A lot of the resources on retirement planning assume a planning horizon of thirty years. In fact, that’s one of the explicit assumptions with the 4% rule. And historically, that’s been a relatively decent assumption.

But we’ve been seeing life expectancy increase over time (and it’s likely to just keep increasing into the future). Which means that you may want to plan for a longer retirement.

How long will your retirement last? The impossibility of answering this question with any long-term accuracy is one of the key challenges of planning a retirement income strategy.

Working with Longevity Risk

The nature of longevity risk is that we know our life expectancy, but it is based on an average with a great deal of variability. Two general approaches exist to deal with this unknown element of longevity:

- Planning for fixed retirement durations that are generally somewhere beyond life expectancy, and

- Making plans that specifically incorporate mortality rates by age into the calculations.

The former method is the most common (the 4% rule’s fixed thirty-year horizon uses this method) and easiest to work with, but both approaches have their strengths.

Fixed Retirement Horizons

Planning for a specific retirement time horizon begins by selecting a horizon you are unlikely to outlive, and then developing a plan that covers the entire time. The horizon should be greater than life expectancy, as retirees have a 50% chance of living longer.

In 1994, Bill Bengen considered thirty years to be a reasonable planning horizon for sixty-five-year-old couples, resulting in a planning age of ninety-five.

Today however, many people use longer planning ages. We are simply living longer than we did in the past. And it’s very likely that medical advances will continue, meaning that current retirees will benefit from treatments that don’t exist today – meaning that future life expectancy is likely to continue to increase.

Depending on how conservative they would like to be, many people are using planning ages of 100 or 105 to account for these longer lifespans. This means that someone retirement at sixty-five years old would need to plan for a thirty-five or forty-year horizon, respectively.

The assumed retirement duration is of utmost importance. Retirement simulations based on longer time horizons will guide optimal retirement income solutions toward:

- Lower withdrawal rates,

- Higher stock allocations, and

- A stronger case for guaranteed income retirement products.

Writing in Harold Evensky and Deena Katz’s Retirement Income Redesigned, Bob Curtis makes a convincing case for fixed horizons. He argues that longevity is not a “probability problem” but a “possibility problem,” adding:

“What possible sense does it make to tell your client that she can spend more money now because you’re assuming in some of the Monte Carlo iterations that she’ll die early? How does a person die ‘some of the time?’”

It is a good question. But at the same time, does it make sense to lower spending now so you can plan to spend just as much at 100 as at age sixty-five, despite the low chance of living to 100? Yes and no are both acceptable answers to this question, as it truly depends on your unique preferences regarding these tradeoffs.

Variable Retirement Horizons

Planning for a longer horizon by spreading out distributions from your portfolio is the conservative approach. (Traditional safe withdrawal rate studies ignore this risk entirely, focusing solely on minimizing failure.). You will have to spend less and will most likely leave a larger than planned bequest.

On the other hand, planning for a shorter horizon could leave you exposed to overspending, which means you could outlive your wealth. For some, the risk of cutting spending and missing out on enjoying hard-earned wealth outweighs the risk of overspending.

The impact of this risk varies from person to person depending on the value each would get from additional spending.

However, as we have seen when looking at life expectancy is that longevity risk is a contingent risk. As we age our life expectancy actually increases – or more specifically, it decreases slower than we age.

As a practical example, it is much more likely that a 99 year old will live to be 100 than a 65 year old. Essentially, the 99 year old has not died prior to being 99, whereas the 65 year old still has the possibility of dying before reaching 99.

This means that instead of using a fixed horizon we can plan on adjusting our planning horizon through time.

Instead of simply saying that your will use a planning age of 100 or 105, you can start there, and then adjust your planning horizon based on your individual circumstances. Not only will you be able to adjust your planning horizon based on your “new” life expectancy as you age, but you can also incorporate information about your personal health.

Adjusting Your Spending Through Time

Whether we use a fixed or variable planning horizon, it’s important to understand how our sustainable spending rates change depending on the length of our retirement planning horizon.

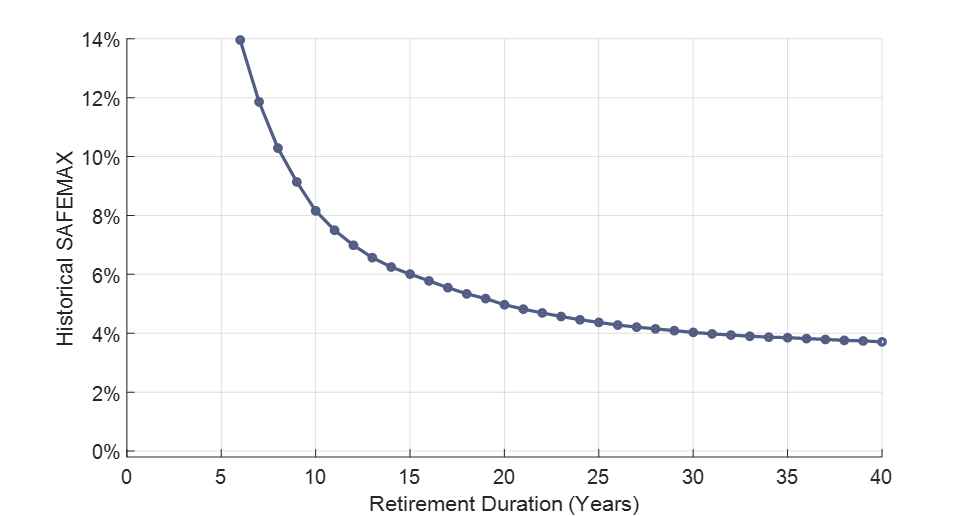

Using the historical data from 1926 through 2022, and all of the baseline assumptions—including a 50/50 allocation to the S&P 500 Index and intermediate-term government bonds—we can see William Bengen’s SAFEMAX withdrawal rate for retirement horizons between five and forty years.

We saw before that the SAFEMAX for a thirty-year retirement is slightly above 4%.

However, as we increase our retirement duration to 40 years, the historical SAFEMAX dops down to roughly 3.7%.

Whether you are using a fixed or variable planning horizon, using these historical SAFEMAX withdrawal rates for different retirement durations can help you think through how you might set your spending rate through time.