Most people don’t think too much about their bonds. They really are the boring foundation for your portfolio. However, occasionally they spring to the surface, and this is one of those times. Lately, a number of people have been wondering why they should be investing in bonds, since we’re obviously in a period of rising interest rates.

One of the first things that finance students learn is that bond prices (and therefore bond returns) are inversely related to interest rates. Considering that all else is equal, when interest rates are going down, bond prices will go up, and when interest rates are going up, bond prices will go down. This is fundamental to how finance works, and this raises the obvious question of why you would want to hold bonds when rates are rising – why would we choose to lose money?

Start at the Beginning

Before we dig into that question, I want to start with something even more fundamental. Why do we hold bonds at all? They have lower returns than stocks, so why would we want them in our portfolio? The answer is fairly straightforward. We (or at least most investors anyway) want them in our portfolio because they give us the ability to specifically target the level of risk that we want in our portfolio. Bonds may not bring in the returns that you can get from stocks, but that’s not their job. Their job is to help you sleep soundly at night. They are there to keep your portfolio pointed in (roughly) the right direction – while your stocks are jumping all over the place.

And bonds are able to help us control the level of risk in our portfolios in two different ways. The first is that bonds are just less risky than stocks. But more importantly, stocks and bonds have a relatively low correlation with each other. This means that they tend to move differently from each other, so as one is zigging, the other is (probably) zagging. This smooths out the total portfolio’s returns and makes it much easier for you to stay disciplined and harvest the long-term returns that will help you achieve your goals.

But still the question remains: if we know that rising interest rates will cause bond prices to drop, why would we hold bonds when interest rates are rising?

I Know That You Know That I Know…

Well, if we knew when interest rates were rising, we probably wouldn’t really want to hold bonds at that point – provided we could do something about it before the market. The thing is, while we are actually able to predict when interest rates are likely to go up (we all have access to pretty much the same information that the Fed does), that predictability means that everyone else is making the same predictions. And they trade on that information – by the time that we recognize that interest rates are going to rise, that’s already incorporated into the price.

The old adage that the best predictor of future interest rates are today’s interest rates doesn’t mean that we don’t expect any changes in the market; we know that there will be changes. It means that the market’s current expectations are already priced in. The market is reflecting the consensus estimate of what will happen next, and the market will move based on what the next piece of information is and how that next piece of information squares with what the market expected.

In other words, if everyone expects that interest rates are going to rise, then that information is already included in the price, and we can see this in the data.

If we look at the correlation of the bond market with the Effective Federal Funds Rate (and if you don’t remember what this is, you should take a look at our article on How the Fed Impacts Your Investments), we see some pretty interesting things.

| One Month Treasury Bills | Five Year Treasury Notes | Long Term Government Bonds | Long Term Corporate Bonds | |

| Correlation with the Effective Federal Funds Rate | -0.05 | -0.19 | -0.11 | -0.15 |

Data from August 1954 through April 2018. Data courtesy of Morningstar. Past performance is not indicative of future performance. Indexes not available for direct investment.

Now, one quick note. Remember that interest rates are inversely related to bond prices, so we should expect those negative correlation numbers. As interest rates go up, we would expect bond prices to go down, and vice versa. We should also notice that the correlation numbers aren’t particularly high, (with the exception of the One Month Treasury Bills) though they are all statistically significant. There is a relationship there. I also want to add one more row to this table. I want to see what happens if we look at the correlation between the Effective Federal Funds Rate and the bond returns of the previous month:

| One Month Treasury Bills | Five Year Treasury Notes | Long Term Government Bonds | Long Term Corporate Bonds | |

| Correlation with the Effective Federal Funds Rate | -0.05 | -0.19 | -0.11 | -0.15 |

| Lagged Correlation with the Effective Federal Funds Rate | -0.08 | -0.22 | -0.19 | -0.15 |

Data from August 1954 through April 2018. Data courtesy of Morningstar. Past performance is not indicative of future performance. Indexes not available for direct investment.

You’ll notice that all of the correlations with the month lag are at least as strong as the regular correlations. This means that the market is incorporating it’s assumptions of what the Federal Funds Rate is going to be doing (or at least incorporating the information driving the Federal Funds Rate). Which in turn means that if you are reacting to what interest rates are doing you’ve already missed the bus. The market has already moved on to the next thing.

And, again, we can see this in the data. If we lag the correlations the other way, so that we’re looking at the correlation of the Effective Federal Funds Rate and bond returns in the subsequent month, there’s really no correlation to speak of at all. The largest correlation is 0.03, and none of them show any inkling of a hint of statistical significance.

If you’re trading on information that you’ve seen on the news, it’s not going to work out well for you. If it’s on CNBC, it’s a fair bet that the information was already incorporated into prices before you saw it.

In other words, market timing doesn’t work. It doesn’t matter if you’re trying to time the stock or the bond market, you can’t time the markets.

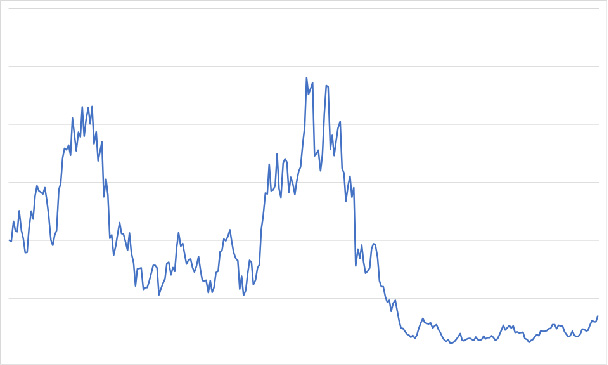

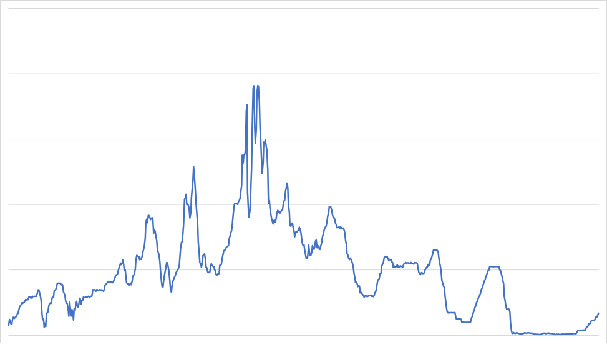

Now a lot of the time people will agree with the idea that you can’t time the markets in theory, but “this time it’s obvious what the markets are going to do and you’d be crazy not to either protect yourself or take advantage of it,” depending on the situation. Well, to that, I’ll simply present two charts. One is a plot of the Effective Federal Funds Rate from July 1954 through April 2018, and the other is a chart of a random series based on the average return and standard deviation of the Effective Federal Funds Rate. If there are periods where market movements are obvious, then it shouldn’t be hard to figure out which is which, right?

Well, here’s the first chart:

And here’s the second chart:

So, which chart is which? If you’re curious, the answer is in the footnotes. In fact, unless you’re looking at long-term data, it’s essentially impossible to tell market returns from a coin flip.

Harvest Your Long-Term Returns

So where does this leave us? We know that rising interest rates are bad for our bonds, but we don’t have the ability to predict when interest rates will actually be rising or falling. Well, it leaves us in the same place as we always were – focus on the long-term. Harvest the long-term returns of a risk-appropriate and properly diversified portfolio. Thankfully, this is a pretty good place if you can stay disciplined.