When it comes to Social Security, deciding when to claim is one of the most important financial decisions you’ll make in retirement. Yet, many people claim early, sometimes without fully understanding the impact of this decision on their long-term financial well-being. This article delves into when people are claiming Social Security, and what factors drive these choices.

Key Claiming Ages: Early, Full, and Delayed

Most people have three key milestones when considering Social Security: early eligibility at age 62, full retirement age (FRA), and delayed retirement credits that max out at age 70. These claiming options result in significantly different monthly benefits.

- Age 62 (Early Eligibility): The earliest you can claim Social Security, but your monthly benefits will be permanently reduced. For example, if your full retirement age is 67, claiming at 62 results in a 30% reduction in monthly benefits.

- Full Retirement Age (FRA): For those born between 1943 and 1954, FRA is 66, but it gradually increases to 67 for those born after 1960. Claiming at this age provides the full, unreduced benefit.

- Age 70 (Delayed Credits): If you delay claiming until age 70, you’ll earn delayed retirement credits, increasing your benefit by 8% for each year after FRA. For someone whose FRA is 67, delaying until age 70 can result in a 24% higher monthly benefit.

Popular Claiming Patterns

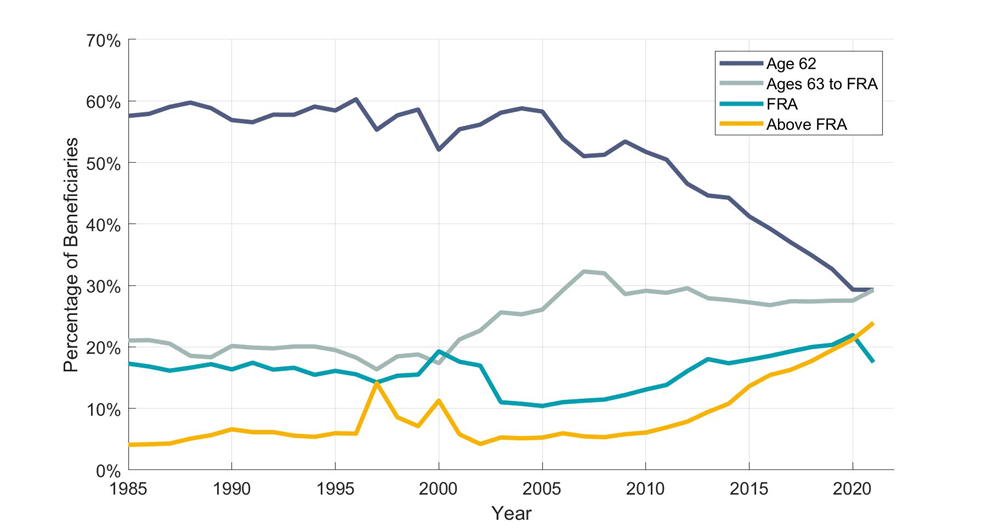

Despite the potential financial advantage of delaying Social Security, many Americans still claim early. According to the 2022 Annual Statistical Supplement to the Social Security Bulletin:

- At Age 62: More than 27% of beneficiaries claim benefits as soon as they become eligible. This decision is often driven by immediate financial needs, health concerns, or the belief that they won’t live long enough to benefit from delayed claiming.

- Before Full Retirement Age: 31% of beneficiaries claim before reaching their FRA, locking in reduced benefits for life.

- At Full Retirement Age: Only about 16% wait until FRA, even though this would provide them with their full benefit amount.

- After Full Retirement Age: Roughly 25% of retirees delay until age 70, garnering the significant increase in benefits from delayed credits.

Age Distribution of New Social Security Retirement Beneficiaries

Why People Claim Early

While the financial benefits of waiting are clear, several factors often push people to claim early:

- Health: Those with poor health or shorter life expectancies may opt to claim early, reasoning that they won’t live long enough to benefit from delaying.

- Job Loss or Financial Need: Many individuals face unexpected job loss in their early 60s or need the income immediately due to insufficient savings, leading them to claim early benefits as a financial safety net.

- Lack of Understanding: There’s a common misconception that claiming as soon as possible maximizes lifetime benefits. In reality, delaying can often result in significantly more total benefits over a longer retirement, particularly for those with longer life expectancies.

The Cost of Early Claiming

Claiming Social Security early comes at a high cost. For example, consider someone whose full retirement benefit at age 67 would be $2,000 per month. If they claim at 62, their benefit drops to around $1,400—permanently. Over a 20-year retirement, this can result in a loss of $144,000 in benefits.

The following table highlights the percentage reduction in benefits for claiming early:

| Claiming Age | Reduction (Relative to FRA) |

| 62 | 30% |

| 63 | 25% |

| 64 | 20% |

| 65 | 13.3% |

| 66 | 6.7% |

| 67 | 0% |

The Benefit of Delaying

On the other hand, delaying Social Security can provide substantial financial benefits. For those able to wait until age 70, the benefit increase from delayed credits can significantly boost monthly income in retirement. Here’s an example:

| Claiming Age | Monthly Benefit (Assumes FRA = 67) |

| 62 | $1,400 |

| 67 | $2,000 |

| 70 | $2,480 |

This strategy is particularly advantageous for individuals who expect to live into their late 80s or beyond, as the higher monthly benefit more than compensates for the delay in starting payments.

Conclusion

Deciding when to claim Social Security is a deeply personal decision that depends on factors like health, financial need, and life expectancy. While many claim early, those who delay can significantly increase their lifetime benefits. Understanding the financial impact of your decision—and being aware of common claiming patterns—can help you make an informed choice that aligns with your long-term retirement goals.