Planning for inflation is crucial when designing your retirement plan. While the average annual inflation rate from 1926 to 2023 was around 3.01%, expectations for the future are somewhat different. In this article, we explore how Treasury Bonds and TIPS (Treasury Inflation-Protected Securities) help us gauge future inflation expectations and how this impacts retirement planning.

Retirees Are More Vulnerable to Inflation Than Average

For people focused on retirement as this big financial focus, inflation is absolutely something to be thinking about.

We often talk about how you are different from the average investor. And one of the classic examples of this is that retirees are generally significantly more exposed to inflation than the average investor.

There are a number of reasons for this: you are (or could be soon) spending your savings, your reliable income sources may not be adjusted for inflation (or may only adjust with a significant lag), or you may have a lower ratio of stocks to bonds than other investors (we’ll talk about this one in a bit). But the upshot is that high levels of inflation can put a strain on your retirement income plan.

Addressing Inflation Fears After the Pandemic

And this is exacerbated by the high levels of inflation that we saw following the pandemic. There were a number of reasons for why we saw high inflation, but thankfully inflation rates have come down substantially.

Currently we are seeing inflation rates that are well below the historical average, and it appears as though that will continue into the foreseeable future.

Using the Market to Estimate Future Inflation

We can use information from the market to estimate future inflation. By looking at the difference between the yields on Treasury bonds and the yields on TIPS (Treasury Inflation Protected Securities), the market is telling us what it expects inflation to look like through time.

The logic here is simple. The only meaningful difference between “normal” Treasury bonds and TIPS is the inflation protection built into TIPS, so the difference in price is how much the market is willing to pay to remove inflation risk over the life of the bond. In other words, what the markets think inflation will be during that period.

Current Inflation Rates

Let’s start by looking at what the numbers are telling us currently.

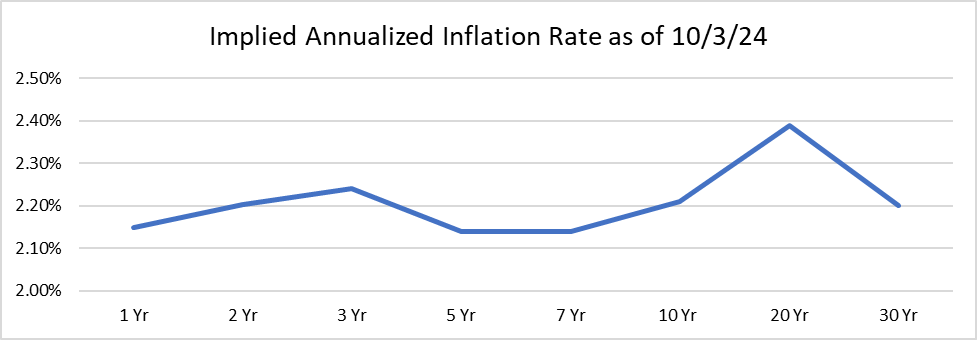

Below is the implied annualized inflation rate based on the difference between Treasury Bond and TIPS yields.

As we can see, the implied future inflation rates are staying in a pretty tight range going forward – between 2.14% per year (for the 5 and 7 year time periods) and 2.39% per year (over the next 20 years).

Now, it’s important to recognize that these are annualized rates – what the markets expect to happen over the entire time period – not necessarily that we will have the same inflation rate each year over these periods. In fact, it can’t work that way since all of the time periods start today and go forward. Even though we’re looking at a pretty tight range on the estimates, the numbers aren’t all the same.

Understanding Forward Rates

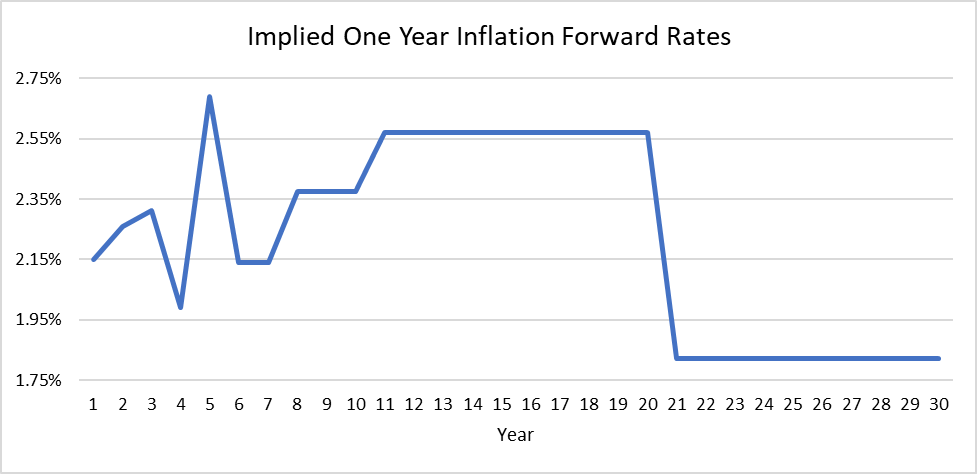

Even though we are (semi)directly looking at expected annualized inflation rates, we can actually pull the numbers apart and look at year by year estimates of inflation through something called Forward Rates.

Let’s say that we want to know what to expect in terms of inflation over the next three years. We expect that over the next three years the annualized inflation rate will come out to 2.24% based on the spread between three year Treasury bonds and three year TIPS. But it’s pretty safe to assume that we won’t have inflation of exactly 2.24% each year for the next three years.

To see how forward rates work, imagine a bond maturing in three years. Like any bond, it’s a promise that you’ll get a certain series of coupon payments, and then the face value when the bond matures (at the end of the three years).

Well, another way to think about it is actually as a series of three one year bonds. In other words, you can buy a one year bond today, and then another one year bond when the first one matures, and then finally a third one year bond when the second one matures.

Assuming that markets are pricing things appropriately, this series of three bonds should be economically equivalent to the single three year bond. If this is true, then we can do a bit of math, and figure out the value of each individual bond to someone today. I know that this can sound a little bit convoluted, but it’s an incredibly powerful technique that allows us to do some really cool things.

Implied Annual Inflation Rates

But for our purposes, these forward rates allow us to estimate the year by year inflation rates. So let’s go back to that three year inflation rate.

We know that the market is estimating that over the entire three year period, the annualized inflation rate is going to be 2.24%. But we also have information about what the market expects the inflation rate to be over the next year (2.15%) and over the next two years (2.20% annualized).

Stringing these numbers together we can figure out what to expect on an annual basis. So let’s start at the beginning.

The market is expecting the inflation rate over the next year to be 2.15%, which we can take as our base number since we are looking at this in terms of years. But we also know that the market is expecting inflation to be 2.20% over the next two years.

The inflation rate in the second year will be whatever makes the math for both of those statements true. In this case, that means that the markets are expecting the inflation rate in the year after next to be 2.26%.

And then we can the same thing for the third year (which comes out to 2.31%), and then on down the line.

When we do out all of the math, it looks like this.

(If you really want to dive into the math here, all of this data is from our Implied Inflation Calculator that is available to members of the Retirement Researcher Academy.)

It’s not quite as tight of a range as the smoothed out annualized numbers, but it’s still a pretty tight range. In fact, the highest expected annual inflation rate is only 2.69% five years out from now (and remember, the historical average annual inflation rate is 3%).

Since retirees are more exposed to inflation risk than the average investor this is really great news for people focused on retirement, but it doesn’t mean that we should be complacent. We still want to make sure that our retirement plans are able to handle inflation – especially the risk of unanticipated inflation.

Building Inflation Into Your Retirement Planning

All of this is interesting information, but we need to be able to apply it to our retirement income plan for it to be useful. And, as much fun as it would be, using a different inflation rate for each year would be a little unwieldy.

As a baseline, you’ll likely want to start with an inflation rate tied to your planning horizon. If you’re 90, you’ll probably be more focused on shorter term inflation than someone who is in their 60s. From there, you can either use the market’s expected inflation rate, or bump it up to make the analysis more conservative.

Another step that you can take is to run multiple scenarios of your plan and vary the inflation rate (including potentially varying it over time in your plan) to see how that will affect things.

While it’s likely that a higher inflation rate isn’t going to do your plan any favors, every plan will respond differently to inflation. Seeing how your results change will help you understand just how exposed to inflation you are.

But how do we go about dealing with this risk? If inflation has a big impact on your retirement income plan, what are some things that you can do to address that? If we focus on the asset side of the equation, I break things into two categories: indirect strategies, and direct strategies.

Indirect Inflation Protection Strategies

Indirect inflation protections are things that are sensitive to inflation and quickly incorporate changes in future expected inflation.

While they may not be specifically tracking inflation, these assets (partially) move based on what inflation is likely to do in the future. If the estimate of the five year inflation rate changes, the price of these assets will change, at least to some degree, in response to this. This category, at it’s most broad definition, incorporates pretty much all financial assets, but there are two that I really want to focus on: stocks and short term bonds.

Stocks are great, if incredibly noisy, hedges for inflation. Aside from having higher expected returns (which make up for a lot of sins), there are a couple of different mechanisms that tie stocks to inflation. The most important of these is that inflation is figured into that expected return. In a higher inflation environment, investors demand a higher expected return to hold stocks.

The story is pretty much the same with short term bonds. When bond investors are deciding how much they are willing to pay for a bond (in other words, the cash flows from the bond), they consider how much they think those payments will actually be worth when they receive them.

What makes short term bonds special is that frequency with which the portfolio is bringing that information to bear. The bonds held in a short term bond portfolio turn over more quickly than the bonds in a longer term portfolio – and that means that new information about inflation (and everything else) gets absorbed incredibly quickly.

Direct Inflation Protection Strategies

On the direct side are things that are based on actual inflation. These are things like inflation riders on annuities, TIPS, or I-bonds.

The specifics of annuity inflation riders will depend on the individual contract, and can vary widely, so we’ll put them to the side here (but they can be great tools in the right situation).

TIPS and I-bonds are both US Treasury securities. We talked about TIPS earlier, but I-bonds, or more technically Series I Savings Bonds, operate on essentially the same idea. Their payments change with the actual inflation rate that we are experiencing. When we have higher inflation, their payments increase. TIPS do this by adjusting the principal amount of the bond, and I-bonds do it by including both a base fixed interest rate payment, as well as a variable interest rate payment based on inflation.

The big difference between the two is that there are pretty strict limits on the amount of I-bonds that you can buy at once and what accounts you can hold them in, whereas TIPS are marketable securities that are just out there for you to buy and sell as you please. On the other hand, I-bonds tend to pay (much) higher interest rates.

Designing Your Portfolio (and Retirement Plan) for Inflation

Figuring out how to balance all of the competing demands in your plan is hard. Removing inflation risk from your plan is not free. As you’re thinking about how exposed you are to inflation risk, and how you want to deal with it, you need to keep that cost in mind. And this cost can come in many forms.

The costs with direct protection are, well, pretty direct. An insurance company is going to charge you for an inflation rider on your annuity. On average, TIPS will have lower yields than “normal” US Treasury bonds. And they just make I-bonds hard to use. But even with the sources of indirect inflation protection, there are still opportunity costs and tradeoffs to consider. You only have so much space in your portfolio, so it is always a balancing act.

You need to look at your portfolio as a cohesive whole. If you are focused on retirement, inflation is probably a risk that you want to address. But there are other risks that you need to deal with, as well. You need to find the mix of solutions (and risks) that you are comfortable with, and that will help you stay disciplined to your overall retirement income plan.

Retirement planning is about controlling what you can and being prepared for what you can’t. With inflation, it’s wise to build flexibility into your plan, ensuring that no matter how the economy shifts, you remain on track to the retirement lifestyle you want.