of the company’s operations.

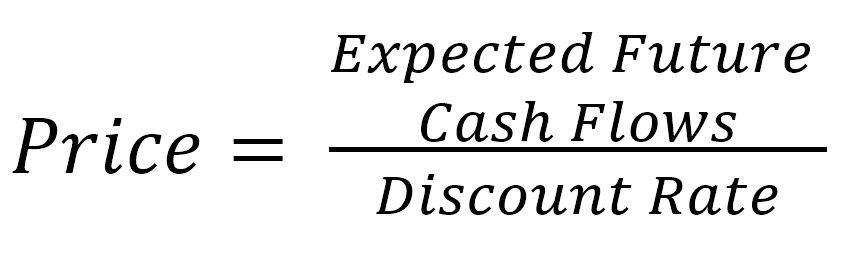

This means that investors are demanding a higher expected return for holding value companies. A good way to think about this is to look at how investors price securities. Effectively, the price of a security is the present value of all of it’s future cash flows.

Basically, if you’re looking at two stocks with the same expected future cash flows, but Stock A’s price is lower, then the discount rate people are using to value Stock A must be higher. Put a different way, investors are demanding a higher expected return for holding Stock A.

This relationship is exactly what the value premium is getting at. Value stocks are stocks that have a low price relative to some proxy for their future cash flows (that fundamental metric that we mentioned earlier). So long as we accept the idea that different companies have different expected returns, then there has to be a value premium – the question is how big that premium is, and how volatile it will be. And in turn if it is a premium that you want to include in your portfolio.

How Often Has Value Been Negative?

I want to dig into this question of how volatile the value premium is in practice though, and specifically how often the value premium has failed to come through. While we can talk about an expectation of a positive value premium, it is important to keep in mind that this premium only exists because value stocks are riskier than growth stocks. The value premium is the market’s inducement for people to hold these riskier stocks.

And because this is all based on risk, it isn’t unusual for growth stocks to outperform value stocks, though we are in a particularly bad period for value stocks. To put this in perspective, let’s look at some numbers.

From July 1926 through December 2023 the annual average return for the value premium, as measured by the Fama/French US Value Index which measures the returns of value stocks minus the returns of growth stocks, was 4.17%, with a substantial standard deviation of 12.39%. But how likely was the value premium to be negative?

To answer that, we can look at rolling returns. This type of approach steps through the returns, month by month, and looks at each subsequent period in turn. You can see the results below.

| Period Length | Percent of Period that were Negative |

| 1 Year | 39.3% |

| 3 Years | 29.9% |

| 5 Years | 23.0% |

| 10 Years | 12.3% |

| 15 Year | 7.4% |

As you can see, it’s pretty normal for growth stocks to beat value stocks, especially over shorter periods of time. If you were to pick a random month, there’s been nearly a 40% chance that the value premium will be negative over the next year, and a little bit more than a 20% chance that it will be negative over the next 5 years.

That said, what we’re seeing now goes beyond what we have seen historically. Prior to the period ending in May 2017, we had never had a 15 year period where the value premium was negative.

What’s going on here? The question isn’t so much about whether the value premium existed in the past – the data is pretty conclusive on that count – but rather has something fundamentally changed to cause the value premium to fail going forward?

Too Many People Know About Value

One of the more common reasons people suggest for the poor performance of the value premium is simply that too many people know about it now. It’s too well known, and there is too much money chasing it, so the premium has been “arbitraged away.”

The idea here is that since people now know that there has been a historical value premium, they are more willing to hold value stocks. They don’t demand as high of an expected return as they used to demand to hold value stocks because they know the premium has existed in the past, so they think it’s “safer.” This means that the forward looking expected returns for value stocks are lower (remember, as prices go up, expected returns go down). And because the expected returns are lower, negative returns will be more frequent.

There are two problems with this argument.

It’s actually perfectly reasonable to think that the expected return of the value premium – or any other premium – has changed over time. Investors are constantly changing their preferences, so it may very well be true that the premium has dropped (more on this later). The problem is that this might get at the relative attractiveness of the value premium (how’s that for a catch-22?), but it doesn’t explain why value has had such a bad decade and a half.

Prices, including the relative prices of value and growth stocks, move based on how new information squares with what the markets expected to happen next. The value premium would still have roughly a 50/50 chance of outperforming (or underperforming) it’s “true” value.

We get to the second problem if we push a little further and argue that the expected return of the value premium is actually negative now. This would certainly explain why value stocks have done so badly for so long, but the problem with this argument is that markets just don’t work this way. Basically, why would anyone be willing to hold a security they expect to lose money relative to a less risky security? Presumably, the prices would drop to the point that someone thought there was a reasonable positive expected return to holding value stocks. At which point we would be back to “normal,” just at a lower price level.

Markets are constantly repricing risk, but that doesn’t explain what we’re seeing with value.

So what is going on?

Risk is Risky

People like comprehensible stories. We want to feel like the world is understandable, and that there are specific, tangible, reasons that we can point at to explain why things happen the way that they do. But that’s not always how the world works. Sometimes bad things happen, and then keep happening, simply by chance. That’s likely what’s been happening with the value premium now.

The value premium is having a historically bad run, but that’s what risk means. If we didn’t have periods like this one, it wouldn’t be risk. The market wouldn’t need to compensate us for holding the riskier value stocks. Right now, we are earning that value premium.

While we may not know when Fortuna will decide that we’ve finally had enough, there are some promising rays of sunlight breaking through the clouds with regard to what we might be able to expect from the value premium in the future.

What’s the Spread?

Before we get into these glimmers of sunlight, it’s important to stress that we really can’t predict what the markets will do with any specificity. In any given year I expect value stocks to beat growth stocks. That’s true this year, it was true last year, and it will be true fifty years from now. But we obviously know that all of these predictions can’t be correct, and we have no way of knowing when value stocks will lose, or when they will stop losing.

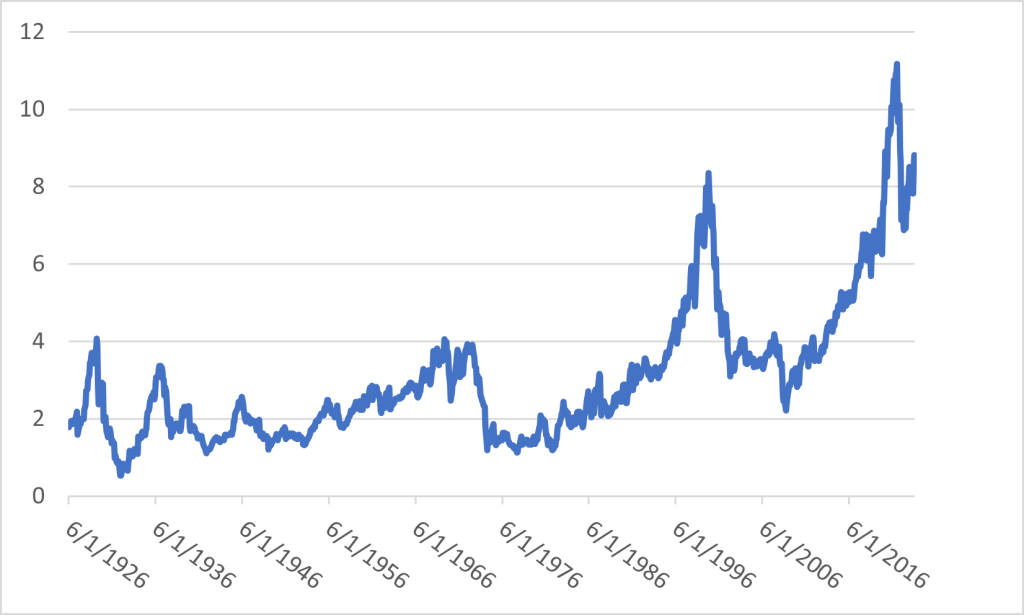

But there are some reasons for optimism about the value premium. A big reason to be optimistic is the spread between the Price to Book ratios of value and growth stocks. This spread is one of the ways that we can get some sense of what the current expected return of the value premium is. The bigger the spread, the higher the expected return of the value premium. And right now, the spread is just about as big as it’s ever been since 1926.

Spread Between the P/B of US Growth and Value Stocks

We haven’t seen spreads even close to this since the last days of the tech book. Now, I want to be careful here – this does not mean that we are guaranteed some massive value premium to “make up” for all of the bad returns that value stocks have gotten over the past nearly 20 years. It doesn’t even mean that we will necessarily have a positive value premium in the next couple years. There are no hot hands in finance. This is all based on risk, and we’ve had a pretty sizable spread for a while now.

But it does mean that the expected return of the value premium is likely higher than it’s ever been. If you were comfortable with the value premium in the past, the arguments in favor of the value premium would seem to be even more convincing. Essentially, we’ve taken all of the pain, so we want to make sure that we stay positioned to capture the gain from the value premium.

Has the Value Premium Changed?

The obvious question here is whether something has changed. Is there something fundamentally different about the market, or value stocks specifically, that is fundamentally different than it was 20 years ago? Especially given how consistent the value premium seemed up until that point.

There are always things we can point to – we’re really good at finding patterns and rationalizing – but there’s no obvious culprit to explain how this time it’s different.

However, it is important to call out that this is one of those situations where it’s impossible to prove a negative. While the Efficient Market Hypothesis is a really good explanation for how the financial markets work, it can’t be perfect. Humans, and the financial markets, are messy. And it’s entirely possible that some amount of the value premium was simply investors consistently making the same mistake over and over (in other words, mispricing value stocks).

And if that is true, maybe investors simply stopped making the same mistake. Which would explain the situation if the value premium simply went to zero.

But to explain the negative premium that we’ve been seeing, investors would have had to stop consistently overvaluing value stocks, and started to overvalue growth stocks. This isn’t impossible – it’s basically human nature to overcorrect when we realize our mistakes – but it seems highly unlikely that this is the whole, or even a big part of, the story. The underlying logic of the value premium is simply too powerful.

Should You Include a Value Tilt in Your Portfolio?

While this is all incredibly interesting (or at least I think so, and you probably do too if you made it this far), we’re left with the practical question. Should you include a tilt towards value stocks in your portfolio.

To which I answer with a resounding, it depends.

We know that the most efficient portfolio is the market portfolio. This should always be our baseline. But, depending on how you are different from the average investor, you may want to tilt your portfolio away from that market portfolio. One of the ways that you might want to tilt your portfolio is to tilt your equity portfolio either towards higher returns (and higher risk), or towards lower risk (and lower returns).

And using the value premium, as well as all of the other risk premiums that the market has on offer, is a really great way to do that. The decision that you need to make is whether you like the risk and reward tradeoffs that these risk premiums offer up. Does the higher potential return from the value premium offer enough benefit to outweigh the additional return?

That’s something that you need to decide for yourself.

But it’s important to remember that the market is always looking forward. The past doesn’t matter, except in so far as it informs what the future could look like. We need to take the same approach with our portfolios. Just because value has seriously underperformed doesn’t mean that the market “owes us” anything. But it also doesn’t mean that value is dead either. We need to be continually reevaluating our portfolios and working to make sure that they are positioned to give ourselves the best chance to capture the returns the market is putting on offer so that we can reach our retirement goals.

And there is every reason to believe that the value premium will be a big part of that going forward.

To find out more about how to build an investment portfolio that works for you, read our eBook 9 Principles of Intelligent Investors.