Changing directions, another optimistic assumption of classic safe withdrawal rate studies is that retirees are able to earn precisely the underlying index returns net of the risks. Three truths dispute that idea:

- Actively managed funds do not precisely match the underlying benchmarks,

- Many investors may make behavioral and timing mistakes of buying high and selling low, and

- Investing costs that reduce returns below the benchmark levels.

In reality, many investors may experience investment returns that lag behind the annually rebalanced and indexed portfolios enjoyed by the hypothetical retiree used in the safe withdrawal rate studies.

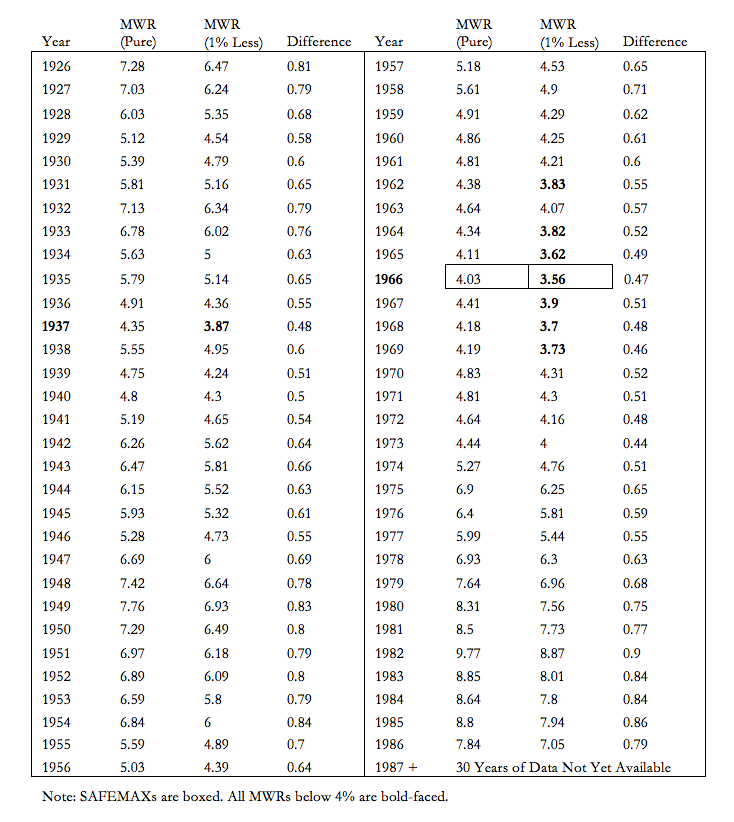

It is important to consider the impact of account underperformance relative to benchmarks. In Exhibit 1, I consider the impact of 1% annual account underperformance relative to the index returns, with every other assumption matching my discussion of William Bengen’s work on the SAFEMAX. These assumptions include withdrawals taken at the start of the year, annual rebalancing from a 50/50 portfolio of stocks and bonds, a thirty-year retirement, and inflation-adjusted withdrawal amounts. The exhibit shows the pure Bengen results and the results when annual returns are one percentage point less than the underlying indices.

In both cases, 1966 retirees are the source of our SAFEMAX. With the index returns, a 1966 retiree could sustain withdrawals over thirty years using a 4.03% withdrawal rate. With 1% underperformance, the SAFEMAX fell by 0.47 percentage points to 3.56%. From the perspective of the SAFEMAX, 1% underperformance would have resulted in reduced potential spending power of 11.9%. Across the historical period, underperformance caused the maximum sustainable withdrawal rates to fall on average by 0.65 percentage points, or 10.9% of spending power.

Despite common misconceptions, a one-to-one tradeoff between underperformance and withdrawal rates does not exist. As the portfolio decreases in size, underperformance impacts a smaller amount of wealth, while real withdrawal amounts for retirement spending do not change. This explains why the 4% rule did not become the 3% rule in response to the underperformance.

Exhibit 1

Maximum Sustainable Withdrawal Rates (MWRs)

Cases: (1) Earn Underlying Index Returns, (2) Underperform Index by 1% Annually

For 50/50 Asset Allocation, 30-Year Retirement Duration, Inflation Adjustments

Using SBBI Data, 1926-2015, S&P 500 and Intermediate-Term Government Bonds