WHAT IS OCCAM’S RAZOR? Occam’s Razor is a principle attributed to William Occam, a 14th century philosopher. He stressed that explanations must not be multiplied beyond what is necessary. Thus, Occam’s Razor is a term used to “shave off” or dismiss superfluous explanations for a given event. This concept is largely ignored within the investment management landscape. This newsletter will “shave off” popular investment misinformation and present what is important for achieving long-term investment success.

Everyone likes the markets when stocks are going up. We’re all getting the returns that we are “supposed” to be receiving for putting our money at risk. Naturally, we aren’t big fans of the market when stocks start falling. Unfortunately, stocks are “supposed” to go up and down – a lot. The financial markets are based on the relationship between risk and return. We wouldn’t be able to harvest the long-term returns we expect without the risk. And, well, this is what risk looks like.

Looking at the S&P 500 Index, this past quarter has been the worst in about a decade, and the second worst since the end of the 2008 financial crisis. It’s also only the 3rd quarter since the 2008 financial crisis with a return worse than -10%. For what it’s worth, which isn’t a whole lot, in both other cases the S&P 500 was up by more than 10% the next two consecutive quarters. However, what we really care about is what is going to happen next this time around. Does this ugly past quarter presage an extended downturn, or was it just a bad quarter? Is this bull market, which has been one of the longest ever, finally coming to an end?

As unsatisfying as this answer is, we just don’t know. In fact, we can’t know. The markets are unpredictable in the short-term (and short-term is a lot longer than most people accept), because the markets react to new information, and specifically how that new information squares with what the markets expected. Everyone in the markets already knows that we’ve had an amazing run this past decade, and where all of the valuation metrics are. They’ve priced in that information, and the current prices are the market’s best estimate of the value of the stock market.

Now let’s say for a second that this past quarter is the start of a bear market. I want to look at two questions: in historical extended downturns(1), how sensitive has market timing been to calling the bottom of the market correctly, and also, how much of a downturn’s drop has come in the first few months (since we’ve already taken those on the chin)?

As we’ve seen in the past, market timing is an incredibly fragile strategy. If you have perfect information about how the market will perform, then you’re probably going to do pretty well, but the returns start degrading pretty significantly as you introduce even small amounts of uncertainty. In that last article, we were looking at market timing over the broad sweep of history. Here, I want to specifically look at the extended downturns. If you are trying to avoid getting hurt too badly during a down market, and have pulled out of stocks, what are the costs of incorrectly predicting when the markets will turn around? In other words, how much are you giving up if you stay out of the market a little bit too long, and how badly will you be hurt if you get back into the market a little bit early?

Well, let’s look at the data.

Using our definition of an extended downturn, there have been nine extended downturns since 1926.

| Name | Top | Bottom | Recovery | Months from Top to Recovery | Decline from Top to Bottom |

| Great Depression | 8/29 | 6/32 | 1/45 | 185 | -83.41% |

| Mid 40’s | 6/46 | 11/46 | 10/49 | 41 | -21.76% |

| Early 70’s | 11/68 | 6/70 | 3/71 | 28 | -29.23% |

| Mid 70’s | 12/7 | 9/74 | 6/76 | 42 | -42.62% |

| Late 70’s | 12/76 | 2/78 | 7/78 | 19 | -14.12% |

| Early 80’s | 3/81 | 6/82 | 10/82 | 19 | -15.33% |

| Crash of 1987 | 8/87 | 11/87 | 5/89 | 21 | -29.53% |

| Tech Crash | 8/00 | 9/02 | 10/06 | 74 | -44.73% |

| 2008 Crisis | 10/07 | 2/09 | 3/12 | 53 | -50.95% |

Period from 1926-2018. Using month end data. Data from Morningstar. Recovery is the month where the S&P 500 ends above the previous top of the market at the beginning of the downturn.

One of the first things that should strike you is that, aside from the 70’s (which was a bad decade for all sorts of reasons), we haven’t had too many extended downturns, though on average they have been pretty painful (which makes sense since these are the really bad periods for the stock market). These nine periods have averaged a 37% drop from the top of the market immediately before the downturn to the bottom of the market during the downturn. It’s safe to say that there’s a lot of appeal to being able to get out of the markets and avoiding these losses, but market timing is a risky game. It’s a game where you have to be right twice – once when you decide when to get out, and then again when you decide to get back in.

Let’s make it a little bit easier, and assume that you have already gotten out (we’ll deal with this question in a bit). Just how important is the decision on when to get back into the market?

To answer this, we want to look at the returns right around the bottom of the markets for these periods to see how big of a deal missing the bottom by a few months is for your portfolio. Obviously if you get back into the market too early you’ll be taking actual losses as the market keeps dropping until it hits the bottom. If you miss the bottom by waiting too long, you miss out on the returns you would have gotten, and markets tend to rebound reasonably quickly after a drop. So neither method is ideal.

Let’s start by looking at the direct losses that you would have incurred by calling the bottom too early and jumping back into the market as it’s still falling.

| Name | Enter 1 Month Early | Enter 2 Months Early | Enter 3 Months Early |

| Great Depression | -0.22% | -22.13% | -37.68% |

| Mid 40’s | -0.27% | -0.87% | -10.75% |

| Early 70’s | -4.82% | -10.03% | -18.03% |

| Mid 70’s | -11.70% | -19.01% | -25.16% |

| Late 70’s | -1.61% | -7.47% | -7.03% |

| Early 80’s | -2.15% | -3.85% | -6.62% |

| Crash of 1987 | -8.19% | -27.95% | -29.53% |

| Tech Crash | -10.87% | -10.28% | -17.28% |

| 2008 Crisis | -10.65% | -18.18% | -17.31% |

| Average | -5.61% | -13.31% | -18.82% |

Total returns using month end data. Data from Morningstar. See previous table for specific time periods.

Calling the bottom too early hasn’t been monstrously painful during these extended downturns, but during both the Tech Crash and the 2008 Crisis, the S&P 500 was down over 10% during the month where the market hit bottom. Now, look at what happens if you entered the market 3 months early. On average, you would have lost nearly a fifth of your money, and being able to call a market bottom within 3 months is something that everyone at CNBC would kill for.

So let’s turn our attention to the other side of the bottom. What’s sort of returns would you have foregone if you got into the market too late?

Well, here you go:

| Name | Enter 1 Month Late | Enter 2 Months Late | Enter 3 Months Late |

| Great Depression | 38.15% | 91.60% | 84.97% |

| Mid 40’s | 4.57% | 7.24% | 6.41% |

| Early 70’s | 7.52% | 12.99% | 16.91% |

| Mid 70’s | 16.57% | 11.35% | 9.38% |

| Late 70’s | 2.76% | 11.70% | 13.22% |

| Early 80’s | 12.67% | 13.91% | 26.74% |

| Crash of 1987 | 7.38% | 11.97% | 17.23% |

| Tech Crash | 8.80% | 15.21% | 8.44% |

| 2008 Crisis | 8.76% | 19.17% | 25.83% |

| Average | 11.91% | 21.68% | 23.24% |

Total returns using month end data. Data from Morningstar. See previous table for specific time periods.

Just like getting into the market too early, getting back in late isn’t a pretty picture. Waiting to be sure that the market’s turned around has been pretty darn costly. Once you miss these returns, they are gone forever. And again, being able to predict the bottom of the market within 3 months would be superhuman (as in basically impossible) prescience. Anyone who says that they can predict what the markets are going to do is lying to someone – either themselves, or you.

So now that we know that not being able to predict the bottom of the market is bad for market timing during an extended downturn, let’s look at the market as the downturn is starting. If the market is really entering an extended downturn, this is where we are right now, so there’s some special significance for us with this one.

What I want to know here is how much a downturn’s drop from the top at the beginning of the downturn to the bottom happens in the first few months (essentially what we’ve just experienced in this past quarter).

| Name | % of Drawdown After 1 Month | % of Drawdown After 2 Months | % of Drawdown After 3 Months |

| Great Depression | 5.71% | 28.24% | 39.66% |

| Mid 40’s | 17.00% | 27.58% | 56.69% |

| Early 70’s | 13.75% | 15.99% | 29.88% |

| Mid 70’s | 3.73% | 11.42% | 11.46% |

| Late 70’s | 34.64% | 44.81% | 52.71% |

| Early 80’s | 13.90% | 9.94% | 15.08% |

| Crash of 1987 | 7.45% | 78.71% | 100.00% |

| Tech Crash | 11.80% | 12.70% | 29.32% |

| 2008 Crisis | 8.21% | 9.51% | 20.72% |

| Average | 12.91% | 26.54% | 39.50% |

Total returns using month end data. Data from Morningstar. % of Drawdown is the total loss after 1, 2, or 3 months divided by the total decline from the top to bottom of the market during an extended decline. See previous table for specific time periods.

Total returns using month end data. Data from Morningstar. % of Drawdown is the total loss after 1, 2, or 3 months divided by the total decline from the top to bottom of the market during an extended decline. See previous table for specific time periods.

In short, if we have entered an extended downturn (and the historical precedents tell us anything), we’ve likely already taken a pretty big chunk of the total loss that we will take before the markets turn around. Which would obviously further limit the effectiveness of market timing as a strategy to avoid taking the losses from an extended downturn.

What this tells us is that market timing doesn’t work if you can’t predict what the market is going to do (I’ll pause while you pick your jaw up off of the floor). So can you predict what the market is going to do?

No.

As we discussed earlier, the markets move based off of new information. The markets are an incredibly complicated, self-correcting system which aggregates all of the available information and comes to an equilibrium price for every security. This doesn’t mean that this is the “right” price (whatever that actually means), just that this is the price where the security is currently clearing – the price where buyers and sellers of the security meet. This is based on what the market participants are actually doing, based on everything that they know about the security. The participants have effectively brought all of that information to bear on setting the security’s price.

This means that the information that the market does not have (what happens next) is what will move prices. But it’s not simply whether the next piece of news about a company is good or bad. What matters is if that next piece of news is better or worse than what investors thought was going to happen. They’ve already built their expectations into what they are willing to pay for a security.

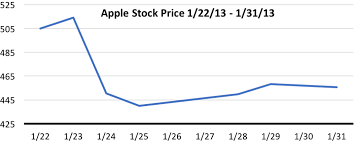

A great example of this is Apple, back in the beginning of 2013.

Source: Yahoo! Finance

From this chart, you can probably guess the gist of the story here – Apple had a very bad day – but why it was a bad day is what we’re after.

Apple released their results from the fourth quarter of 2012 on January 23rd, and these weren’t just regular results. Apple was announcing record breaking profits; in fact, they were the second best quarterly profit numbers of any company ever up to that point. So what did the stock do? Well it tanked, of course. Apple’s stock dropped by 12% immediately after they announced the second best quarter of any company, ever.

What happened? Well, everyone thought that they would do even better. Everyone was anticipating that Apple’s profits numbers would be even higher, and now that this new information came out, they needed to reassess their expectations. It wasn’t that Apple had a bad quarter per se (it was still the second best quarter of any company up to that point), it was just that everyone thought it would just be even better.

I have no clue whether the market will be going up or down from where we are today. We may have hit the end of this incredibly long bull market, or it may just keep on trucking, but here’s the thing: no one else does either. All the clever and nuanced analysis you hear on TV (or not so clever and nuanced as the case may be) is largely meaningless for us as investors. By the time that something makes it onto TV or into the Wall Street Journal, the financial markets have largely absorbed that information and prices have moved to take it into account (including what it likely means for the future). For information to be useful to us as investors, we would need to be able to process it, and act on it, before nearly anyone else. And realistically, that just isn’t going to happen. What we want to do instead is make the broad sweep of the market our ally, not our adversary. We want to focus on building a financial plan that will help us reach our financial goals, and harvest the long-term returns that the market puts on offer.