Everyone always talks about investing (and planning) for the long term. But they’re usually vague about what the “long term” actually means. Does that mean 5 years? 10 years? More? (Spoiler: the answer is definitely more). And frankly, talking about how you need to focus on the long term can feel like a bit of a dodge when the markets haven’t been cooperating.

Let’s dig in and think about what “long term” actually means – both in theory and practice.

Long Term in Theory

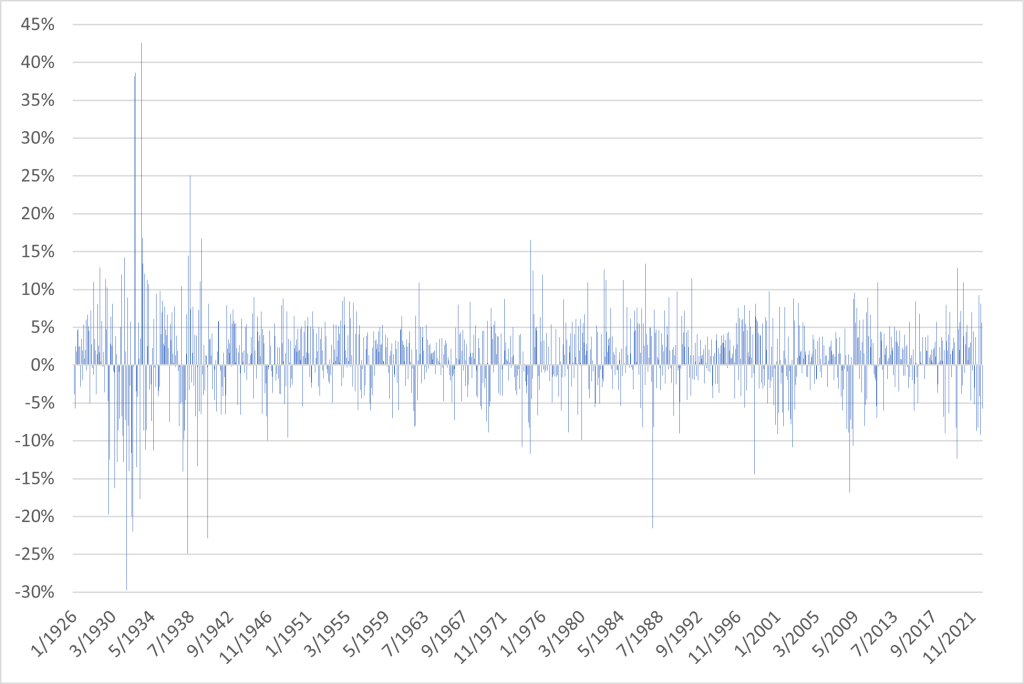

First, let’s discuss theory. Why does investing for the long term matter? It’s not like the market keeps score and will toss us a couple of good years if we have had a run of bad years, or will keep us honest by throwing a bad year into a bull run. The market is way too messy for that. Financial returns are nearly random. A good way to see this is to just look at the returns. For instance, below, we have the monthly returns of the S&P 500 Index from January 1926 to December 2022. We can do all sorts of statistical analysis on these returns (and we have), but it comes to the same place as just eyeballing the data – each return is largely random. It’s effectively impossible to predict what will happen next.

A common way of describing this is to say that the market moves in a Random Walk. Each individual step that the market takes (the next return) is basically random.

But not completely random.

While we may not be able to predict each individual step, there is a direction that this walk is generally going (and we wouldn’t bother investing if this wasn’t the case). But it’s incredibly hard to identify this trend over shorter time periods. In fact, I’ve written an article about how you can’t tell short term stock returns from the flip of a coin.

In essence, the “long term” is however long it takes for these trends in the Random Walk to assert themselves.

Keeping Risk (and Return) Honest

These trends are all of the different risk premia on offer in the market. For instance, stocks are riskier than bonds, so they tend to have higher returns than bonds. If this were not true no one would buy stocks. There’d be no reason to. Why would you buy something risky (stocks) if you could get the same return with a safer asset (bonds)?

These risk premia are the market’s way of getting you to buy risky assets. And the riskier an asset is (at least for certain types of risk), the bigger the risk premium, and the stronger the trend in the Random Walk.

But it’s called a risk premium for a reason. It’s risky. There are no guarantees. There are absolutely going to be periods – even relatively long periods – when the Random Walk is not our friend and the randomness overwhelms the trend.

For risk to actually be risky, it can’t always work out.

That said, the longer you stick around, the more likely it is that that trend will assert itself. But you’ll never get to 100% certainty – there’s always a chance that things won’t work out no matter how long you stay invested. This is part of the bargain we make when we invest in risky assets. To get the higher returns “promised” by the markets, we need to accept the risk.

Putting it Into Practice

But this is all very abstract. It’s important to think about (and make peace with) but it doesn’t really help us put numbers around our primary questions – how long is the long term?

So let’s do that.

But before we do, let’s think about what we’re looking for. Just like most big fundamental questions, there are no definitive answers, and no bright lines. We’re not going to be able to say that 24 years is “long term,” but 23 years isn’t. We’re dealing with gradations here – different levels of confidence. But putting numbers around this can help make the question more concrete.

As I said, there are never any guarantees with investing (I’m going to beat this point into the ground) but we can see the effects of a longer time horizon very clearly in the data. To do this, we’ll keep things simple, and just focus on the S&P 500 Index. But these same principles apply everywhere in the financial markets. This is a story about the fundamental relationship between risk and return – and what that means.

For this analysis we’re going to be looking at rolling annualized returns of the S&P 500 Index over differing lengths of time from January 1926 through December 2022. What we’re asking is if you invested at a random point in time during this period, what would your return have been?

A good place to start is by looking at the range of returns. What were the best and worst returns for each holding period? Let’s start by looking at the data.

| Holding Period | Best Return | Worst Return | Total Range |

| 1 Year | 162.88% | -67.57% | 230.44% |

| 3 Year | 43.35% | -42.35% | 85.70% |

| 5 Year | 36.12% | -17.36% | 53.48% |

| 10 Year | 21.43% | -4.95% | 26.38% |

| 15 Year | 19.69% | -0.41% | 20.10% |

| 20 Year | 18.26% | 1.89% | 16.37% |

| 30 Year | 14.78% | 7.80% | 6.98% |

| 60 Year | 13.32% | 9.03% | 4.28% |

The results here are fairly obvious. The longer that you are invested, the narrower the spread is between the extremes. But there are actually two things going on here that are worth talking about. The first is what we want to focus on – the effects of your time horizon on your investment returns.

But the second is a little less obvious. We have fewer independent observations with the longer time periods. For instance, with the 1 year observations, we have nearly 100 separate 1 year periods (each year from 1926 – 2022), but we only have about one and a half independent 60 year periods. This means that the longer time periods will naturally have more overlapping data. This will tend to reduce the variance of the returns for these longer time periods relative to the shorter periods that have relatively less overlap in the data. I don’t want to overemphasize the point, but it is a limitation that we need to consider as we look through everything.

But even with this in mind, the difference between the range of the 1 year returns with the longer term returns is astounding. The range between the best and worst 1 year returns was 230%. The range for the 60 year returns was only 4.3%. And not only that, the worst 1 year return immediately preceded the best 1 year return. Short time periods will whip your portfolio around, and really emphasize just how random the Random Walk can be.

And with the longer term returns, they contain all of the craziness of the shorter periods. But over time things have balanced out. The trend in the Random Walk has time to show itself.

Looking at the Distributions

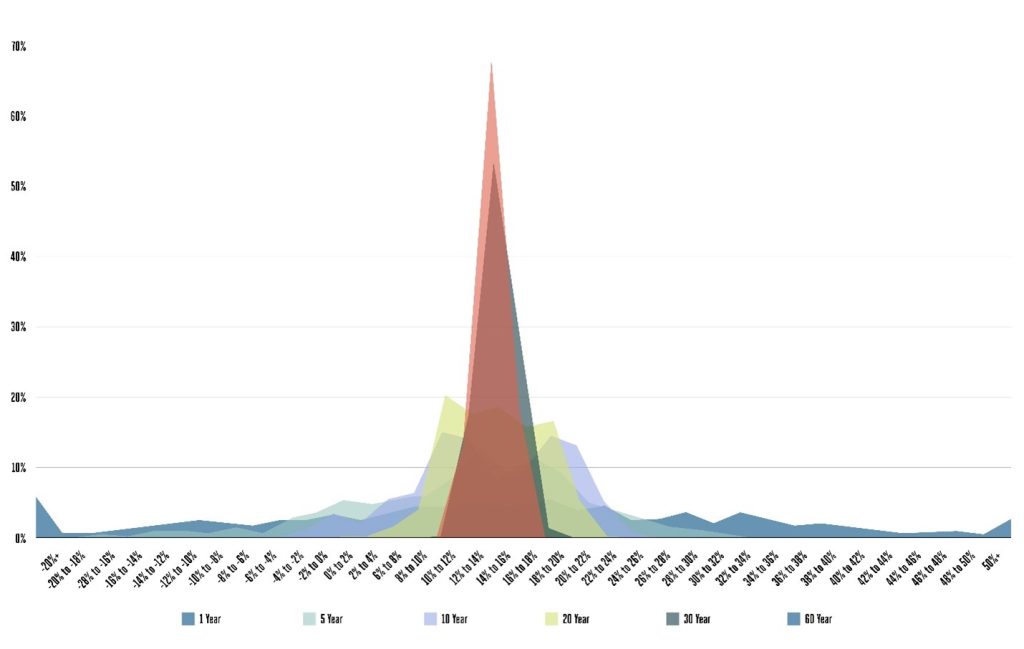

This is interesting, but it’s purely focused on the edges of the distributions. And we don’t want to do our planning based on outliers. So let’s look at the actual distribution of returns – how often each holding period had a particular return.

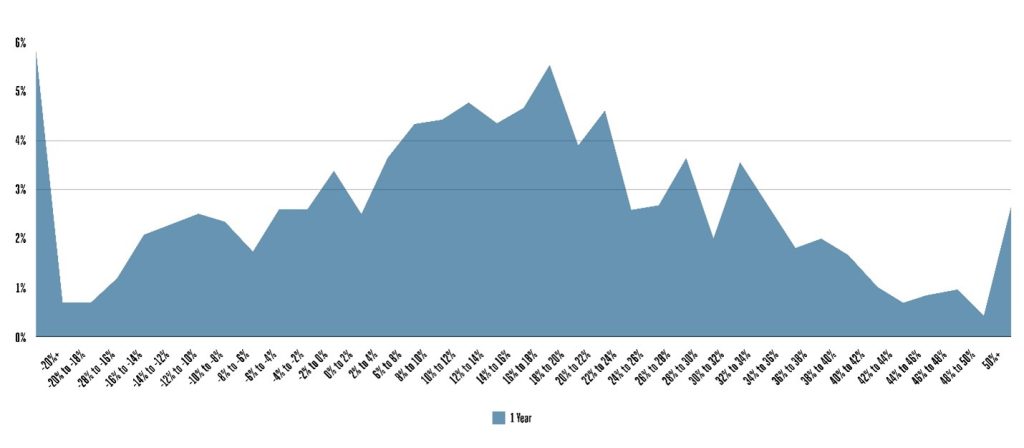

Just like with the range of returns, this data is relatively well behaved. The longer time periods have a much tighter distribution than the shorter time periods. In fact, if we focus in on the 1 year data – even when we zoom in (take a look at the differences in the scale), it’s not that much a curve.

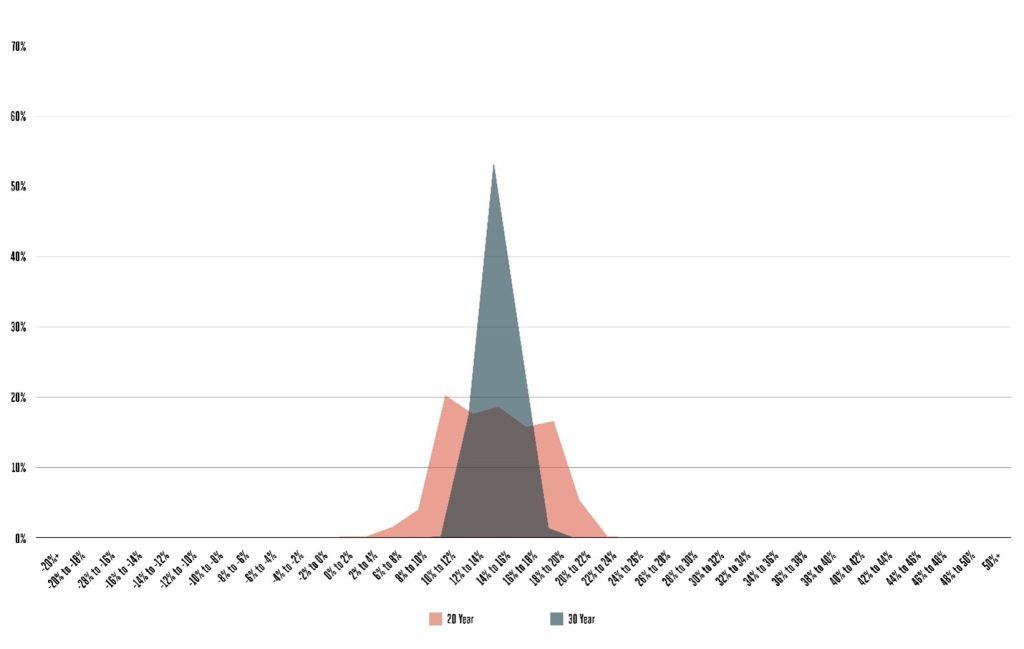

It’s basically all over the place. There’s a little bit of a cluster around the average, but not much of one. When we compare this to the 20 or 30 year observations, we can see the difference very clearly.

With both of these, there’s a very clear curve. They are mostly centered around the average return, but there’s still a little bit of dispersion. With the 20 year time periods, there was a little bit more than a 15% chance that you would have an annualized return of less than 4% and a little bit more than a 20% chance that your annualized return would be more than 14%. As a point of comparison, with the 1 year periods, you would have had a 30% chance of a return below 4% and a nearly 48% chance of your return being more than 14%.

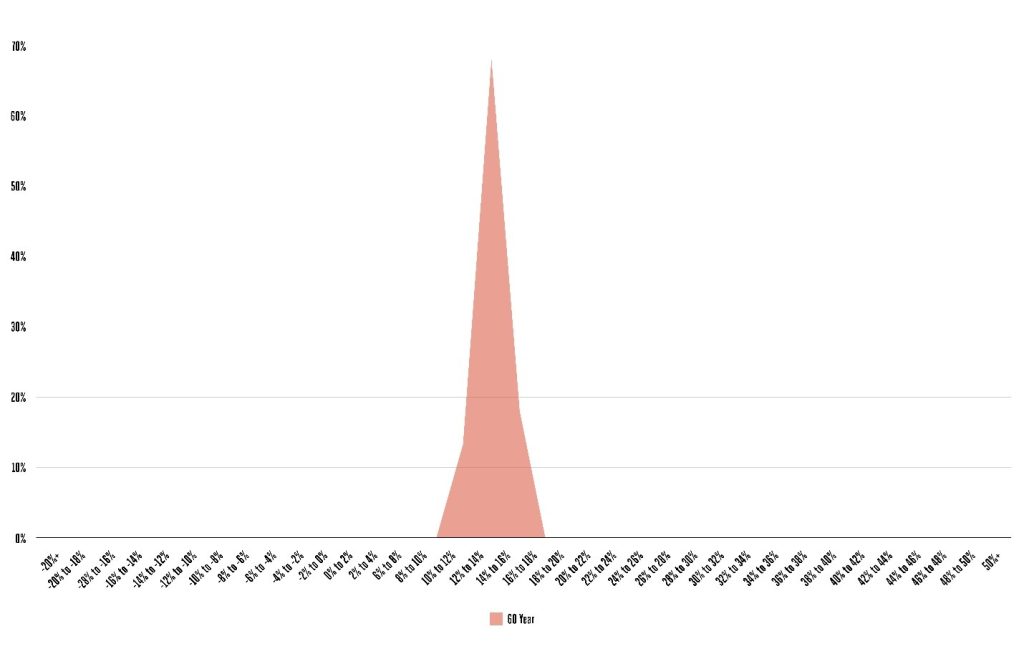

And when we look at the 60 year period in isolation, it’s basically a spike.

There’s technically a distribution here, but almost 70% of the observations were within a 2 percentage point range.

The longer you give your investments to work, the more confident you can be that you’ll be able to harvest the risk premia that we talked about – those fundamental risk and return relationships in the market. There are still no guarantees, but if you wait long enough the randomness in the Random Walk tends to cancel itself out.

What Can You Do With This?

But we can get even more practical. Generally, when people ask what the long term means in the context of investing, they are asking one of two things: how long do they need to be invested to be “sure” they don’t lose money, or that they’ll do better than some alternative investment. So let’s look at those questions.

We’ll start with the simpler of the two – how long you would need to have been invested in the S&P 500 Index to be “sure” that you wouldn’t lose money (we’ll ignore inflation here for simplicity’s sake). I’ve got the quotes around sure here because, again, there are no guarantees in investing. The most confident that we can be is to say that during the time period we are looking at there were no periods of a specific length where the S&P 500 lost money. That doesn’t mean it can’t happen in the future.

And even ignoring absolute certainty, different people are comfortable with different levels of risk. What it takes for one person to be “sure” is going to be different than what it would take for another person. This is all about the varying gradations. So after all that, let’s look at the data.

| Holding Period | % of Observations Greater than 0 |

| 1 Year | 75.4% |

| 3 Year | 84.4% |

| 5 Year | 88.2% |

| 10 Year | 94.9% |

| 15 Year | 99.8% |

| 20 Year | 100.0% |

| 30 Year | 100.0% |

| 60 Year | 100.0% |

There are two things you probably noticed immediately:

- The S&P 500 Index does pretty well if you just want to avoid losing money (though there are probably better approaches if this is your goal).

- It doesn’t take all that long to be pretty confident (at least based on this set of data) that you won’t lose money investing in the S&P 500 Index.

The first point is one we all know reasonably well – stocks tend to go up over time. We wouldn’t be having this conversation if that wasn’t true. And over this time period (1926 – 2022), the total annualized return for the S&P 500 Index was 10.12%. But this should actually give you a little bit of pause. Nearly a quarter of our 1 year periods had a return more than 10% less than the overall annualized return for the period. It’s one thing to look at standard deviation numbers, but this helps drive home what that actually means.

The second point is more specific to our conversation, though. There were no periods of 20 years or longer where the S&P 500 Index lost money. And there were only 2 out of 985 15 year periods where it lost money as well. Again, there are no guarantees, but this would likely make a lot of people pretty comfortable that a 20 year holding period (or even 15 years) would be “long term” enough to be reasonably confident that would have a positive return.

What’s the Alternative?

But let’s turn to the second (and more important) question. How long do you need to invest to be confident that you’ll beat out an alternative investment strategy? To keep things simple, for our purposes that alternative strategy will be owning 5 Year US Treasury Notes instead of the S&P 500 Index over the same time frame. We want to know how often we would have been better off investing in stocks compared to bonds (at least based on the total returns at the end of the period.)

As a point of comparison, on a monthly basis, over the total time period, the S&P 500 beat 5 year Treasuries 59% of the time. In other words, in 41% of months bonds beat stocks.

We know that stocks tend to beat bonds over longer time periods because stocks are riskier than bonds, but again, we’re seeing the Random Walk in action. In almost 5 months of every year, on average, bonds beat stocks.

But what if we look at a slightly longer time period than a month?

| Holding Period | % of Observations Stocks Beat Bonds |

| 1 Year | 66.9% |

| 3 Year | 72.5% |

| 5 Year | 74.3% |

| 10 Year | 82.4% |

| 15 Year | 86.1% |

| 20 Year | 98.6% |

| 30 Year | 100.0% |

| 60 Year | 100.0% |

We see pretty much what we expected (at least in a general sense). Stocks beat bonds more often over a full year than they did each month, but stocks still lost a third of the time over the course of a year. In fact, you would need to wait a little bit longer than 5 years to have a 75% chance that the S&P 500 would beat 5 Year Treasuries. And this isn’t some aggressive benchmark – this is one of the foundational relationships in investing. Stocks are supposed to beat bonds.

And they do. You just need to give them some time. There were no 30 or 60 year periods where stocks lost to bonds (phew).

Putting it Into Perspective

There are no clearcut answers for how long the “long term” is. But it’s longer than most people think. Investing for the long term doesn’t mean a handful of years. It means decades. It means your investing lifetime. This doesn’t mean that you can’t make changes along the way. Your portfolio and retirement plan will change through time. You will change through time – your situation in life will change, what you want from your money will change. And we’ll find new ways to invest that allow us to more effectively capture the fundamental risk and return relationships in the market.

But we can’t make those changes as a reaction to the short term, random, gyrations of the market.

As we’ve seen, the Random Walk really is random. The market is going to do some just plain weird stuff. We know this going in.

But over time, that randomness (and weirdness) melts away. And what is left behind are the fundamental risk and return relationships in the data – the risk premia that we want to build our portfolios around.

The trick is that you need to commit to your investments. You need to commit to seeing this through to the “long term.” One of the few things that we can say with complete confidence is that your investments are not going to follow a straight path. They are going to bounce all over the place (remember that chart of the monthly S&P 500 returns.) But if you give them the time, their Random Walk will get you where you want to go.