Bonds serve as the foundation of many people’s retirement plans. Because of their reasonably predictable nature they are able to both temper the risk to your investment portfolio from stocks, as well as provide a stream of reliable income when held as part of a bond ladder. However, the mechanics of how bonds are priced – and subsequent bond returns – is often confusing for investors.

Put simply, the price of a bond is the discounted present value of all of the payments that the bond will provide, including both any coupons that the bond will pay as well as the face value that will be repaid at the bond’s maturity.

Bond Pricing in Practice

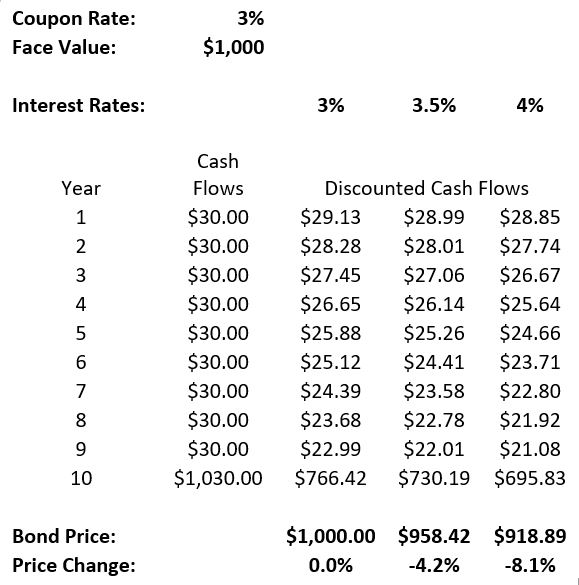

But this explanation confuses more than it illuminates. Let’s look at an example to understand how this works in practice. As a simple example, let’s consider a 10 year bond with a face value of $1,000 and a coupon rate of three percent. To keep the math simple, let’s assume that the coupon is paid at the end of the year, rather than in two equal payments as is typical.

In this simple example, one coupon payment of $30 (3 percent of $1,000) is made at the end of each year for ten years to the bond’s owner(s) on those dates, and the face value is paid in full at the end of the tenth year.

But we need to be able to determine how much we value the payments out in the future today. A dollar today is worth more than a dollar ten years in the future. This is where the “discounted present value” part of the explanation comes in.

Without diving too deep into the details we can use an interest rate to estimate how much we (and more importantly, other investors) think a bond’s future payments are worth today. In this example we will consider three different interest rates: 3 percent, 3.5 percent, and 4 percent. We want to consider multiple interest rates so we can see how changes in interest rates will impact bond prices.

Understanding Discounting

Before we look at the numbers, I want to be clear about what the discounted value of these payments means. Even over a relatively short period of time (and yes, ten years is a short period of time in investing) and with a relatively low interest rate, the discounted present value of a payment can be significantly lower.

As an example, the discounted value of the cash flow from the bond in year 10 – which includes both principle repayment and the $30 annual coupon. Instead of the $1,030 you would expect, with a 3 percent interest rate it is only worth $766.42.

To understand how this works, imagine placing this amount in a bank account that earns an annually compounded 3 percent return each year. After ten years, it will grow to be $1,030, which is the amount of the cash payment provided in year ten. In other words, an investor would need to set aside $766.42 today in order to have $1,030 in ten years if the funds grew at a 3 percent annually compounded return.

If interest rates are instead at 3.5 percent, then the value of all of these future payments would be worth even less. In a competitive and active market, bonds with the same maturity and risk characteristics must offer the same potential return for both parties to agree to a trade. In this case, the future cash flows are discounted at 3.5 percent, and the sum of these discounted cash flows (and potential selling price) is $958.42.

Bond Payments (Usually) Don’t Change

In this example – as with almost all bonds an investor might purchase – whoever owns the bond is entitled to the predefined cash flows of $30 per year plus $1,000 more in the final year. These cash flows do not change with interest rates. One of the few exceptions to this rule is TIPS, or Treasury Inflation Protected Securities, which adjust to provide inflation protection.

Bond Prices Do Change

But if a bond’s payments don’t change, why would someone buy a bond that pays a lower coupon than the prevailing interest rate?

Because the price of the bond changes.

Typically, bonds are issued with their coupons set near the prevailing interest (though this is different for each bond issuer). When their coupon is equal to the interest rate that investors associate with the bond, it will trade at it’s face (or principle) value. When this happens, the bond is said to be trading at “par”. But even if the bond issuer was able to get it right initially, the bond market doesn’t stay still very long. Almost immediately something will change, and investors will either increase or decrease the interest rate they are associating with the bond. And this will mean that the price of the bond will either go up or down.

But one of the most interesting things about bond prices is how they change for a given change in interest rates. To see this, let’s look at the numbers for our example.

When we change the interest rate (usually called the bond’s yield to maturity in this context) a small amount, we can see a sizable change in the price of the bond.

For instance, moving from an interest rate of 3% to 3.5%, the price of the bond drops by more than 4%. The specifics of this relationship is a little beyond the scope of this article, however, the farther out the bond’s maturity date is, and the larger a proportion of the bond’s cash flow it’s final principle repayment is, the more sensitive the bond will be to changes in interest rates. This sensitivity is measured by what is called the bond’s duration.

The Interest Rate See-Saw

One of the most important things to understand about bond pricing is that a bond price and interest rates are inversely related.

When interest rates go up, bond prices go down. And when interest rates go down, bond prices go up.

This is because a bond’s payments do not change. No matter what happens with interest rates you will always receive exactly the same payments. However, the value of those payments will change based on the prevailing interest rates.

Though this may seem basic and simple as I explain it, it has proved to be a major source of confusion. Bonds are often seen to be confusing, but they are relatively simple investment vehicles. Their entire value derives from their specific, and set, cash flows. While it can often be complex in practice, the principles of bond pricing is very straightforward.

9 Principles – To find out more about how to build an investment portfolio that works for you, read our eBook 9 Principles of Intelligent Investors.